MacroEdge Super-Redeye: 'Volatility', Peak Capitulation/Economic 'Nirvana' Circus, Notetaking, a Rant, Data, and Charts...

MacroEdge Super-Redeye: 'Volatility', Peak Capitulation/Economic 'Nirvana' Circus, Notetaking, a Rant, Data, and Charts...

Your average person couldn't put this together from a loud SoBe cocktail lounge... Let's go on a plane ride together - through my brain, through the charts, data, thoughts and more - on Redeye...

(@DonMiami3, Chief Economist - MacroEdge)

*excuse typos on Redeye

I know many of you are out enjoying your Friday evening (as you should be) - which is my time to shine from a more relaxed scene this evening… I first began authoring my thoughts to the world almost a year ago now here on Substack and sought to get out a different voice to a broader audience which resulted in MacroEdge - from last October to present… Very cool beans to see us go viral with coverage on some CRE sales this week (the AT&T Tower in St. Louis and another auction in Baltimore) and all of the data we oversee from labor market data to manufacturing, school closures, and more. We’re on a mission to do it all. Six is also now leading our new Vision Equity Research Desk - and pioneering ways to identify opportunities in markets both here at home and abroad for us.

Now is the time to hop on the train with us and join us as we transform the economic and financial data landscape for years to come, through slow times, confusing times, and euphoric times. You can get access to MacroEdge Ozone directly through Substack while we continue to maintain posts on this platform:

or go through our updated V2 web interface and get two weeks of access at MacroEdge.net/OzoneTrial . With Ozone you get access to our monthly updated interactive data dashboard, our weekly research reports, weekly equity research desk reports, live actionable market data, Social Club and more.

I look forward to us finally moving off of Substack in the coming months for everything but Redeye but we will make

Another Friday Evening…

This evening I want to dive right into the action the past few days in the market itself - which we have spoken about briefly the past few weekends - then discuss in depth some of the ‘peak capitulation’ activity we are seeing both from those on the more MMT/married to low rates crowd as well as those who were ‘bearish’ through 2022-present who have given up on all of their complex theories and evidence supporting a likely economic downturn. We’re in a weird spot in both markets & with the labor continuing to cool and geopolitical risks - it’s important to assess where we are in this long and drawn-out cycle in the post-QE4 world. That’s why we’ll touch on inflation data as well as some important labor market data, and lastly wrap up with a few updated data points on the health of the manufacturing sector - one of the more cyclical economic sectors tracked in our Cyclical Leading Employment Index…

Market Movements

Peak ‘Mania’ and Capitulation

Inflation Goes Hot

Labor Market Continues to Cool

Manufacturing Sector Health

Market Movements - A Volatility Blip or More to Come (Charts and More):

While the chart below we shared to our Ozone members Current market sentiment remains in the bounds of euphoria - it is likely around the .4 mark to end today on the sell-off. What is quite interesting is the potential shift in the market regime of ‘up only’ to one where we may see a relief bounce in the first half of this week before being able to reassess a potential larger sell-off to the downside.

The whole ‘everyone is bearish’ narrative is bullocks - nearly every single corporate leader I interact with on a day-to-day basis, politicians, the everyday American speculating in the markets, and most X users that we get to interact with are all in and they think the Q1 rally autopilot casino is the permanent reality of a new ‘nirvana’ market backed by the largest debt/GDP ratio since WW2.

Does sentiment determine ‘nirvana’? I tend to think not, and the reality is in the data. While the reality does back a much more bifurcated future for the American economy (see my: Your South African Future) work that I am in progress on for what I am outlining about the underlying permanent shifts underway in the American economy.

There is an interesting pattern within the technicals chart itself (several of you requested that I start posting these) on the Nasdaq. We closed near the low of the lower trendline after falling below the ‘Valhalla’ trend from December-end of March, and have been sideways now for about a month. The larger structure here appears to be an (at least) short-term reversal in the trend, which may play out over the next several months. Note that this is only from a technical perspective and needs to be taken in the larger economic context as well as in the context of upcoming tech earnings… it’s a market myself and Six alike are remaining nimble in on the Vision Research Desk side of things.

Similar patterns are playing out on the S&P and Dow and more confirmation will be given in the coming weeks on a longer-term directional shift if one takes hold here or if the ‘nirvana’ narrative moves asset prices higher. The market here at these levels is one that was pricing in the Fed perfect landing scenario - and now with talks today of just one or two rate cuts for the year, risks are growing for any landing but a hard one as the Federal Reserve continues its overstay in restrictive rate territory (2y/FFR) - not to be confused with loose financial conditions.

With the VIX interacting with the pre-COVID trend that it has struggled with for four years, I am hesitant to think any huge reversal to this trend will occur, but that remains to be seen.

The theme here is: be nimble with this very ‘hard-to-read’ casino/nirvana market

Peak ‘Mania’ and Capitulation:

The signs of ‘mania’ are ever present which is why I think the latest rhetoric of late (especially given the length of our 10y3m inversion and weakening economic data) should be paid close attention to. While the financial media, pundits, and X influencers have a tough time even sitting through about a 1.5% drop intraday without showing their outlandish emotions - I have been collecting a compilation of some of the best ‘capitulations’ and pivots to the economic nirvana narrative as soft landing island becomes packed with even more newcomers and any other landing island becomes barren and desolate…

Some seem to think we’ve financially engineered our way into ‘economic nirvana’ as the AIER stated it back in 1991 when downturn struck, but this seems to be a weird theme that appears over and over throughout the modern economic period (defined as 60s-present):

We’ve gone through this merry-go-round before on past ‘Nirvana’ maxxers praising government spending, deficits, technology, the Fed, etc as reasons to expect a permanent nirvana in the quarters and years to come. Much of the data - from manufacturing to employment - looks like anything but ‘achieved nirvana’. That doesn’t mean they won’t kick the can and utilize financial engineering to kick the can as much as possible in months to come (student loan waivers, mortgage forbearance continuations, etc).

Let’s took at look at some of nature’s finest exhibits from the last week:

(This is a public company, lol, very ‘chic’ 2000-like?) - I have spent time with people very close to the charter aviation industry, it’s a mostly terrible business to be in post-rate hikes, way oversaturated and we’ve seen operators dropping like flies over the last several quarters (including larger operators like SetJet who couldn’t afford their payments on the Bombardier’s). A lot of the business ideas coming out of the United States (including business innovations) are arguably not very innovative at all in recent times… It’s hard to put a finger on whether or not this is a byproduct of maximum innovation output achieved over a particular period of time or if ZIRP for so long has just encouraged terrible business ideas… Maybe a little bit of everything?

Let’s take a look at the world’s best contra indicator:

Another ‘doomer’ flipping, bullish?

A nice young man that thinks his complex-sounding theories about MMT, financial engineering, and technology are new:

Trendy NY Times author declares the business cycle dead as his industry undergoes huge job cuts (due to business cycle):

Who is still giving this circus clown business financing?:

To me… it looks like we’re much more aligned with peak mania and peak ‘capitulation’ from reality found in the data, then economic nirvana… price action and recency bias do make people crazy in their own casino worlds though…

Inflation Goes Hot:

Commodities and other inflation-sensitive basket items continued to move higher this week - although many saw an abrupt reversal towards the end of the day as the market moved lower.

We saw an acceleration in the deadline CPI #, and a substantial rise in the Supercore basket.

The next few weeks will be interesting on the commodities side to see if the ‘re-inflation’ trade continues, or if the winds come out of the sails for a few months. With wide uncertainty around both the economy and geopolitical situations - I am open to a multitude of scenarios playing out here… you can see more on my thoughts on oil, particularly from previous reports in the last several months.

Labor Market Continues to Cool:

On the employment side, the dynamic and lag of this cycle are very long but not uncommon compared to past cycles. The window is rapidly narrowing for the Federal Reserve to not over-exert force on a tightening labor market. With a larger population in the United States compared to February 2020 (Indeed’s Live Job Openings Baseline) - the labor market continues to swiftly tighten and it is becoming more and more difficult for white-collar laborers to find work. Things remain okay on the part-time side of the equation and also among lower-paying sectors in the blue-collar workforce, but on the aggregate - the labor market continues to cool:

U6 lag underway (labor moves very slowly, claims usually moves much quicker although we can do a deeper dive on the disconnect on the initial claims side of things in the coming days):

Nice little media outlet coverage:

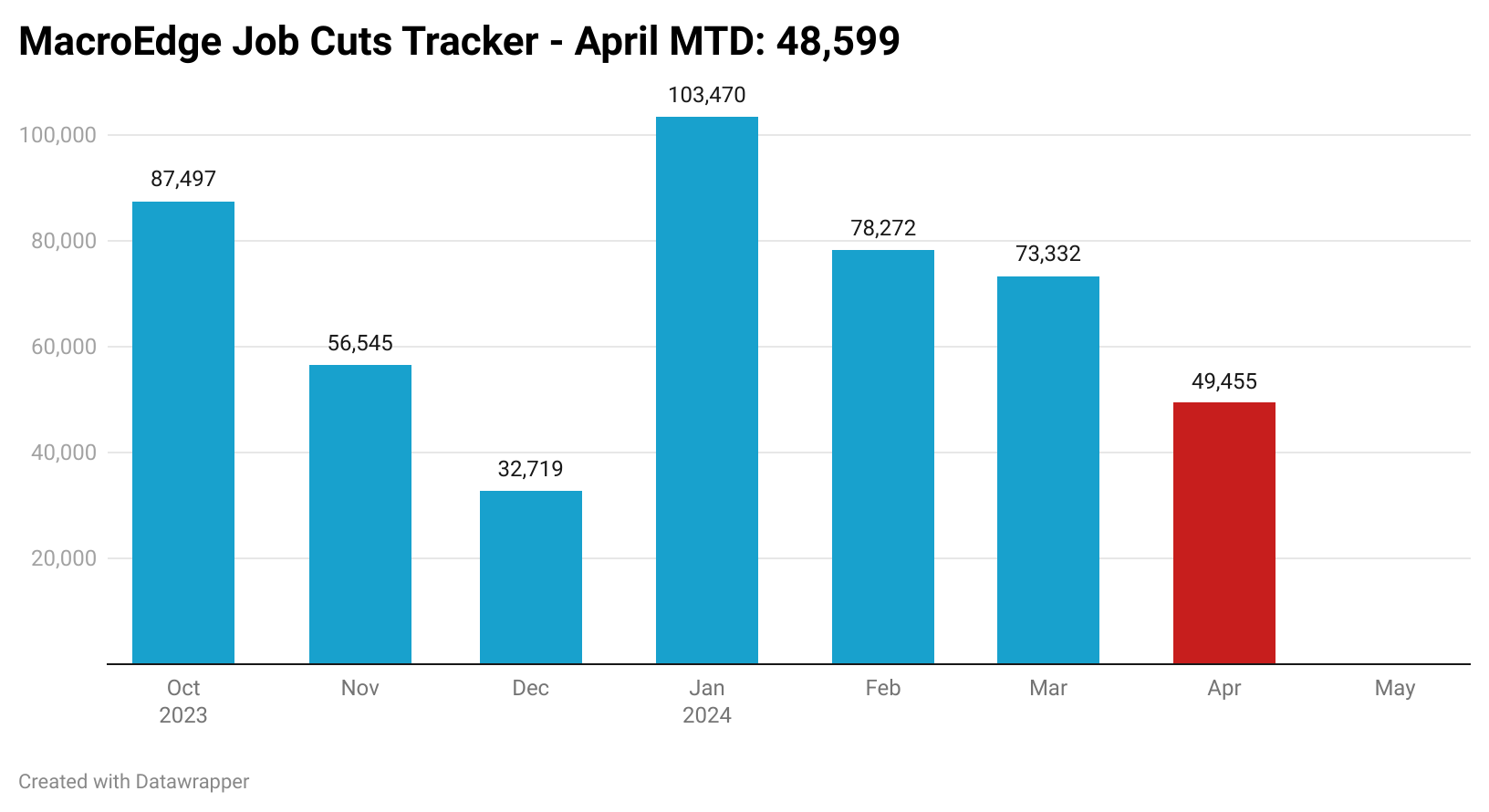

Job cuts for this month are elevated and we have plenty of earnings reports coming up in the second half of the month that may propel the total # of job cuts to around the 100,000 mark… These job cuts are adding up.

And job openings are down 2% in the last month and now back at May of 2021 levels:

At current pace - we will see the # of job openings back to pre-lockdown levels nationally in about 6-12 months.

Manufacturing Sector Health:

One of the more important and overlooked ‘hyper-cyclical’ areas of our economy is the manufacturing sector… While there’s a whole lot of talk about onshoring and political speak on a ‘boom’ in American - the downturn in manufacturing began months back in both total industrial production (total industrial output) and in capacity utilization - employment in manufacturing which has shown signs of slowing down as well (contributing far less to headline employment in recent months) and usually follows Capacity Utilization and Industrial Production fairly closely.

Capacity utilization continues to weaken marking the ‘end of the growth cycle’ for manufacturing this time around. The key indicator is when capacity utilization sees a 5% or greater decline it’s marked a downturn every time since 69.

Notice how manufacturing employment mimics capacity utilization drops >5%. The manufacturing base in America is much smaller than it used to be on the employment side of the equation - so arguably it plays ‘less’ of a role on the overall headline payrolls figure, but the cyclical nature of employment in the sector is pivotal in driving downturns (ie: early 90s and 2000s both saw substantial contraction in manufacturing employment).

Lastly, industrial production (total industrial output):

Zoom in for the last 20 years and the manufacturing ‘boom’ of the last 3 years doesn’t look like much of a boom at all. The lagged average is just rolling over.

Enjoyed sharing this longer Redeye with you all and hope you have a fabulous weekend… Look forward to seeing you all in the Ozone for Sunday’s report…