Redeye Macro Note: Accelerating our Enterprise, Into the Stratrosphere, Chart Blast, Videos from the Past

In this Redeye Macro Note - we discuss our accelerated enterprise and offering portfolio expansion, CAPE and valuations, potential rate cuts, long-end blowouts, and videos from the past.

Good Saturday evening MacroEdge Readers & Community,

Tonight we’ll dive into the stratospheric market moves of the past few months—and what that’s meant for valuations. Since the April lows, we've seen broad-based strength powered by relentless fiscal support. Equities have surged across the board, while many of the prior Administration’s fiscal missteps have been repeated. Cryptocurrencies, metals, and tech/AI names have all posted rapid gains in what’s felt like a “make everyone a winner” market. But beneath the surface, market concentration has only continued to narrow.

We’ll also preview AlphaSights—our next-generation equity research product launching at the end of the month. Designed to help you identify major shifts across equity, bond, credit, and currency markets before they fully materialize, the first AlphaSights Report will be sent to all current MacroEdge Ozone members and clients.

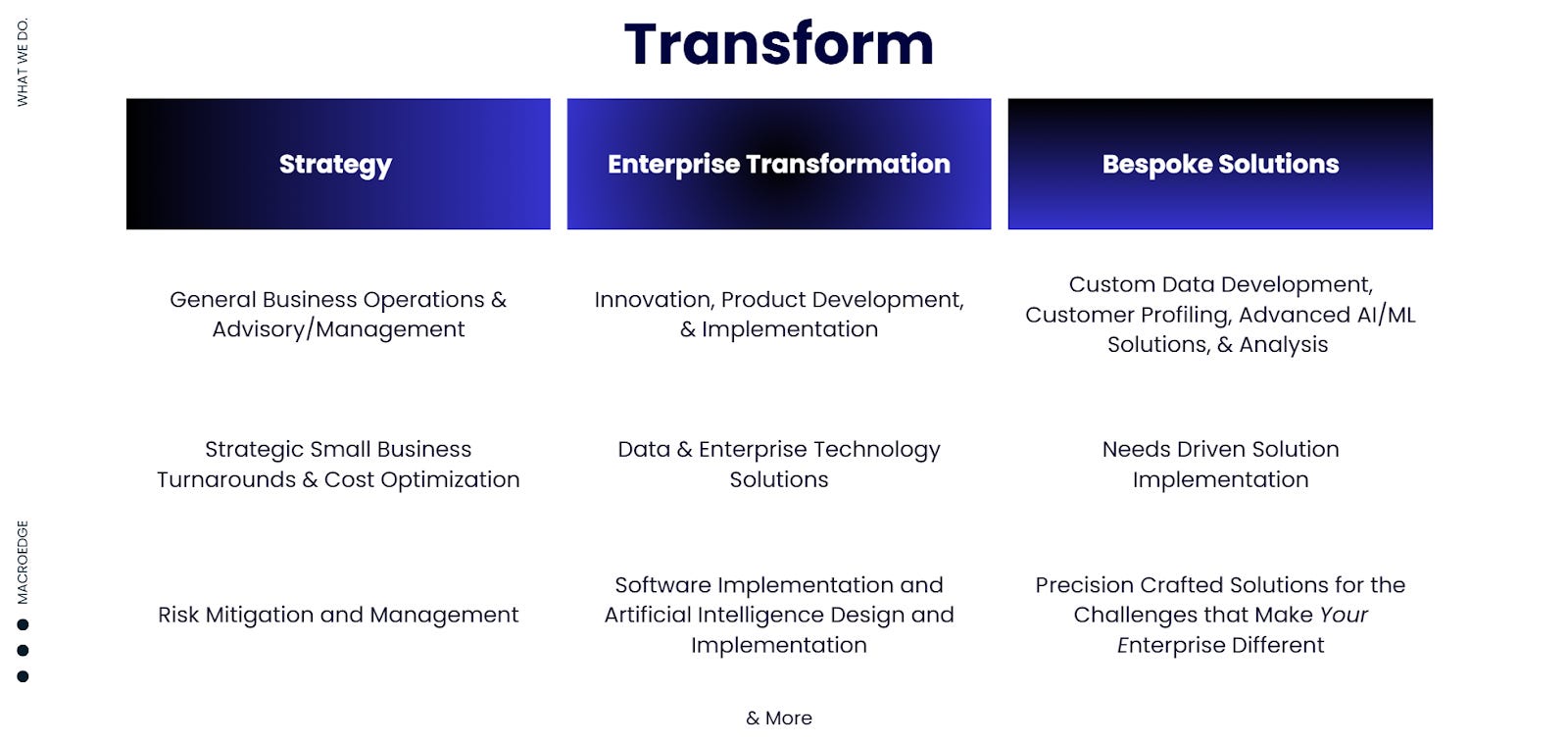

Meanwhile, we’re continuing to expand and sharpen the broader MacroEdge suite—now organized around three core pillars: Research, Transform, and Economic Advisory. The breakdown below provides a clear new way to understand our reimagined structure:

Research:

Ozone/Vision

CEO Macro Briefings

AlphaSights + Solutions

Media/MacroEdge TV

Data Team

& More

Transform – utilizing our capabilities to transform enterprises for the 2030-era.

Learn more about how we can Transform you and your enterprise, for the future of tomorrow:

Economic Advisory:

RESights - implementing Transform solutions, tailored economic advisory, and more – through this offering

Economic Advisory

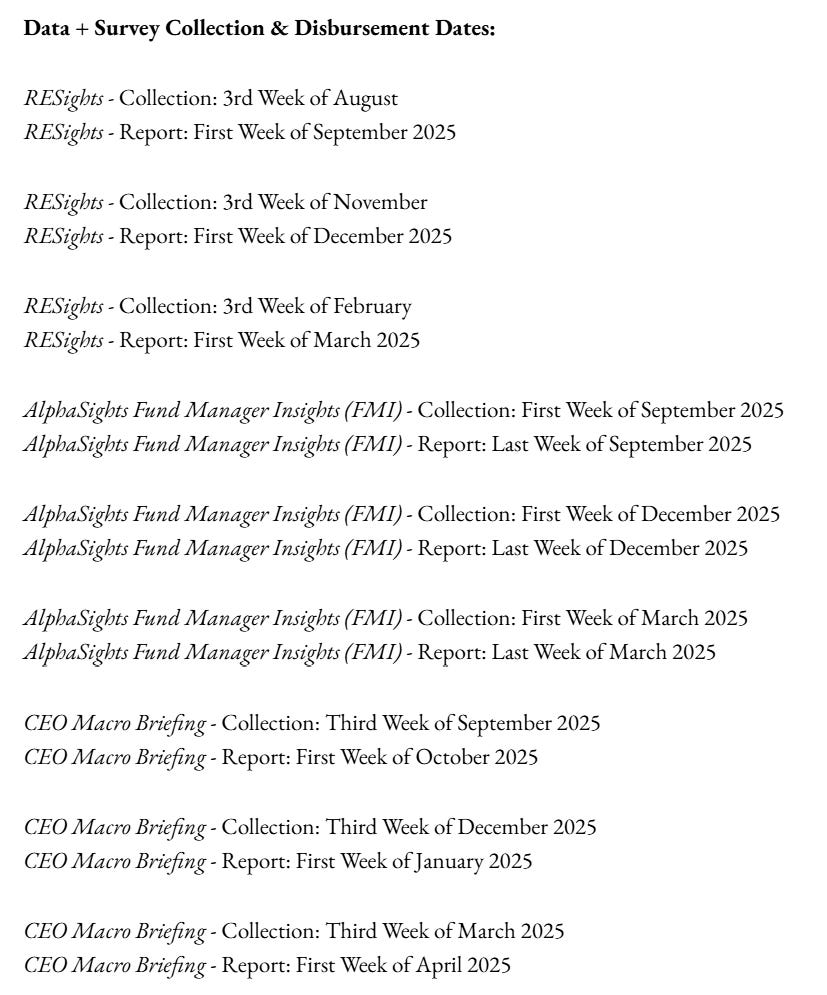

From a qualitative/quantitative standpoint - we’re pioneering three new core surveys – our MacroEdge Fund Manager Insights Survey (FMI) - our RESights Intelligence survey in the Sunbelt, collecting and compiling data by region across sub-sectors within the real estate industry, and our CEO Macro Briefings survey. If you would like to participate in one of these surveys and become integral to our nationwide data collection infrastructure, email: Don@MacroEdge.net

Release dates are below:

Our goal with our updated product and portfolio mix is to continue to develop into a leadership position in the financial and economic landscape - now with transformational service offerings available to enterprise leaders, an expansion of our insights into the pulse of macro/micro data across the economy and its sectors, and a reinforcement of all of the things we’re already excelling at.

Note that a website overhaul will be completed in the next week or so - impacting the Client Portal, home page, webpage categories, and more.

CAPE

A lot of echoes from the 2000-era to go around - with valuations and speculation pushing their highest levels in recorded history:

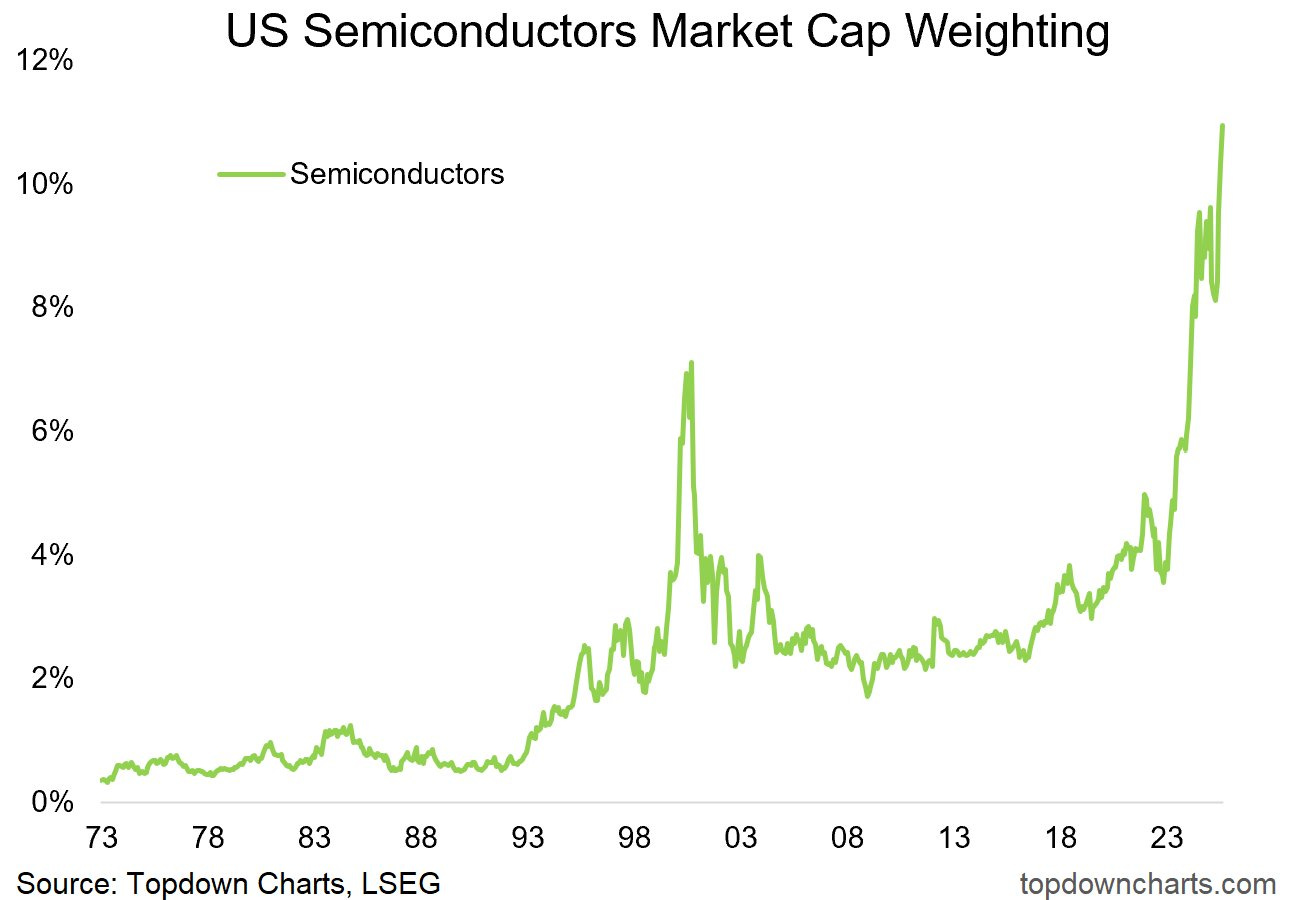

While some of that might be skewed by our current form of ‘Modern Monetary Theory’ - it’s always easier to profit from the trend rather than protest it… Exploiting opportunities in the current monetary regime involves seeking out the ‘fair’ or ‘undervalued’ names rather than those that have already been juiced to the max. The AI/semiconductor trade picked up its momentum with vigor after the brief tariff panic earlier in the year:

Market concentration has continued to narrow - with names like Nvidia by itself now accounting for almost 10% of the S&P… If this trajectory continues, we’ll soon see semiconductors alone accounting for over 12% of total US market cap…

Continuation of the Same

While we can certainly cherry-pick differences in policy from the last decade - we’re seeing a lot of the same from this Administration as the previous three (including during Trump 1).

Into the Stratosphere with Rate Cuts?

With deregulation and the continued setup of a Federal Reserve that is more pro-rate cut, and an Administration that may induce the first quasi-form of yield curve control that we’ve seen in the United States - there’s a lot of opportunity in value to capture the themes in fiscal and monetary policy that we’re seeing.

Valuations have three pathways now - continue to expand higher in a 00-scenario which eventually sees higher inflation and a Fed that puts an end to the speculation with another rate hike at some point. The Japanese outcome means no limit to valuations here - and a total disconnection from reality across the board from a broader asset class lens (ie: things like real estate resume thier climb if rate cuts are induced, even against the will of the long-end). The third outcome means a meaningful slowdown of the economy - which for the asset class means there would have to be a sustainable drop in asset prices (namely the liquid ones like equities). Though we’ve seen a slowdown in equity acceleration in the last few weeks, we’re not in an environment that encourages anything beyond left-tail hedging until broader distribution and weakness appears - especially in the crypto-sphere. Speculation right now is immense, and if the stars align as they did in February, then we’ll call them out.

Sectors set to potentially benefit in shorter-term moves in the event of potential aggressive easing by the Fed:

Homebuilders

Mortgages drop, demand surges. DHI, LEN, TOL go vertical.Regional Banks

NIM expands if the curve steepens on the short end. Loan books grow.REITs

Cap rates compress, financing costs drop, yields look more attractive.Consumer Discretionary

Credit flows easier, big-ticket items see a lift—autos, travel, durables.Utilities

High debt loads benefit from cheap financing. Dividends get re-rated.

In addition to that – if we see the long end blowout while the Fed lowers:

Energy

Reflation, real assets, pricing power. Oil moves, XLE leads.Large Financials

Steeper curve = better lending spreads. Think JPM, MS, BACIndustrials

Growth trades, capex cycles, defense and logistics. Lockheed to CAT.Materials

Input pricing strength and global demand tailwinds. Copper, steel, chemicals.Aerospace & Defense

Long-cycle contracts, safe budget priority in a rearming world.

In non-crisis environments, small caps tend to outperform large caps by 1.5x to 3x post cut.

Fed cuts short end → financial conditions still ease, even if long rates remain elevated.

Small caps don’t rely on issuing 10-year debt—they benefit more from front-end relief.

Curve steepening is historically bullish for small caps (short rates fall, long rates hold = net tailwind).

Growth expectations with elevated long rates = reflation-lite = not toxic to all small caps.

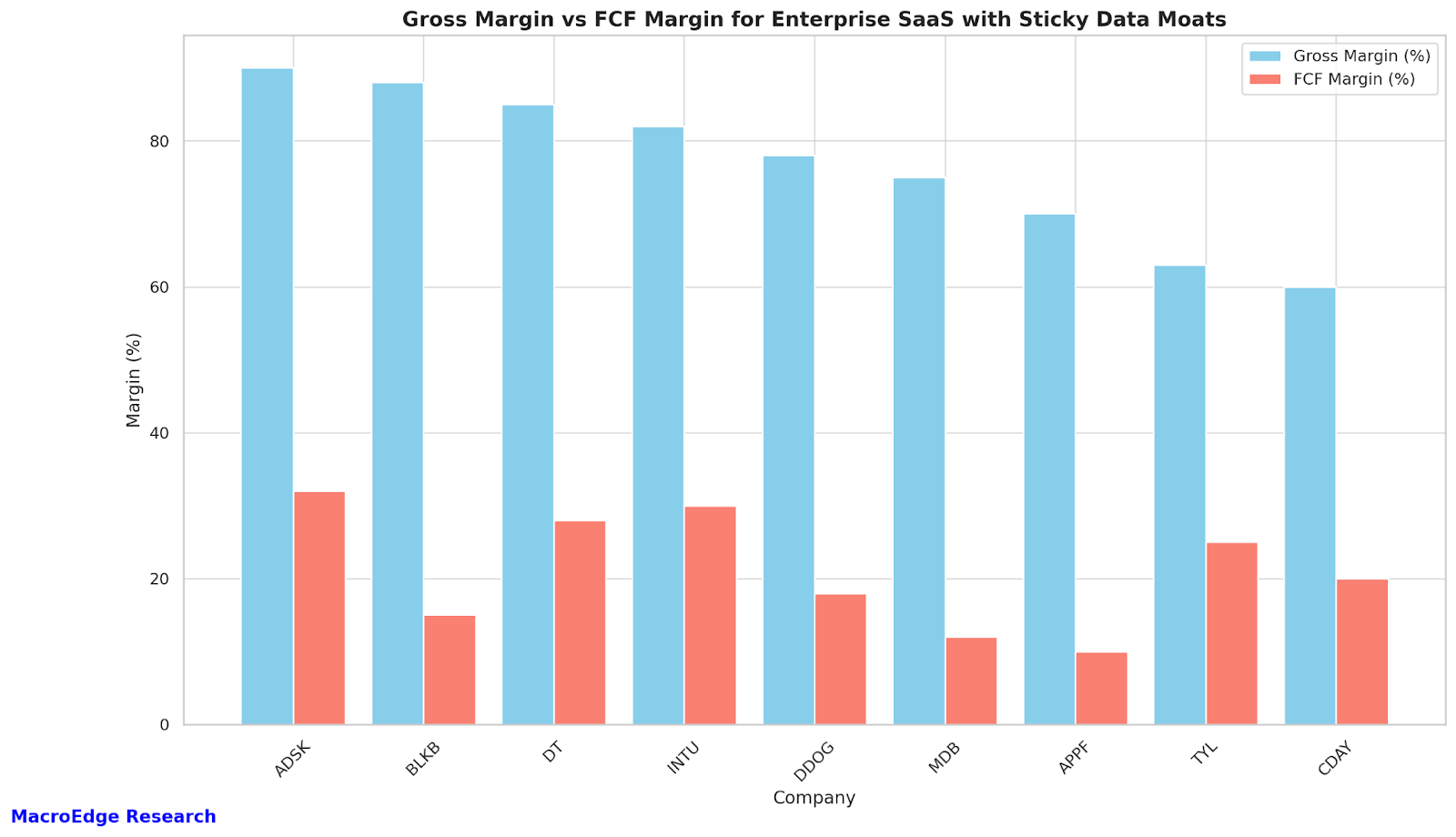

If Powell delivers real cuts and doesn’t blink, even with sticky long yields, small-cap trash will benefit: unprofitable tech, regional lenders, busted SPACs, and debt-laden cyclical names. If Powell takes the opposite approach through the remainder of his term, the opposite might just be true — but for now it remains difficult to say. We still haven’t yet seen the full impacts from the tariffs, though the fiscal backdrop remains highly supportive of asset prices. The economy is in a slowdown state - and monitoring for inflection points remains something we’re broadly in tune with – which is why we’re releasing our first AlphaSights Report at the end of the month – to cut through the noise, and deliver the insights that matter in broader trends and macro. Another theme that I continue to monitor is the ‘sticky data moats’ basket - and the leaders enjoy fat gross margins:

Unlocking the Broader Macro Trends with AlphaSights

We're unlocking a deeper understanding of broader macro trends through AlphaSights, delivering insight that cuts through noise and helps decision-makers stay ahead of what's next. At the center of this initiative is our Fund Manager Insights (FMI) Survey, which captures sentiment, conviction, and positioning at the fund manager, family office, and CIO level. This data is not only collected but translated into actionable intelligence—visually and narratively—to empower our clients.

Our once-a-month report will go far beyond surface-level commentary. It will be a tool designed to identify long-term trend shifts and asymmetric return setups, providing readers with both conviction and clarity. These are signals, not guesses, and when paired with portfolio strategy, they unlock an edge.

The effort is being spearheaded by @SixFinance, and we believe it will be nothing short of transformational for those who engage, implement, and act. The era of waiting for alpha to show up is over. The new game is reading the map before others even realize there's a terrain shift.

Later this year, we’ll launch AlphaSights Solutions, which goes one step further. It allows fund managers and investment teams to outsource real problems to our group built to solve them. From building thematic strategies to addressing today's market structure challenges—like extreme passive dominance and portfolio concentration—we're offering real support.

This is our answer to the 2025 investment environment. One shaped by liquidity, fragility, distorted leadership, and a 'partake or die' structure that punishes hesitation. AlphaSights is built for those who are still playing to win.

Two Historical Videos of TV Stock Market Coverage Relevant to This Era

(@RealJohnGaltFla, John Galt - MacroEdge Contributor)

FOR the record, I watched the entire session on the only real financial media cable channel, the Financial News Network (FNN), from 9 a.m. that morning until 10 p.m. that night.

October 19, 1987 was one of the most terrifying days in US history that I had ever lived through and watching the closing bell and market coverage afterwards was sobering; and I was not even invested in the markets at that point in time.

At about 16 minutes into the first video is an interview with legendary investor Paul Tudor Jones, who was President of Tudor Investments at this time. Listen to what he says about equities being overvalued and reflect on what is happening today.

John Bollinger’s commentary is also worth noting as his analysis of the situation was sobering.

In the second half of these videos, Ed Hart, one of the greats of financial media history offers some sobering reality to what that time was a generation of permabulls who never thought it was possible for markets to perform as they just had.

“The world is too heavily leveraged for such a quick return to reality” has to be some of the most sobering words I have ever heard.

Perhaps our current financial and political leaders might want to listen to that statement by Ed Hart and reflect on the house of cards they have constructed.

(Thank you to YouTube and the user Mr.Infinity for preserving these videos and posting them. My VHS copies were corrupted decades ago.)