2/18 MacroEdge Weekly Report - Doubling Down on Nevada Data as It's Too Cold to Fold & More

In this weekly report - Don. Six, Greg, and John tackle the latest economic issues including Nevada labor market woes, inflation risks, tons of data, and more. Catch the rest at MacroEdge.net

Doubling Down on Nevada Data as It's Too Cold to Fold (@DonMiami3)

Hi all -

I hope you are having an enjoyable and uneventful second-to-last weekend of February. I am sitting here again on the road gearing up for a busy week ahead, the mind never truly stops while traveling, as many of you probably know. I do hope you all enjoyed my piece from very late in the evening on Friday - our first edition of a special series called ‘Redeye’.

It’s been a busy last few months for us here at MacroEdge - I am thrilled at our progress on the development of Ozone V2 and the new site that will be coming out sometime soon (expect an announcement at some point). We’re going to be making a big impact in the world of finance and economics as we continue to expand and we cannot say enough thank you’s to you all who continue to read and support us week after week.

If you haven’t made the switch to Ozone yet - you can do so here thru Substack (which gets you access to our legacy Ozone platform and you will be transitioned over when the new platform is complete) + weeks of trial:

Or here on our website directly at MacroEdge.net/get-ascend

Today - like I do every few months or so - I want to turn our attention back to the data coming out of Nevada. While the Nevada economy has remained…

Full article included in this week’s MacroEdge Weekly Report only available at MacroEdge.net.

Global Tightening Rattles Economies: Recession, Inflation, and Strategic Moves in a Turbulent Market (@SixFinance, MacroEdge Head of Research)

The global tightening cycle this week continued to inflict its’ slow burn, causing Japan and the UK to both slip into a technical recession (two consecutive quarters of negative GDP growth). Germany, the powerhouse economy of Europe has now overtaken Japan on a GDP basis, while remaining in a prolonged slump for the second consecutive year. The third and fourth largest economies are now in a technical recession, and China in second place has a laundry list of issues and although it reports positive growth, its’ financial sector is having serious issues due to the enormous overdevelopment of Real Estate…

Full article included in this week’s MacroEdge Weekly Report only available at MacroEdge.net.

2024 Inflation: The Dollar's Purchasing Power Now 'Dust in the Wind' (@GregCrennan, MacroEdge Contributor)

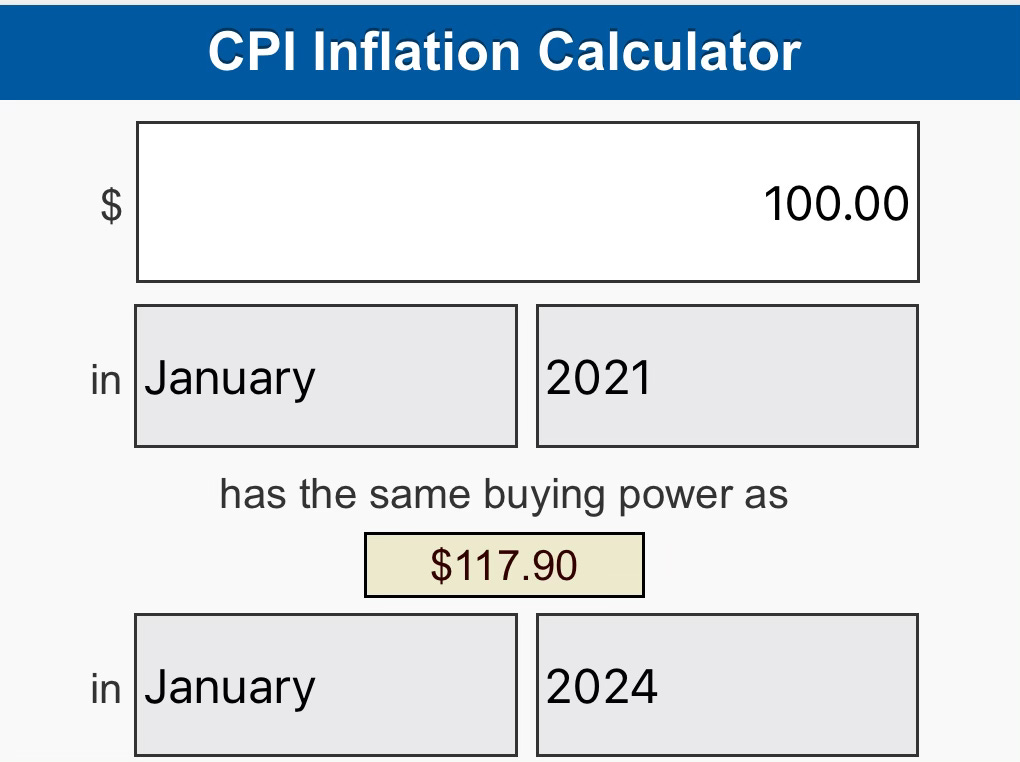

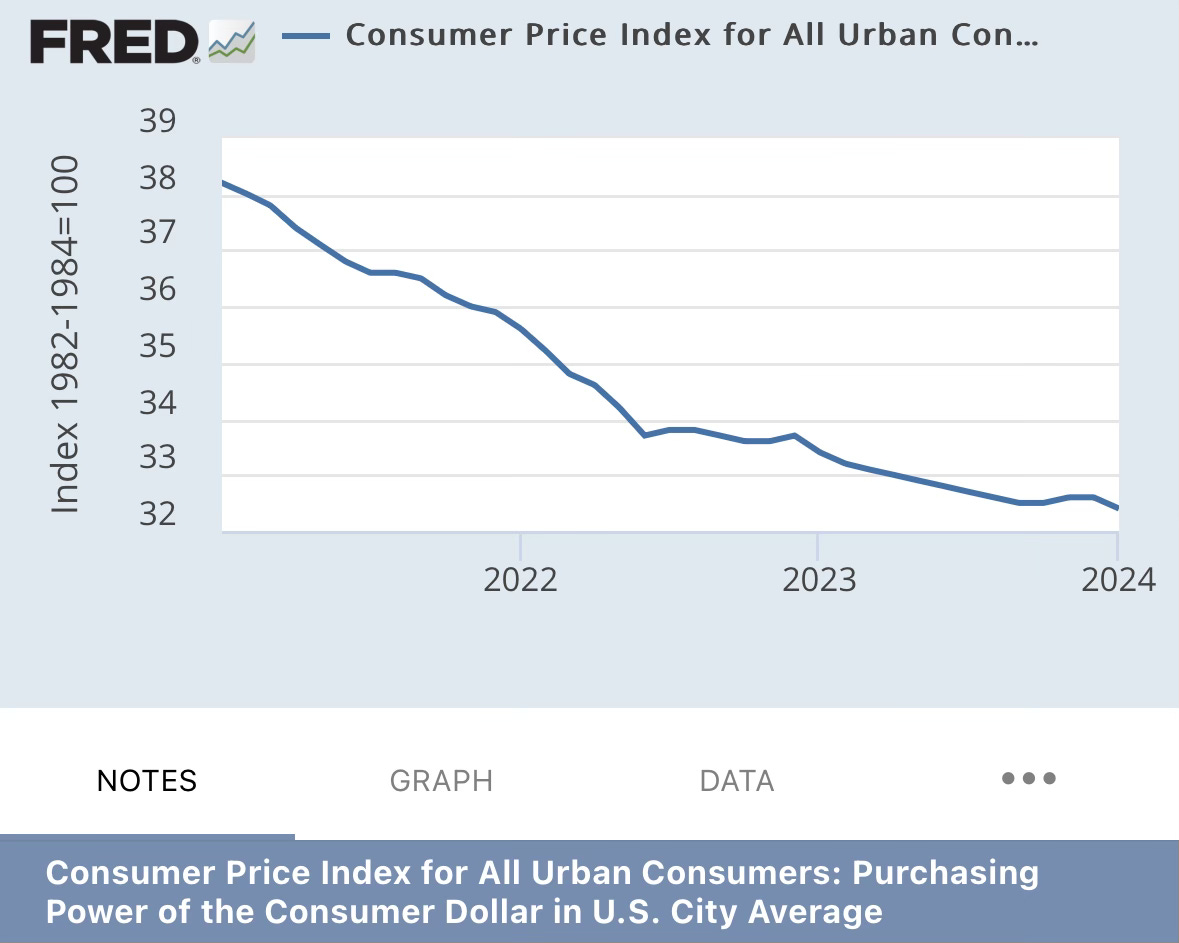

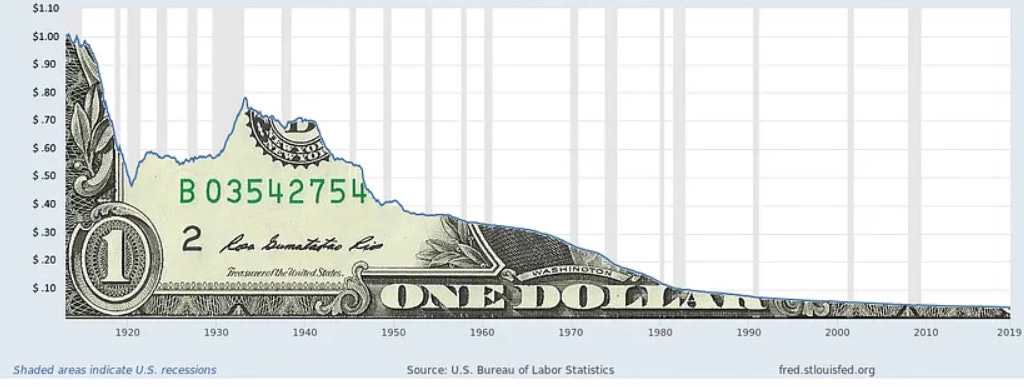

As 2024's economic data begins to unfold, today's revelation of the U.S. inflation figures casts a foreboding shadow over both Main Street and Wall Street. The haunting strains of Kansas' timeless anthem, "Dust in the Wind," echo through the corridors of economic analysis, underscoring the grim reality of eroding purchasing power, particularly since January 2021. To illustrate the gravity of this loss, consider this: if you saved $100 in 2021, that same $100 would now require to be $118 just to purchase the same goods in 2024. With inflation now poised to reach another 4% in 2024, it appears increasingly likely that the dollar will have depreciated by a staggering -22% over the past four years.

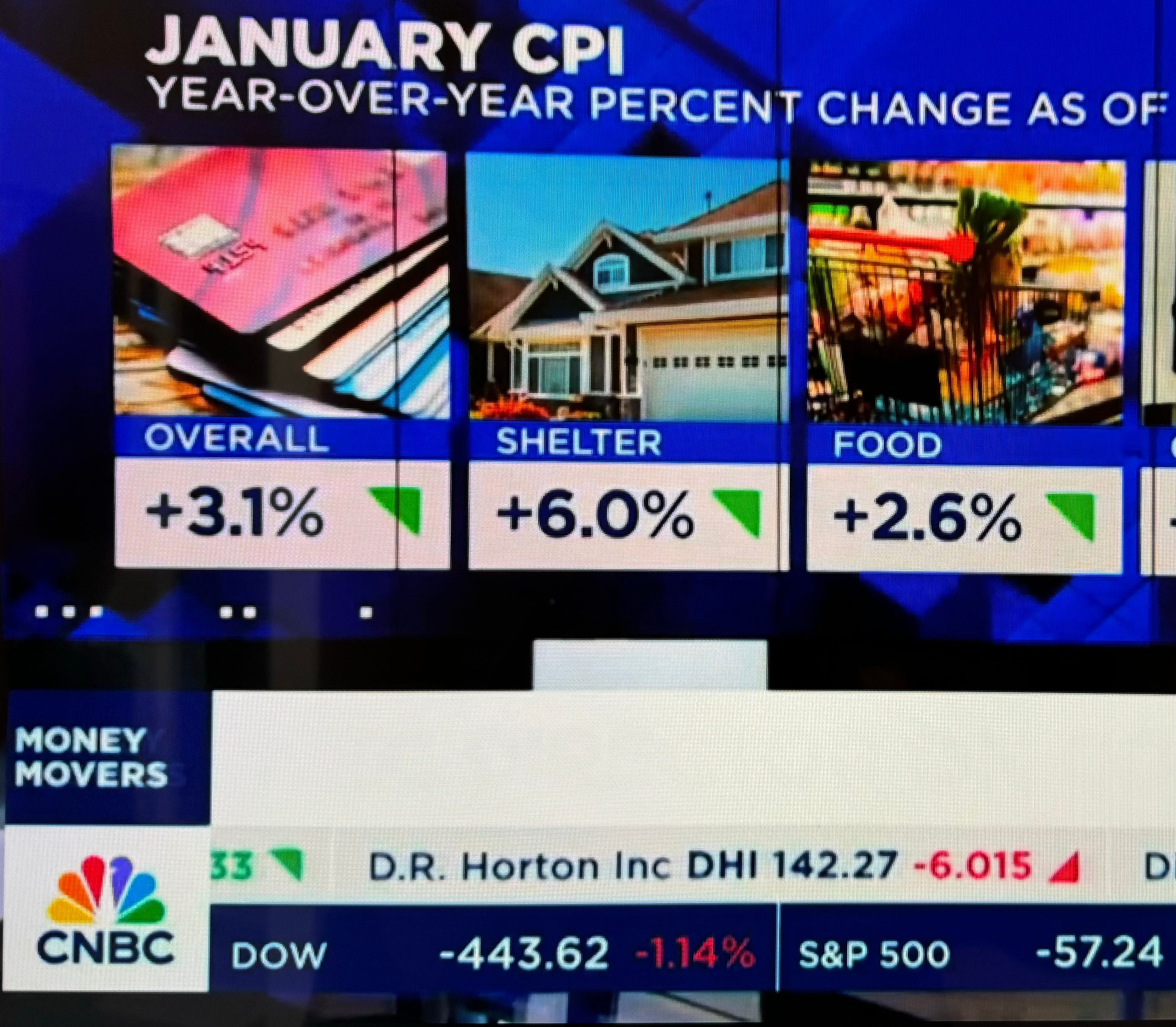

The inflation data, revealing total and core inflation rates of 3.1% and 3.9% respectively, mark a departure from the anticipated slowdown in price increases. These figures, exceeding the Federal Reserve's purported "normal" inflation target of 2%, stand as a testament to the relentless erosion of the U.S. dollar's value. As Kansas sang, the dollar today just seems to "crumble to the ground," having lost a staggering -18% since January 2021.

On Wall Street, speculation ran rapid since November 2023, with pundits proclaiming victory on the inflation war and advocating for imminent interest rate cuts as soon as March 2024. This speculation fueled a frenzy in financial markets, propelling valuations to dizzying heights, even for companies with questionable fundamentals that don’t make any money and even ones that do. However, with the recent inflation report is shattering these illusions as the stock market almost -2% on the day, financial speculators find themselves confronting a stark reality in regards to rate cuts akin to Kansas' fleeting moment as they: "closed their eyes, only for a moment, and now the moment's gone."

For the average American on Main Street, the repercussions are dire. The erosion of purchasing power, reminiscent of the tumultuous Jimmy Carter era, leaves many feeling the pinch as essential expenses soar. From housing to healthcare, the cost of living climbs at a pace not witnessed since the 1970s. As Americans tighten their belts, discretionary spending dwindles, exacerbating the strain on an already fragile economy. The following price increases stood out on this months report:

Car insurance: +20.6%, House repairs: +18.2%, Vet services: +9.6%, Shipping fares: +9.1%, Baby food: +8.7%, Car repairs: +7.9%, Hospital services: +6.7%, Shelter: +6%, Eating out: +5.1%.

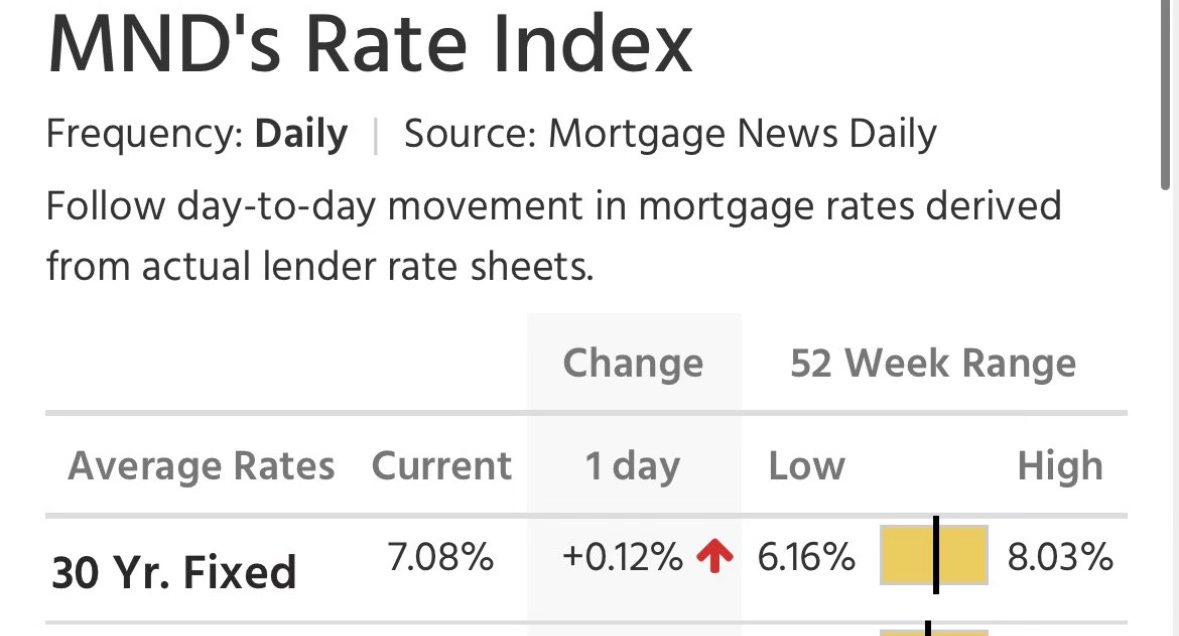

In the realm of real estate, the landscape appears equally bleak. Mortgage rates soared to 7% today,

signaling further distress for homeowners, while increasing supply and dwindling demand makes the real estate bear market continue. Sellers, once buoyed by visions of windfall profits, now find them selves singing the same old song.

In the face of these challenges, the resonant chorus of "Dust in the Wind" offers a sobering reflection on the transient nature of economic fortunes. As investors navigate the unchecked inflation, the haunting melody serves as a reminder of the impermanence of speculative fervor. In this grand symphony of economic flux, where markets rise and fall like passing gusts, the enduring truth remains: all material wealth, all financial grandeur, is but fleeting, ultimately fading away like dust in the wind.

Gold’s Inflation Dilemma (@RealJohnGaltFla, MacroEdge Contributor)

The age old adage that the shiny monetary metal throughout history has always been the ultimate hedge against inflationary times is now being challenged by the current era of global modern monetary theory. Central banks have abandoned their old role of defending the currency of individual nations in favor of economic “stability” which is basically defined as tolerable consumer price increases with illusionary asset valuations.

This too shall pass however.

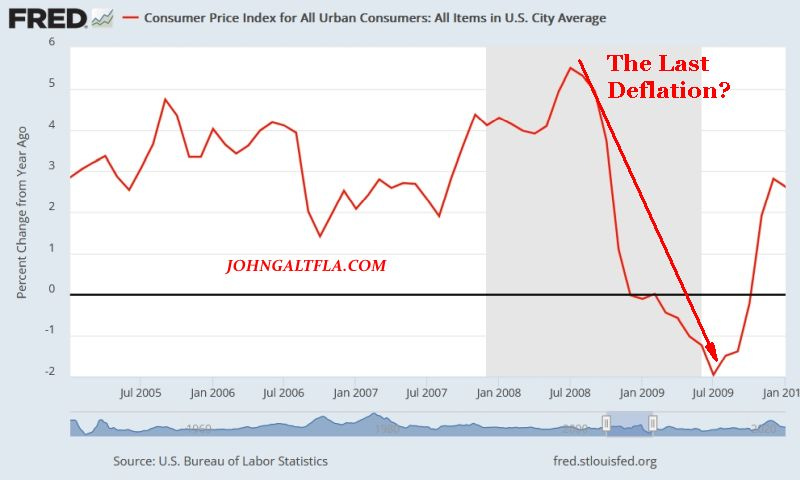

Many individuals remember the Great Financial Crisis which should be more accurately declared the Depression of 2008-2009, where inflationary pressures spiked, then collapsed with an outright deflationary collapse.

While it took over seven months for the March 2009 QE experiment of the Federal Reserve to take hold and began reigniting inflationary prices, the theory that this was the era of the “last deflation” took hold and the belief that joint fiscal and Fed policy would always to be capable of blunting deflation without sparking inflation.

The fears of insufficient Federal Reserve stimulus and a return to credit related deflationary pressure on the global economy were still present in 2010. The fears echoed by Paul Krugman’s alarmist New York Times editorial, The Third Depression(June 27, 2010) where he stated:

And this third depression will be primarily a failure of policy. Around the world most recently at last weekend’s deeply discouraging G-20 meeting governments are obsessing about inflation when the real threat is deflation, preaching the need for belt-tightening when the real problem is inadequate spending.

Fortunately for the world, Mr. Krugman was wrong again, there was no “third depression” and government spending continued at insane rates unabated by political idealism and the threats emanating from conservative ideologues who never demonstrated an understanding on how to effectively govern and institute their policies.

Fast forward past the 2020 Pandemic and one begins to understand that indeed the theories that Krugman was promoting in 2010 were indeed instituted by President Trump and the Federal Reserve in 2020. The idea was that because the government shut down private businesses to protect the citizens from the pandemic, then stimulus would be required to avoid a deflationary depression.

Well, as President Bush would say:

Obviously both of them set the table for a stupid monetary theory which is not based on reality that the US and the world will embrace for now, then suffer for in the future.

So what does this little history lesson have to do with gold prices? Everything.

The new dilemma facing Goldbugs is not hyperinflation as of yet, but stagflation. The policies of Jay Powell and the two major political parties over the last twenty years have all but guaranteed this outcome in the past twelve years and the chart I prefer to use to highlight this is “The Great Divergence” where inflation as reported via the BLS, CPI-U versus gold prices.

If one notes this chart’s initial start date of September 1971, the end of the gold standard, gold and inflation behaved logically right up until 2017. Then the Silent Financial Crisis of 2018, which was blamed on utter nonsense by the state sponsored media, created a sense of urgency for the Federal Reserve to quietly bail out the financial system while proclaiming the economy was sound and stable.

Despite the bailout being announced on Christmas Eve after the markets closed at 6 p.m. by a junior Federal Reserve Governor, not Jay Powell himself.

This brings us to the recent consolidation in gold prices over the past year around the $2000 level. Theoretically, gold should break out substantially after this consolidation but the government and financial media have detected a trend which they are so happy to report on:

Is gold still a good hedge against inflation? Experts weigh in

Inflation will have to get a lot worse to justify gold’s current price

These articles can be found ad infinitum, even during the 2008 financial crisis. The reality of 2008 and what is about to hit the American economy this summer is that gold is a terrible hedge against inflation because the dependency on the US Dollar as the world’s reserve currency keeps the price suppressed in US Dollars.

It is this author’s belief that gold prices will see a decline, potentially below $1900 per ounce as bank liquidity and credit availability further tightens between now and June of this year. The counter to this will be an inflationary wave similar to the July 1980 surge in the CPI-U which ended Volcker’s attempts to reignite an expansion out of the stagflation of the economy for the past half decade.

Economic growth and the toleration for stagflation versus deflation plus the politicization of our financial system will supersede any realistic economic theory or concerns. The belief that the economic powers that be will not allow a crash, that their is no threat of domestic or global conflict, nor threat to the major financial institutions will allow the pressure on gold prices to intensify, despite the inflationary suffering of the lower and middle class in the United States.

That is why I believe that a Fed rate cut of 50 basis points in June and 25 bps in July, followed by a fiscal spending spree by the Romans of DC, will initiate a Modern Monetary Theory type of acceptance of at least two years of stagflation to get past the 2024 election season.

In the end, gold should eventually rebound overseas as priced in domestic currencies first, especially in Asia. If and when gold in US dollars reaches the first ledge on the mountaintop at $2200 on a closing basis, then and only then will $2500 and the reality of a potential hyperinflationary threat come into focus.

Meanwhile, for those of us who invest in precious metals for it’s true purpose, domestic and international instability, we can sit back and enjoy this grinding, nasty, muddle where the tug of war between inflation and deflation re-writes economic theory for the decades to come.