Redeye Macro Note: May Labor Market Report & Widening Oil Asymmetry

In this Redeye Macro Note - we discuss the May employment data in the May MacroEdge Employment Report - and also highlight widening oil asymmetry and potential opportunity.

Good Saturday evening MacroEdge Readers and Community,

As we steam closer towards the start of summer, in just a few weeks from now, we’re going to dive into the employment trends with our May MacroEdge Labor Market Report and talk about the widening asymmetry in inflationary pressures and oil prices. With the CPI picture becoming more blurred with things like OER cooling and oil having dropped a considerable amount further, we’re seeing mixed signals about what’s ahead for CPI. What’s most likely now is a pretty defined two-tail scenario given the data we analyzed (that is covered below), where price levels across the board begin to deteriorate and unemployment rises further, or we see broad commodity and oil acceleration into the end of the year – which doesn’t mean that unemployment can’t also rise concurrently.

While Trump was largely bearish for oil prices in his first term, the situation now with domestic drilling and production highlights much more disciplined E&P players pulling supply back more dramatically than they have in the past. The ‘Big Beautiful Bill’ may provide further inflation tailwinds as it adds an additional $7 trillion in total spending to the inflation picture, though the tax cut extensions and provisions aren’t as completely stimulative as advertised. Unusual divergences from leading price pressures have been uncommon since the late 80s, which is why we dive deeper into the statistics and data below on the opportunities in the space.

On the employment report – the May report pushed forward the narrative of continued cooling in the employment market, not collapsing – a cooling that’s been taking place since the Fed first hiked rates back in March of 2022. We’re not seeing enough weakness in the major cyclical sectors yet to impact broader employment, and the demographic picture from 2020 onwards also adds headwinds to higher unemployment levels, though the unemployment level did hit another cycle high. Revisions to the March and April data were negative, and job growth was overstated by around 900,000 last year – per the QCEW. Danielle DiMartino does great work on this, and the employment data collection methodology continues to be greatly flawed. Fed Gov. Harker noted his concern on what many of us have been talking about for the last three years… there’s a lot of garbage data (which is why we originally formed to track things using alternative methodologies).

Tomorrow we’ll dive into the latest single-family trends in the country – focusing particularly on the rise in single-family inventory and cooling of prices across the Sunbelt – opportunities in the homebuilding sector related to our analysis of the industry – yield curve relationships, a 10Y/30Y bonds update – and a Vision note (also one of my favorite charts about the dollar…). At the end of June, we’ll have our first half of 2025 operational update – discussing new things about the development of MacroEdge, and our long-term outlooks, new product developments, releases, and much more.

Version 3.0 of the MacroEdge website has been pushed through with new content, fresh looks, updated product information, and much more. You can visit the refreshed MacroEdge website below:

Trident & Ozone

With Trident - we’re turning our leading macro perspectives into action. Learn more about the Trident I Global Macro Fund below:

Access MacroEdge Ozone for two weeks and never miss a beat on our reports, research, data, and more:

May Labor Market Report - Cooling, Not Collapsing

Broadly the labor market continues to soften at a near snails pace through May – with job postings continue to cool, layoffs remaining somewhat limited, and job growth continuing at a moderate clip. The data we dive into below covers those trends, and we continue to expect a higher U3 number by year’s end then we currently have – though we know that this Administration is going to intervene going forward during signs of economic weakness. The ‘BBB’ bill is one example of this - and may prove stimulative for things like WTI - which we cover in the following section.

For federal employment, we’re already likely near the decline of the total federal workforce from DOGE related cuts, as the Trump Admin begins chasing down and rehiring tens of thousands of federal employees who have had their jobs reinstated through litigation, or the Trump Admin sees the midterm as a bigger goal than containing either costs or inflation.

We added slightly over 130,000 jobs (SA) for May, slightly beating estimates, and with substantial negative revisions to March and April data. The unemployment level hit a new cycle high – revisions remain rampant – and the data below paints the picture clearly. We have seen a rebound in the hiring rate, though where we go next with rates (and oil prices, etc.) will determine what corporations due regarding their headcounts. At the same time – we know from our data that companies remain ready to shed additional jobs – though they’re cautious to do so after lessons learned from 2020, and with a rapidly aging workforce (ex-foreign employment).

Payroll growth, aggregate

Payroll growth, Y/Y slowing – and continuing to do so

At what point does this become problematic? When cyclical sectors begin to roll-over in concurrence with softer and softer headline prints. Note that prints don’t need to go fully negative for broader issues, but the

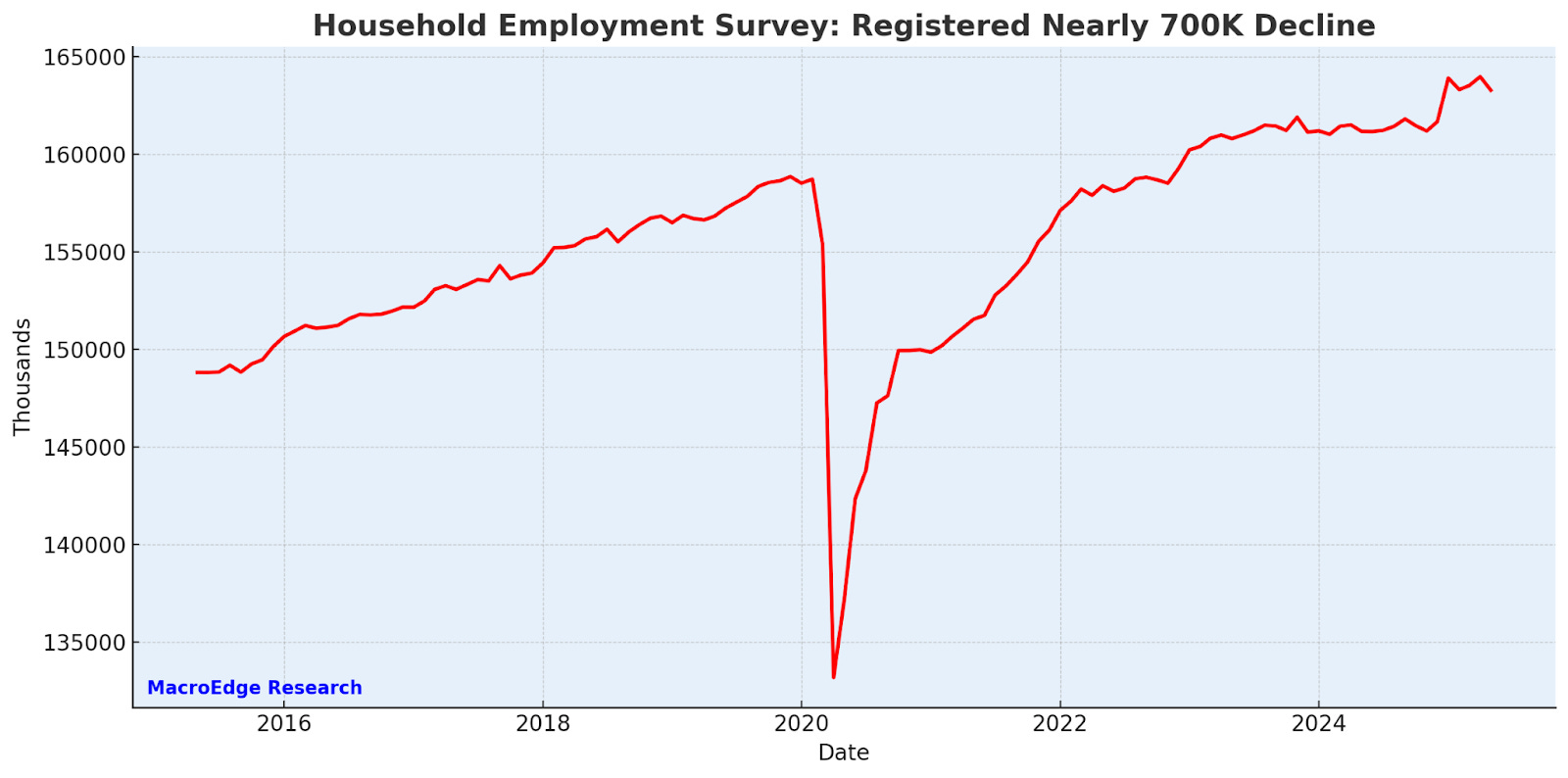

Household employment, monthly

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.