6/29 Weekly Macro Note: More Macro, Race to Pass BBB (the new PPP), Project Zimbabwe Continues, Employment Week, FOMC, & a Big MOAB

The July Turn: More Macro, Race to Pass BBB (the new PPP), Project Zimbabwe Continues, Employment Week, FOMC (@DonMiami3, MacroEdge Chief Economist)

Good Sunday Evening, MacroEdge Readers and Community,

The second half of the year is rapidly approaching, hard to believe, given that February still feels like yesterday. The sharp market ascent has continued across asset classes over the past few weeks (notably equities and metals), though we aren’t seeing the same strength in sectors like real estate. It will be fascinating to see how this all evolves, especially with a potential Fed Chair announcement from Trump, who may name someone early in an effort to undermine Jerome Powell’s perceived “hawkishness.” That said, it increasingly looks like the bond market, not any one individual—will dictate the push to get rates lower, and that push is gaining serious momentum.

As I noted in a recent comment on X, the disconnect between qualitative economic reporting and actual price action—particularly in equities, is the widest I’ve ever seen. As the GOP prepares to push through the latest version of the “Big Beautiful Bill,” expect further feedback loops into risk assets as deficit expansion continues. While we’re not quite matching Japan in terms of how we conduct our fiscal and monetary business, we’re also not far off at this pace.

The recent surge in equities, especially high-beta tech (QQQ), is beginning to track eerily close to the late-1990s bubble era, specifically 1998–1999 in terms of valuations. And notably, performance off the April lows has now outpaced the post-pandemic stimulus rally.

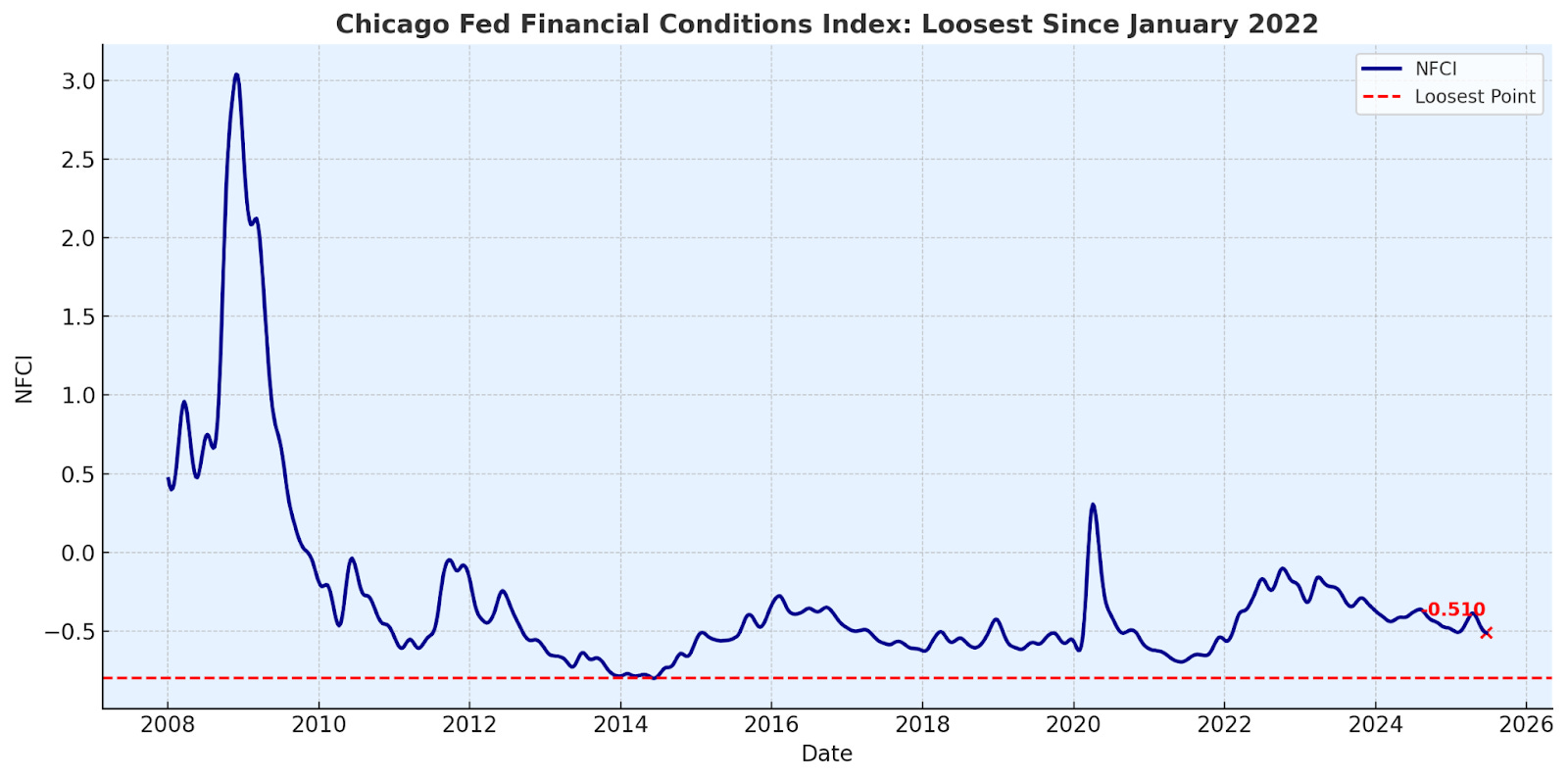

The “nothing ever happens” crowd is out in full force. But they may want to rebrand as the “something major already happened” crowd. We’ve witnessed a striking pivot from an administration that began with a commitment to fiscal sanity, only to revert to a policy mix that now mirrors Bidenomics, Trump’s first term, and even the Obama era. Financial conditions have now loosened to their most accommodative levels since the early-2022 post-COVID mania.

That was just before the Fed hiked interest rates with repeated 75bp rate hikes to tame inflation… (after it was transitory). The name of the game since 2010 has been much looser FCI levels, as evidenced by the Index. Below, we’ll dive more into what’s ahead for equities (and the economy) in the second half of the year. The direction of travel has been quite clear and that will be the case with the Administration being as supportive as they are of equities of late. Until we get our next macro-trigger inflection point, like we saw with our ‘Liberation Day’ moment - don’t look to step in front of a moving train even if hedging the left-tail remains affordable and sentiment remains skewed towards significant optimism.

Tomorrow evening we’ll have our ‘What’s Next for 2H with MacroEdge’ note where you’ll be able to explore all of the new things our team will be rolling out over the next 8 weeks. These include CEO Macro Briefings, AlphaSights + Solutions, Economic Advisory, Transform, and more. We’ll also discuss where to access the new Weekly Macro Briefing videos and much more.

Ozone & Trident

With Trident - we’re turning our leading macro perspectives into action. Learn more about the Trident I Global Macro Fund below:

Access MacroEdge Ozone for two weeks and never miss a beat on our reports, research, data, and more:

More Macro

Back to an employment week… that means more macro as we move away from earnings for this week. This shortened week sees a speech from Powell & Ueda, as well as employment data moved up to Friday. Weaker employment data would greatly strengthen the case

Monday – Chicago PMI, Dallas Fed Mfg Index, 10Y JGB Auction

Tuesday – BoJ Ueda Speech, Fed Chair Powell, ISM Mfg Data, JOLTS Job Openings, Dallas Fed Services Index

Wednesday – ADP Employment Change, BoJ Takada Speech, Total Vehicle Sales

Thursday – Nonfarm Payrolls, Unemployment Rate, ISM Services

Friday – 4th of July Holiday

Race to Pass BBB (the new PPP)

The Senate is racing to smash the Big Beautiful Bill through before the July 4th recess, and the implications for equity markets could be substantial.

This marks a full endorsement of the post-2020 monetary regime that began under Trump with the pandemic response programs. The bill would further expand the deficit, reduce taxes on seniors, and reinforce a market environment that rewards risk-taking and dismisses fiscal restraint. This move from what started off as a ‘fiscally responsible Admin (not)’ signals that the era of austerity is not just over, it never had a chance and passed away a long time ago in this ‘Project Zimbabwe’ regime.

Pressing for Yet More: Overheat Growth Faster Than Debt Expands

A substantial pivot after the tariff pause and the halting of the DOGE efforts came when Bessent noted that they could attempt to grow the economy faster than the debt. This suggests a future of significant money supply expansion, especially as each new spending package delivers diminishing returns. We are still operating with pandemic-era emergency spending levels while GDP growth remains flat. This continues to support the "Project Zimbabwe" narrative, as coined by Harris Kupperman. The long-term consequences of this regime are clear, particularly in its downstream effects on the birthrate and the price level of goods for everyday citizens. However, these consequences will likely be ignored due to the political class's complete inability to exercise fiscal responsibility. Trump, for the first time, acknowledged this today on Truth Social. If they succeed in significantly lowering rates, the runway will remain fully foamed for the ongoing debt bonanza trade. With major single-sector recessions continuing in sectors like single-family real estate activity, this Admin remains hellbent on getting rates lower.

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.