Midweek Macro Note: No July Cut, The Passive x Retail Mania Marches On, MacroEdge Vision Note, MOUs

In this Midweek Macro Note - the team explores the explosion in investor margin debt, discusses the mania-like price action that can be compared to... Zimbabwe, delivers a Vision Note, & much more.

(@DonMiami3, MacroEdge Chief Economist)

Good Thursday morning, MacroEdge readers and community,

This week has been relatively quiet as we steam our way through mid‑summer. I’m finally back in my usual time zone for the next two weeks before another venture out West for client visits in California, Arizona, and Utah. Travel can really start to wear on you, especially with flying and constant time changes. It’s nice to be settled for now as we prepare our first office location for operation, with a second not far behind. Physical locations will allow us to host clients on-site rather than vice versa, and as we continue to scale, they will enable us to expand our relationship networks exponentially. We continue to ideate and brainstorm on new ways to connect with communities, such as through various branches under the ‘MacroEdge Social Club’ label - and if we see you at an event through summer or later in the year - don’t be shy

The President is set to visit the Federal Reserve today in a symbolic statement of opposition to the $2.5 billion scheduled renovations on the Fed building. That visit comes one week before the Fed is set to hold rates for another two‑month period. The hold means the next decision will arrive in September, and markets are leaning toward a 25 basis‑point cut depending on lagged tariff impacts, yields, and employment conditions between now and then. A cut right now is unjustifiable, given that financial conditions are near post‑pandemic levels after the Fed and Congress supplied unlimited dollars to the economy. If M2 equals inflation, these loose financial conditions will prove problematic at some point, but there is no clear pivot signal yet as negative divergence signals and declining volume and liquidity at these levels become more obvious.

Six & John have great additions for this very early morning edition of the Midweek Macro Note and I’ll briefly discuss the 10Y and why rate cut odds for July remain so low, the passive and retail ‘clown parade’, and the ‘bifurcation nation’...

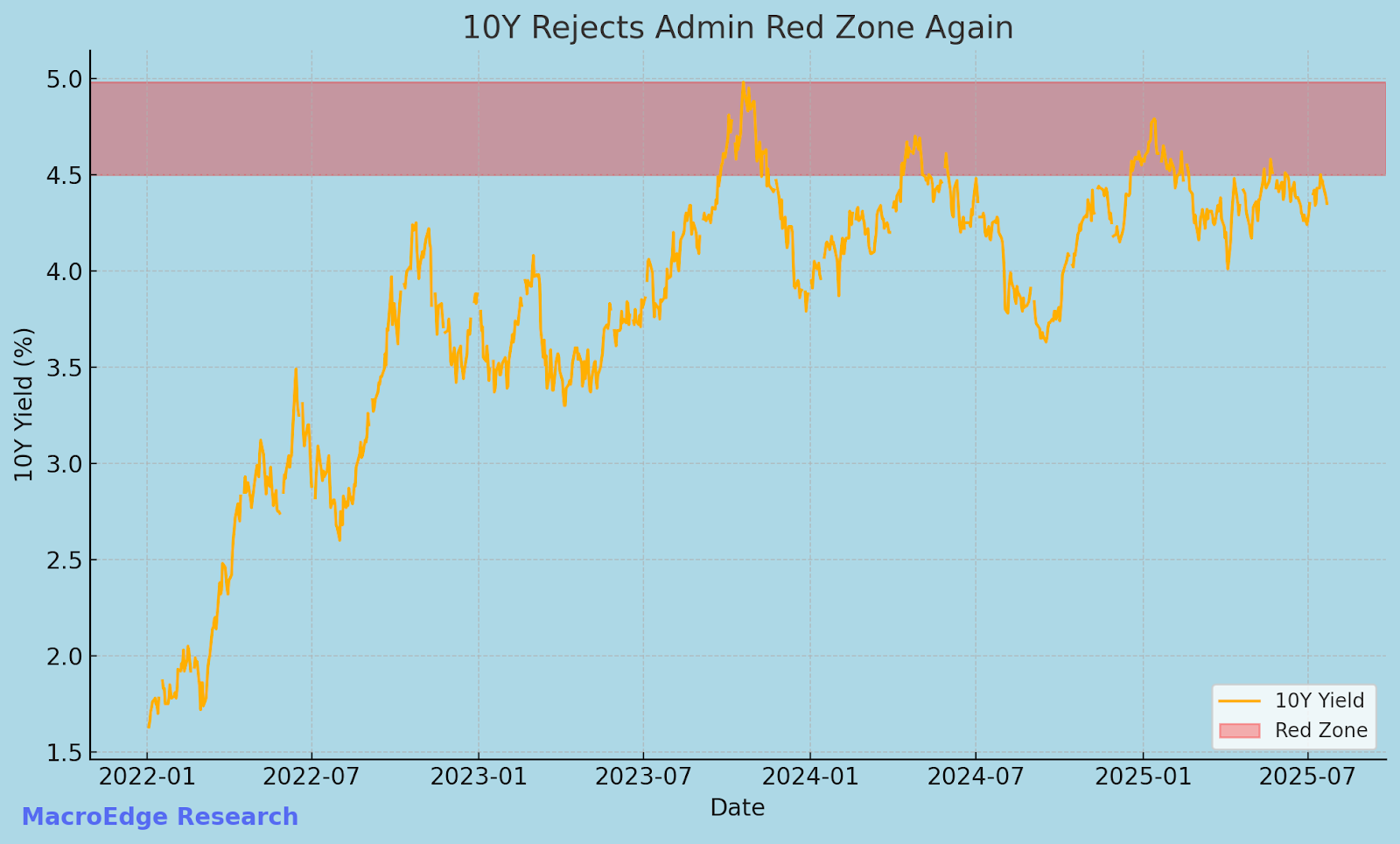

10Y Yield Still Higher Than Admin Wants It

Given the rhetoric of Pulte, and what will likely continue tomorrow - the Admin wants low rates (and especially lower mortgage rates) and they’ve been struggling with the latter. Existing home sales volumes ticked back toward a cycle low today, and that’s problematic from the Admin’s perspective. While yanking the short end lower is not a solution to high rates, when Powell’s term expires, we are likely to see the Fed and Treasury merge into one for a period of time.

Passive & Retail Clown Parade Marches On

Since the April put on markets as bonds held on for dear life, we’ve seen a rally larger than both price action seen in 98 and post-2020 (so very impressive to say the least). When Central Banks stepped in globally to intervene in markets, and tariffs were paused, it gave the all clear to investors in an unprecedented risk on move that has spread across global equity markets (in places like Japan & China) and even more so in the high-beta assets like crypto, which has also enjoyed large moves over the previous 3 months.

Valuations have returned to their second highest level in market history - and while real terms returns and dollar devaluation blur the actual picture for those of us that pay attention - this is a hyper pro-nominal asset price Admin, which has the RESights team on edge for how future monetary policy is enacted – esepcially post-Powell if Bessent starts acting as a shadow Fed Chair.

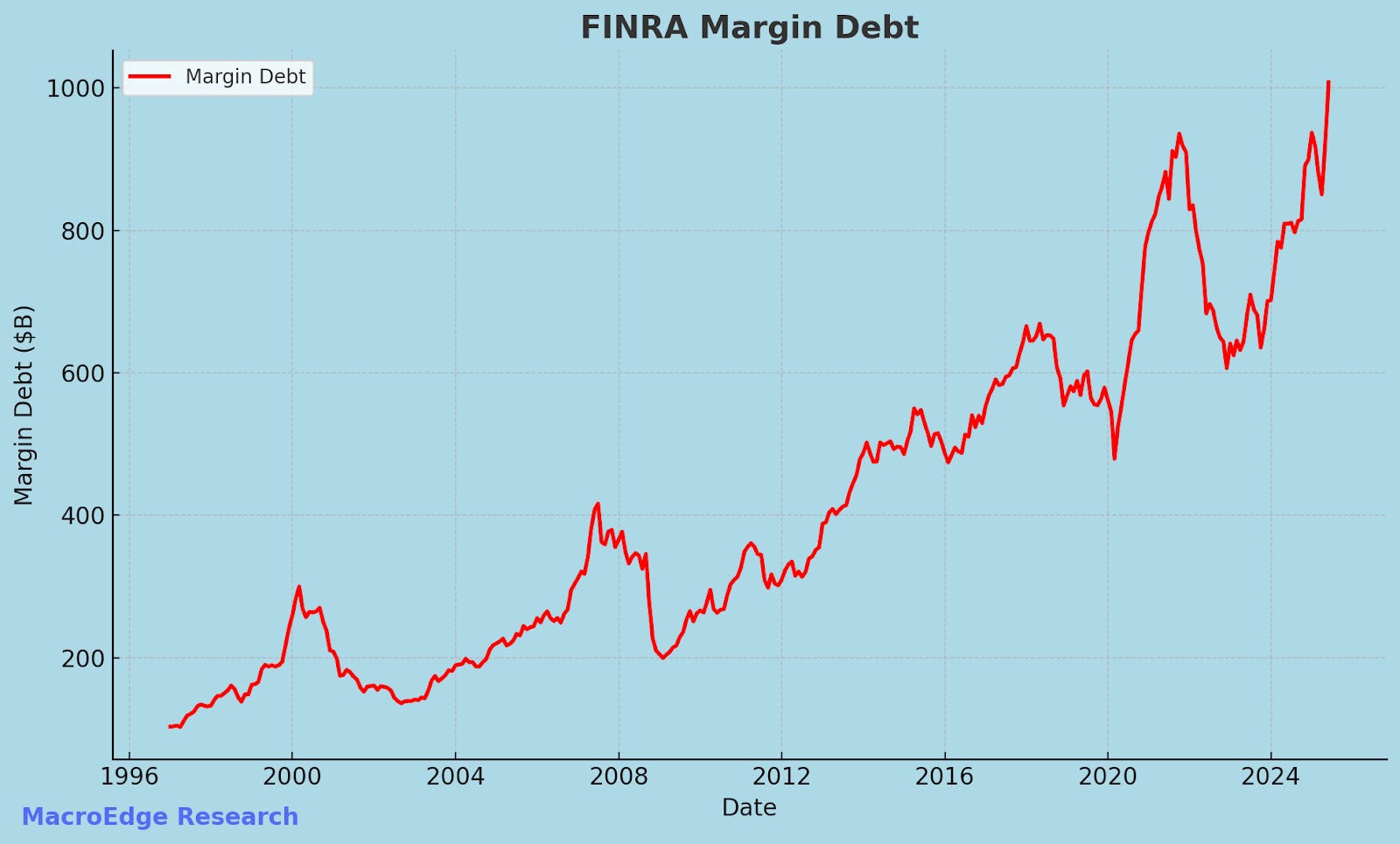

Margin debt in June topped $1 trillion across investing accounts, and the July print will likely see this figure jump another $50 or so billion based on the trend:

This margin x passive x TACO formula has created a relentless bid in equities higher - even though gains have abated slightly from the April - early July move across markets. April gave us a glimpse of how fragile markets are when the bailout element is removed, and why the bubble most continue to be protected at all costs – especially with the looming retirements of another 15 million or so in the Baby Boomer generation over the next 5 years. When you look at the

We’ve truly adopted this bizarre formula of a gerontocratic, technocratic, South Africa style economic model – and the long-term consequences of this will be dear, even though we can continue to sip champagne and chat about incredible returns over happy hour for the time being. Until clear conditions present themselves, it’s still not advisable to step in front of a freight train of the above conditions - though it becomes cheaper by the day to acquire left-tail hedging, in the event those tariff impacts do start to bite, and nominally, things start to show cracks as they did in February.

The classic volume profile of a passively driven market, with retail volume to continue pushing things higher:

Note the impressive reliability at volume in forecasting lows as well, when applying a similar standard deviation from median volume formula.

For now, the ‘party’ continues - and elements to slow it remain present but elusive, when Agenda #1 is to keep the nominal party rocking on – keep your seat the table until the music can barely be heard.

MacroEdge Vision Note - 7/24 (@SixFinance, Managing Director)

The twist steepener trade is becoming more and more obvious to me here. It is a regime expression, especially if the Fiscal (dominance) side of the mandate is enabled to oust the Fed Chair, but likely still to a lesser degree if he is replaced by an obedient Fed chair in this era of fiscal dominance. The potential for a powerful 2s10s steepener in this backdrop is being overlooked. Financial conditions remain historically loose, and inflation swaps are not just elevated, but broadly reaccelerating. A rate cut into this environment would be a policy mistake of first order magnitude. The impact on the curve would likely be immediate and violent. The front end of the curve may gravitate towards Trump’s 1% Fed Funds desired rate, while likely never getting there without substantial objection from the long end.

We are entering a phase where policy obedience by the Fed will accelerate curve steepening, not arrest it. With fiscal policy still running hot, the front end is being priced as if monetary and fiscal tools can cap inflation. The reality is, the Fed is subordinated in a regime of fiscal dominance. Rate cuts here are not easing into weakness, but fuel into a reflationary fire. Every basis point they cut steepens the curve, supports nominal GDP, and embeds further inflation risk at the long end. History has proven that terming in the weighted average maturity of the Federal debt creates a monetary easing like stimulus by increasing “money like” yield bearing assets at the front of the curve, which then frees up longer duration funds from fixed income, pushing those funds further out the risk curve, into higher yielding assets like junk bonds and namely equities. The current market is underappreciating how sticky the liquidity impulse remains. The longer the Fed stays slow to respond to rising inflation risk(which is already becoming evident via increased debt issuance and inflation swap rates rising), the more this accelerates.

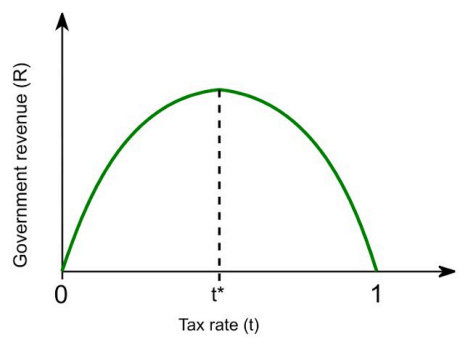

April’s tariff adjustments gave Bessent a real time read on where current rates sit on the Laffer curve, allowing for continued live adjustment.

With Bessent doing the bulk of the fiscal policy management at this point, the right question then becomes not “what level of tariffs are likely to persist, or are the tariffs nonsense”, but at what level are the tariffs likely to generate the most federal revenue. The Laffer curve shown above illustrates the concept of tax revenue maximization. This is sure to be a key framework behind the scenes giving insights into how the fiscal side of the mandate is thinking about tariffs.

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.