Midweek Macro Note: All for Faux: Equity Rally Continues to Defy, Retail Floods the Zone, Bifurcated Outcomes, Tariff Price Pressures, & More

In this Midweek Macro Note - the team discusses the latest in earnings, the everything asset bubble that has continued to make records, retail margin and record trading activity, technicals, + more.

All for Faux: Equity Rally Continues to Defy, Retail Floods the Zone, Bifurcated Outcomes (@DonMiami3, MacroEdge Chief Economist)

Good Wednesday evening MacroEdge Readers and Community,

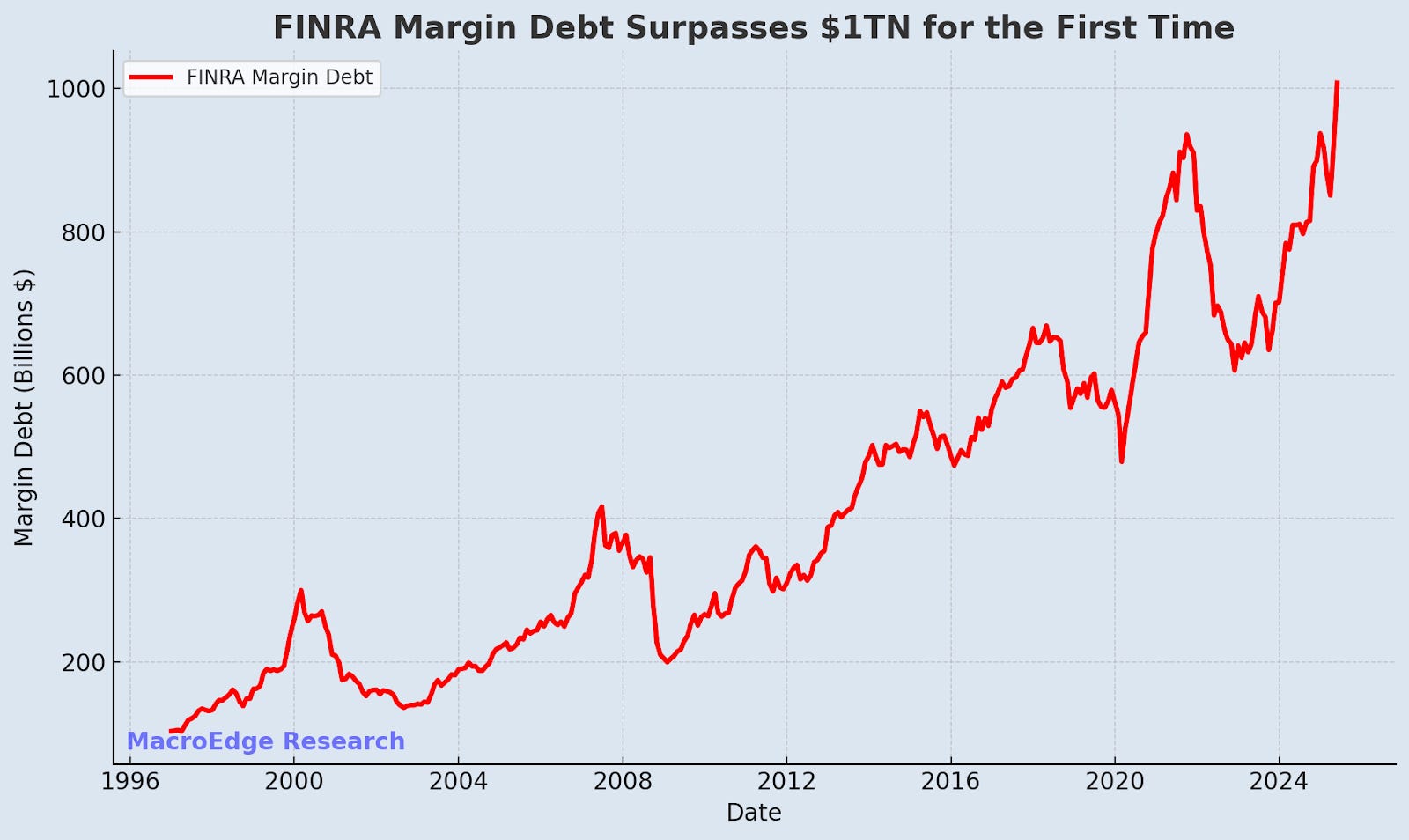

This week we’ve seen a small continuation of the much broader rally that’s been underway since the April lows. Much of this optimism has been driven by the pull forward of rate cut odds to September, including the expectations for a second cut later in the year - potentially in October - to take us through the remainder of the year. Rate cuts are likely to spur a short term spurt in housing and mortgage activity - though if we use Canada and the United Kingdom as any barometer - it won’t likely bring a broader housing recovery which is being reflected in lumber prices right now, even though homebuilding stocks have participated in the speculative rally from the April lows. Rate cuts will improve margins for homebuilders, though it will likely impact volume on their end, as they’ve already started to eat into their home prices, with broad based reported declines among the builders in earnings this season, so far. Any impact from the initial easing has been very minor, though speculation remains substantial in the equity and cryptocurrency markets, but has been capped by a lack of credit expansion in a lot of other sectors. Note that credit expansion has been abundant in markets - with margin debt surpassing $1 trillion for the first time - and it’s likely to hit the $1.3-1.5 trillion range if the current rate of change and addition of margin to trading accounts continues.

The 1999 scenario/Japan 88 scenario has hit terminal velocity - and has been amplified by dollar weakness. The deficit in July approached $300bn - a $3.6 trillion annualized rate - a second highest print on record for the month, only behind COVID. It’s a very complicated macro picture given all of the Frankenstein-esque monetary and fiscal forces at play now, and even though qualitative data and hard econ data continues to point towards softening - the asset class itself is stronger than ever - bolstered by equities and crypto at all-time highs and up 40-50% from the lows, a historic rally matched by no other time in history for how quick the rally itself has materialized.

Every bubble continues to get amplified by leverage and retail access to it, at the core:

This cycle just happens to be unique in the sheer volume of fraud and greed out in the wide open.

Data Rest of Week

For the rest of the week, we’ve got the PPI reading tomorrow, along with claims, continuing claims have continued to move higher from the start of the year, though job cuts have remained somewhat similar relative to last summer now. Initial claims haven’t seen a huge boost from DOGE-related cuts yet, but there is still very gradual labor market cooling under the hood.

On Friday, the day remains macro-heavy, with retail sales, import/export prices, and manufacturing data, along with consumer sentiment. There’s also the continuation of earnings for the next several weeks - including some of the larger semiconductor companies. It’s not likely that we see the momentum here stop immediately, though I do note some of the materializing technical risks below, as valuations have surpassed their 2021 highs.

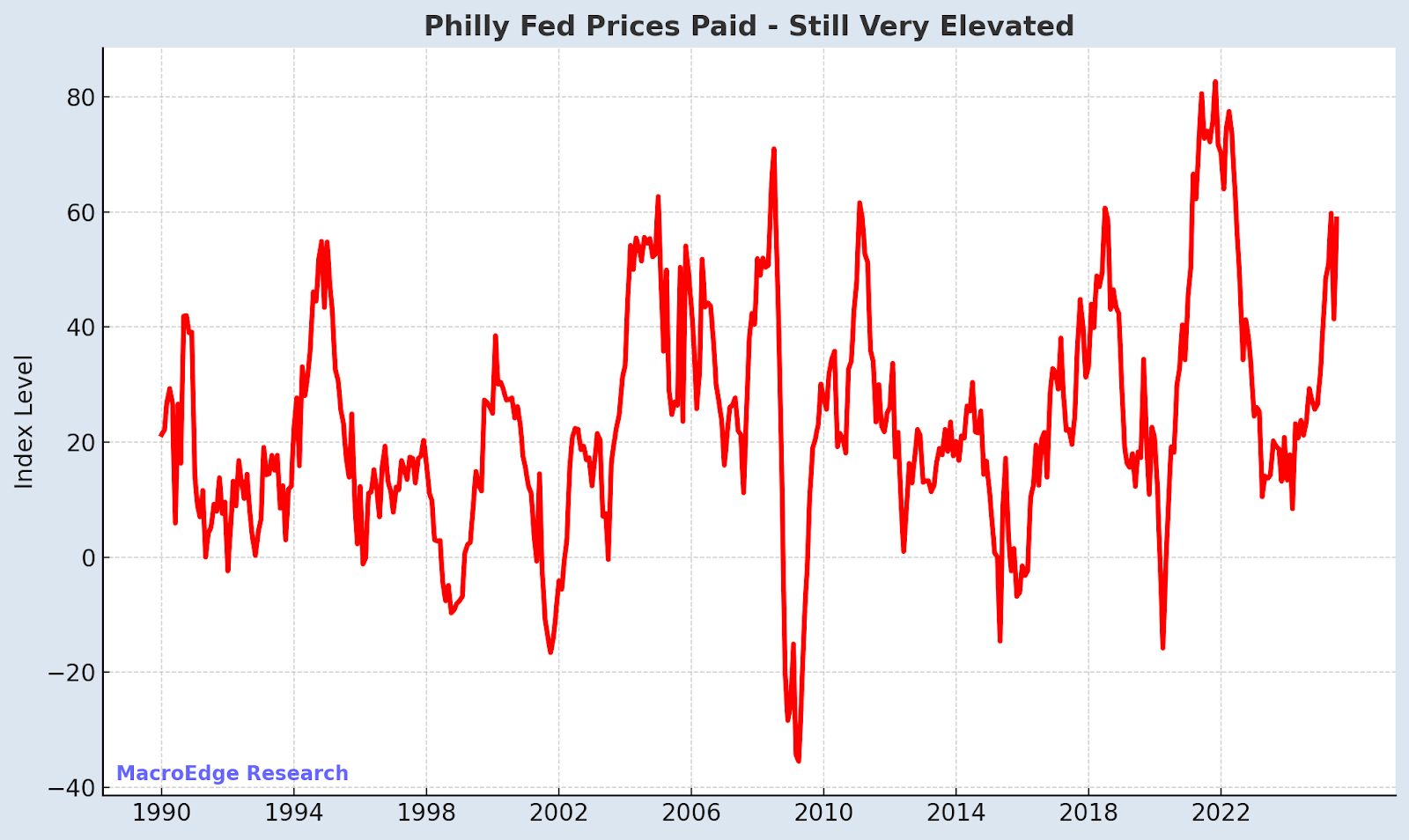

On the PPI front - producer prices showed no signs of cooling in the latest NY/Philly Fed leading Prices Paid indices - which usually lead the PPI reading by several months. All of this either eventually materializes into disinflationary forces again, as the best cure for high prices becomes high prices – though that’s more complex then meets the eye in today’s world & macro backdrop.

Equity Rally Continues to Defy & Retail Floods the Zone

The equity rally shows no signs of exhaustion in the short term, even as valuations have now pushed beyond their 2021 peaks. Retail money continues to pile in, chasing upside and ignoring the narrowing breadth under the surface. This participation has helped push momentum into overdrive, yet it also creates an environment where a sharp unwind could be amplified if sentiment flips. For now, dip buying remains relentless and corporate earnings, especially in high profile sectors, are keeping the tone bullish.

Are Markets Really…

It is worth asking whether markets are operating on fundamentals or simply running on liquidity and animal spirits. The resilience in risk assets, despite flashing macro risks, points to a disconnect that has historically resolved with volatility. Key macro prints this week could serve as catalysts to either reinforce the narrative or fracture it.

MacroEdge Ozone

MacroEdge Ozone is transforming the way funds, firms, and individuals see data and financial research. Our cutting-edge team and infrastructure enable us to stay ahead of the pack — especially at the critical moments. Access MacroEdge Ozone below for two weeks and experience the difference.

Inversions Stay Inverted

The yield curve remains deeply inverted, a stark reminder that historical, recessionary indicators have not gone anywhere, even though their efficacy has come into great question. Despite a rally in equities, the bond market continues to signal caution. The length and persistence of this inversion are now among the longest in modern market history, and while timing the exact inflection has been a fool’s game, the odds of a soft landing greatly depend on where one lands in their socioeconomic status, and how far policymakers are willing to push us down the Japan pathway of hyper-financialization.

Commodity Land Bifurcation

From lumber to gold, to energy prices, cattle, and more – the picture here is as complicated as it gets… on the other hand, the grocery bill speaks for itself, and the restaurant bill does too.

QSRs Get Cooked in the Kitchen

The ‘fancy’ quick service restaurants - Cava and Sweetgreen, got smashed after their latest reportings. Quick service restaurants (QSRs), especially at the elevated or premium tier, are starting to crack under pressure. Consumer discretionary spending patterns show a pullback in higher ticket fast casual, with some operators reporting traffic declines and margin compression. The post-pandemic pricing power story appears to be breaking down, forcing operators to rethink promotions and menu strategies.

Bifurcated Outcomes - Technical Overview

Two clear scenarios here - either a record-breaking crash up, or a sizeable correction to materialize in the 2H of the year. Given the obvious macro risks, it’s a very cheap hedge to punt at the very least, while keeping exposure on the table for an Administration that can’t handle a single red day materializing in financial markets.

That’s all for the Midweek Macro Note…

Don

How Retailers Like Walmart Pass on Tariffs to the Public (@RealJohnGaltFla, MacroEdge Contributor)

After listening to Peter Navarro bark like a trained seal on Bloomberg Television this afternoon, I fear this brief thread is more necessary than ever. Courtesy of YouTube:

To stay consistent, let’s review what these pages published after the June CPI reportand update the same everyday consumables that were quoted on July 15th.

Food at Home: MoM (month over month) up 0.3% YoY (year over year) up 3%July: (MoM) 0.2% YoY: 2.2%

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.