Excited to join you all for our latest weekly report alongside Six and Awsumb.

I am calling tonight’s release ‘Urban Economics’ since that is what our new brand of economic science is becoming here at MacroEdge. We’re attached closer to the beach - than we are to the Street - giving us a unique edge away from Wall Street consensus group think. While consensus forecasters and economists continue to look away from the reality on the ground, obsess over rampant asset speculation, and paper over charts that are critical to economic health (or ignore them all together), we’re one of the last holdouts bringing both our Ozone community and the rest of the financial/economic world a place to interact with reality. That’s been our primary goal from the start: transform the way individuals and enterprises interact with financial and economic data.

Tonight I want to touch on current market sentiment and unemployment data from 3 of the 4 largest states (CA, FL, NY) in the country that point to caution ahead on the labor market, as well as some of the updated data from our Data Dashboard.

MacroEdge is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

This week there’s important data coming out like the latest CPI reading which may have bearing over the Fed’s pace of QT runoff (if they announce this plan) in addition to rate cut probabilities - what I really care about here is still the labor market data and current market sentiment. While Fed cuts may drive a bit more optimism into the market, labor is beginning to look like the Fed is overstayed their welcome at 550bps as long term moving averages roll-over in the labor data (data we’re applying a 12-month lag to, to highlight policy transmission time). I will also briefly touch on some of the latest data we updated in the newest push through of data to our Data Dashboard that you all have access to within the Ozone Portal.

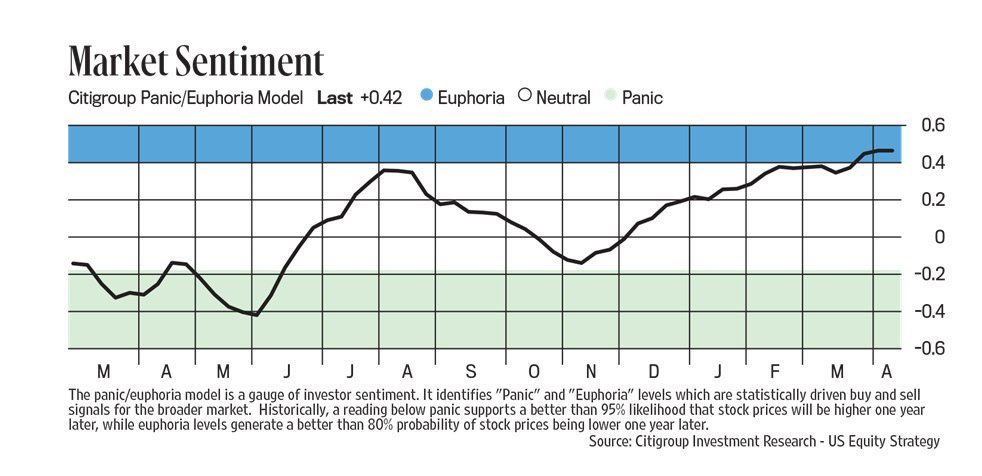

Turning our attention to the current market sentiment - while we saw an interesting reversal on Thursday, everyone went right back to their usual ‘casino’ selves on Friday. I think the Euphoriameter from Citi here provides a very nice overview at where we are in the current market sentiment:

Note: this obviously doesn’t mean price action cannot continue to rise, but it’s interesting that even though we’ve maintained peak euphoria - positive market momentum has slowed down sharply in the second-half of March/early April from where we were from December to February on the ‘green’ escalator. This is the highest reading since the top ranges last seen in 2021.

An update to the very interesting ‘round’ chart pattern occurring on the Nasdaq:

Looks like April and May may be very interesting months in both the data landscape and for markets…

Multiple Job Holders increased noticeably in February and March, almost returning to the pack from last November. It’s interesting that peaks in multiple job holders usually occurs 1-2 years before the troughs of larger employment downturns (notice the spike right before 2020 as well):

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.