Midweek Macro Note: CPI Report, Geopolitical Tensions, WTI Movements, Vision Note

In this Midweek Macro Note - the team breaks down the CPI Report, discusses the new geopolitical tensions between Israel/Iran, talks about WTI movements, and the Vision team provides an update.

(@DonMiami3, MacroEdge Chief Economist)

Good Wednesday evening MacroEdge Readers and Community,

This evening we’ll briefly go over the CPI report today, discuss what’s ahead for the week - prep for the FOMC next week - where we expect no rate cut from Powell’s Fed, touch on the geopolitical tensions, WTI movements, touch on a brief technical overview, and Six will close with a note from our Vision team.

We’ll have our first ever CEO Macro Briefing out next week covering energy: particularly the asymmetric opportunities in oil and gas, and this will provide a preview of what we are developing with the Briefings as well expand our data collection capacity out across our pilot markets through the 2nd half of the year… something that I am extremely excited about as we build out our ‘boots on the ground’ micro-level relationships and data infrastructure. At the event of the month we’ll have much more in our 1H 25 wrap up - with new releases, details on Trident, timelines, and much more.

CPI Report

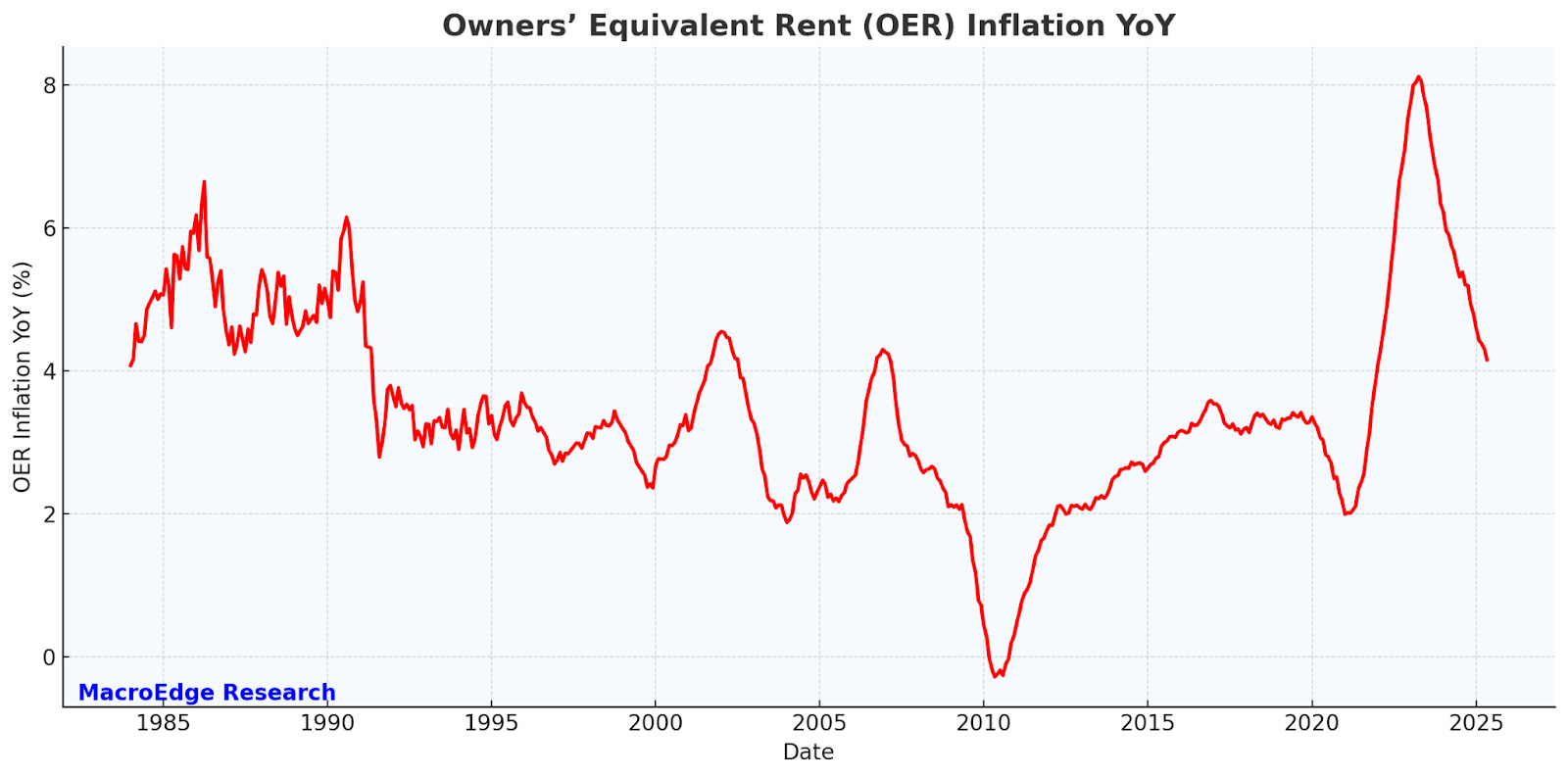

The CPI report showed slightly softer inflation then consensus expectations on a m/m basis - but y/y CPI bounced back from the April lows to 2.4% y/y. OER showed signs of further cooling - even though it was an important component causing the y/y increase - being up .3% month-over-month. Outside of that - medical care services increased +.3% m/m, household furnishings rose +.3% m/m, motor vehicle insurance rose .7% m/m (y/y +8/2%), & personal care prices rose .5%, while education prices increased .3%.

The largest decliners in May:

Gasoline prices (y/y -12%, m/m -2.6%) - this has likely bottomed for its effects on CPI

Airline fares fell 2.7% m/m

Used cars and trucks -.5% in May

New vehicles -.3%

Apparel & eggs (-.4% and -2.7% m/m) respectively

Housing shelter remains the dominant inflation driver, supported by healthcare and insurance. Energy and transportation prices have pulled CPI lower - and the Trump Admin should note that as those base effects wear off (look at energy prices over the last week).

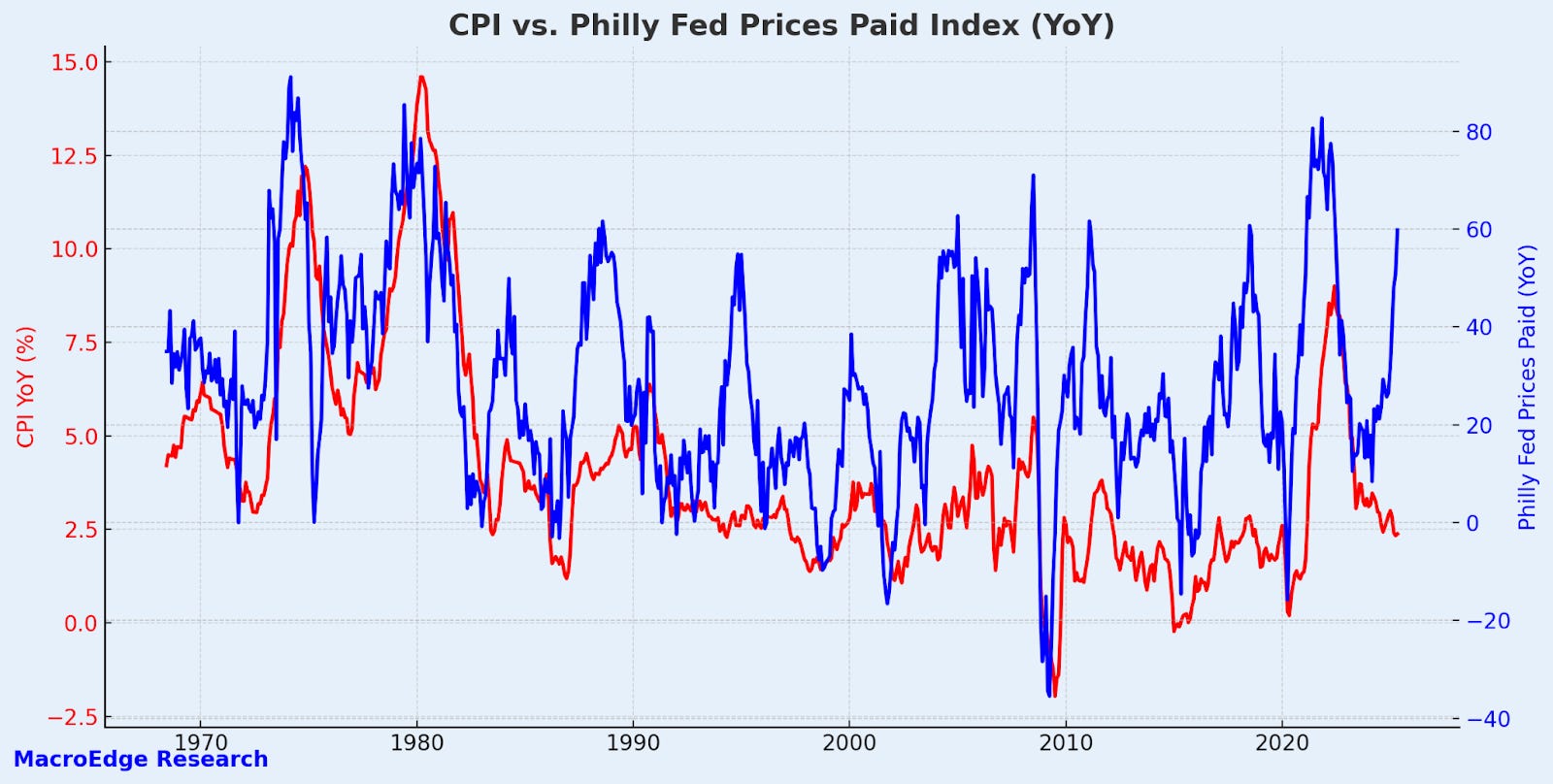

Versus Prices Paid (CPI operates with a lag)

As we’ve discussed many times this year - CPI has been lagging input prices, and tends to do so historically.

Current variance is nearly 2STD, but not there:

Of note - above - the outliers tend to be when CPI has risen sharply, lagging input prices – if you add in the tariff factor and a new energy factor if it plays out - the case for a higher CPI becomes much clearer - even if OER gains stall.

OER (Owners Equiv. Rent)

We talk more about energy prices below and discussed them extensively in the last Redeye Macro Note. With energy prices now on the move – that will play an important role for the summer & especially later in the summer as we assess the breadth and impact of tariffs on price levels for consumers.

Trident & Ozone

With Trident - we’re turning our leading macro perspectives into action. Learn more about the Trident I Global Macro Fund below:

Access MacroEdge Ozone for two weeks and never miss a beat on our reports, research, data, and more:

Geopolitical Tensions

RE: Taco and trade, markets are really not reacting to Trump’s ‘tougher talk’ regarding trade. Trump cited a deal being made with China in the morning - though the effective rate remains up to 55% with China on their exports to the United States. The US-China talks in London produced limited progress - and Bessent noted that, saying a deal could take years. A framework involving rare earth minerals and student visas was agreed upon, but there was no breakthrough on structural issues.

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.