Midweek Macro Note: H1 Operational Review, What's Next for MacroEdge, Equity Market Bonanza Rolls on, NFP Preview, Vision Note

In this Midweek Macro Note - the team explores the euphoric rise in valuations, what's ahead for the employment markets, our newest offerings at MacroEdge, delivers a Vision Note, and much more.

(@DonMiami3, MacroEdge Chief Economist)

Good Wednesday evening MacroEdge Readers and Community,

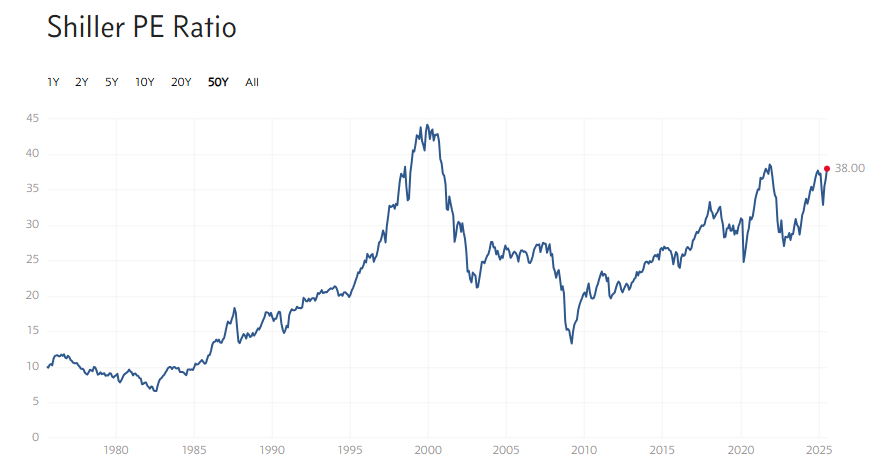

This evening we’ve got an operational update regarding what’s ahead for the second-half of the year, as we’ve now turned the corner into the summer months, and look towards a very busy Q3. Since the April market lows - equities have continued to embark on a ‘riskless’ campaign - taking valuations back to their third highest level on record (using CAPE - our preferred measure of valuations) - and from a broader valuation perspective, the second most overvalued equity market on record.

The shift from K2 - as we described conditions in February - to the descent - to the re-ascent and enablement of an equity melt up by policy makers, aligns the current equity market conditions to the 1999/2000 environment.

The question that we continue to receive is the age old question of ‘is this time different?’ or are we truly in a ‘new paradigm’? With fiscal policymakers prioritizing short-term gain over short-term pain, not looking at the longer term consequences of their actions, currency debasement, and reckless spend & print campaigns – timing again becomes more complicated in these environments. The rally of the last several months has other similarities to the 2021 mania action we saw - especially with some of the recent IPOs in unprofitable garbage going sky high as soon as they debut. Gravity becomes an eventual reality – but for now – the only way to not step into a freight train is to hedge downside while staying highly in tune if high beta continues to outperform. Value now is increasingly difficult to come by (which is why the questions above are becoming more prevalent) - though there will be plenty of opportunity in the 2nd half of the year to seek out returns & outperformance.

With that being said, we’ll dive into the updates on all things MacroEdge.

A Look at the First Half of 2025:

We enjoyed continued growth in the first half of 2025 thanks to our strong reader base and online community. MacroEdge articles on Substack have been seen by nearly 500,000 people, and we enjoy almost 7,000 readers on the platform. MacroEdge Radio continues to be available on our YouTube channel, and our X surpassed 48,000 followers as of yesterday, 7/1. Our focus on the second half of the year is to really expand out beyond our core base of offerings that is Ozone and Vision, and branch out across the nation through Transform, Economic Advisory + RESights, and get our new Macro Briefings & AlphaSights Reports in front of thousands of business leaders across the country.

What’s New for MacroEdge:

We’re working with our team and infrastructure to continue expanding into the second half of the year. One of the most notable transitions we’ll be making is in growth of our new offerings, which range from professional services offerings – to tailored research, and much more. The new MacroEdge organization structure is broken down into three smaller divisions: Economic Advisory, Transform, and Research.

With Research, you’ll continue to find Ozone/Vision – and there will be no change to our brief Macro Notes we put out anywhere from 1-3 times per week. Under Research will be the all-new CEO Macro Briefings and AlphaSights + Solutions. CEO Macro Briefings are designed for business leaders looking to get an understanding at cyclical trends impact their industries directly - and the offering is geared towards those in those major cyclical sectors like trucking/freight, real estate, energy, and more. AlphaSights + Solutions are designed for funds, wealth management firms, and individual advisors looking to get our full-depth coverage and analysis of equity markets. This investment research offering will give you the insights needed for quick decision making, to stay ahead of - rather than behind the trends. From day 1, MacroEdge has been at the forefront of setting and identifying trends, rather than following them. Learn more about our Research division below:

With Transform - we’re engaging with companies at the ground level to deliver tremendous enterprise impact. With nine core Transform solutions, our discovery process identifies what’s working, what’s not, and how we can bolster your business for a world moving at the speed of light. From development of a cutting-edge technology solution, to optimizing data, or implementing the AI-tools required to keep you ahead of your competition - our Transform team is equipped for success around the globe. Learn more about MacroEdge Transform below:

Economic Advisory enables your enterprise to navigate everything from the macro to the micro, leveraging our full range of capabilities:

Customized macroeconomic insights

Strategic guidance through market cycles

Data-driven decision support

RESights expands on our Economic Advisory division, offering tailored real estate intelligence and solutions to drive strategic clarity and measurable outcomes. Built for homebuilders, CRE operators, construction firms, trades, and investors, RESights delivers actionable, tailored insights, and hands-on support to enable to your success. Learn more about Economic Advisory and RESights:

MacroEdge is now:

Ozone/Vision

CEO Macro Briefings

AlphaSights + Solutions

Transform

Economic Advisory & RESights

Media

Under our three divisional umbrellas: Research, Transform, & Economic Advisory.

Keep an eye out for the first edition of AlphaSights, the preview to what we’re expanding upon there – as well as with CEO Macro Briefings. For any Transform or Economic Advisory/RESights related question, you can inquire directly through those respective pages on the MacroEdge website. By the end of July - everything will be up & running for these divisions, and expect to see us push into the world of video creation and more.

NFP Preview

As highlighted on Sunday evening, the labor market continues to track a gradual cooling trend, and signals are not yet pointing toward a snap in the numbers - though the ADP private payroll print came in much cooler than expected.

Given the trend - on a seasonally adjusted basis - I am looking for something in the ballpark of 78.4K (90% CI range of +20K to 136K) - and expect to see federal government job cuts slow now through the end of the year as DOGE has been shut down. Outside of that - we also saw job cuts tick down in June on a y/y basis - but slack continues to grow in the employment markets. A negative print would really send rates spiraling, though it remains the unlikely case given the data and layoffs have not had a ‘snap’ moment yet - the slow bleed has been more like the early 90s recession, coupled with poor demographics for broader layoffs. A print >125K means a 10Y likely back above 4.3% - though with what we’re watching for in residential construction employment, speciality contracting, and more tomorrow - that remains the other outlier on the opposite side of the equation for now. Expecting U3 at 4.3% tomorrow given the trend in claims and job postings, which would also likely be a new cycle high.

Inflection Point for Rates

Rates - both short and long-term - are at key inflection points, which matter given the complexities of the current macro environment.

The 10Y has remained in a wide range since 2023 and the cooler economic prints of late resulted in a small pullback in the 10Y - which finds itself at the ‘slow or go’ level again. Interesting today, was the fact that the employment data came in much cooler than expected and the 10Y moved higher alongside precious metals - and more importantly, oil.

If the nonfarm data comes in cooler than expected tomorrow, the 10Y will likely fall back towards the lower end of the range.

Note the pop in oil today, as well, off of a key level. The move tomorrow may be the determining factor in the short-run of a cut as soon as this month, or it may mean cuts are held off to the expected September date, and there’s a long time from now until then. The odds of a rate cut for July are underpriced even with inflation pressures having accelerated (ex-OER) and odds could be boosted to a 50/50 scenario if NFPs come in cooler than 75K tomorrow.

MacroEdge Vision Update July 2, 2025 (@SixFinance, MacroEdge Head of Research)

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.