Saturday Macro Note: Feb Data Center Report Pt. 1, Macro Data Review, & Hotel Demand Cooling

In the Saturday Macro Note - we discuss the latest trends in AI/data center infrastructure with Pt. 1 of our February Data Center Report, talk about last week's macro data, hotel demand, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Saturday evening MacroEdge Readers and Community,

This evening, we’re going to kick-off our weekend deep dive with the first half of our outlined segments from yesterday evening’s Friday Macro Note. There’s a lot to cover from the past week, with some volatility trickling back into financial markets globally. Cryptocurrency markets got rocked - with leveraged liquidations rising into the $10bn+ range over a multi-day period. In addition to that - technology equities continue to struggle to move out of their multi-month range. Japanese equities have surged higher on a weaker yen, and our global bubble gauges - the IBEX, N225, KOSPI, and TSX all remain supportive of the current bubble environment we find ourselves in.

This environment has come under more pressure in the United States - and I expect that it will get even more difficult through the year for things like the AI/data center trade as new regulations, postponements, and ground-up efforts to stop the massive construction pipeline get underway. Below, we’re going to cover the latest developments through the beginning of the month, and in three weeks we’ll have the second update for the month of February. Six states now have active bills to be voted on that will serve as outright bans on the construction of new data centers - some with multi-year windows… like the bill in New York introduced yesterday that calls for a 36-month moratorium on new construction:

In the Saturday Macro Report this evening - we’re going to review the macro data published over the past week - including on JOLTS (delayed release from December), highlight Pt. 1 of our February data center report, look at trends in the hotel sector in this ‘i-shaped’ economic dynamic, highlight air travel data and equity performance, and briefly talk about what we’ll be covering tomorrow in the Weekly Macro Note.

On Friday, we saw a rebound across the board as the yen weakened, and small caps & crypto led the brief bounce higher. Oversold conditions are now present in many cryptos, but oversold conditions are often where we can see further downside extensions. Given the gap still to measurements like the balanced price, downside continuation seems probable after a period of time of consolidation. The equity markets continue to ‘churn & burn’ as highlighted in the macro note. Let’s dive in.

Not a MacroEdge Ozone subscriber? All of our research, reports, data, portfolio strategy, and much more is located only on Substack. Try MacroEdge Ozone for one week below, and transform your data ecosystem with Ozone:

Macro Data Review from the Week

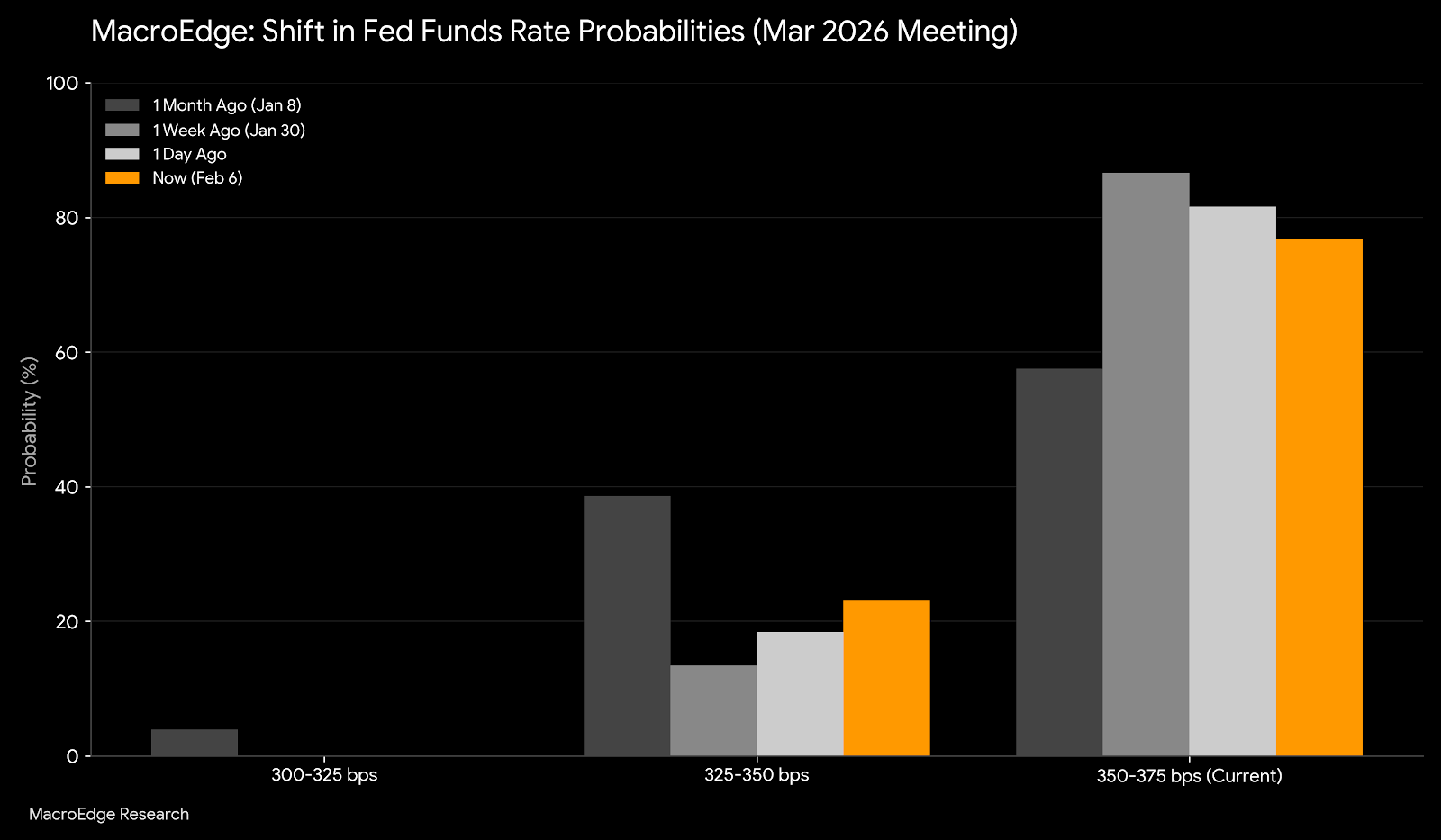

Over the last week, we got some interesting macro data. The bulk of the employment data landscape continues to highlight a cooling labor market - and the JOLTs report sent rate cut odds lower. Rate cut odds for the March meeting now stand at about a ⅓ chance, after being down to as low as 10%.

The Trump Administration is going to want a cut in March, so they’ll need much softer data still to secure one. With Warsh now in the confirmation pipeline at some point in the next few weeks, we’ll continue to monitor market performance with a potential Warsh pick. While online pundits are calling Warsh a hawk, he really just does whatever is required from a policy standpoint, depending on the period of time he’s involved in rate decisions. This means predictability in his decisions, which is something that investors love, and they likely won’t get under the last few months of Jerome Powell.

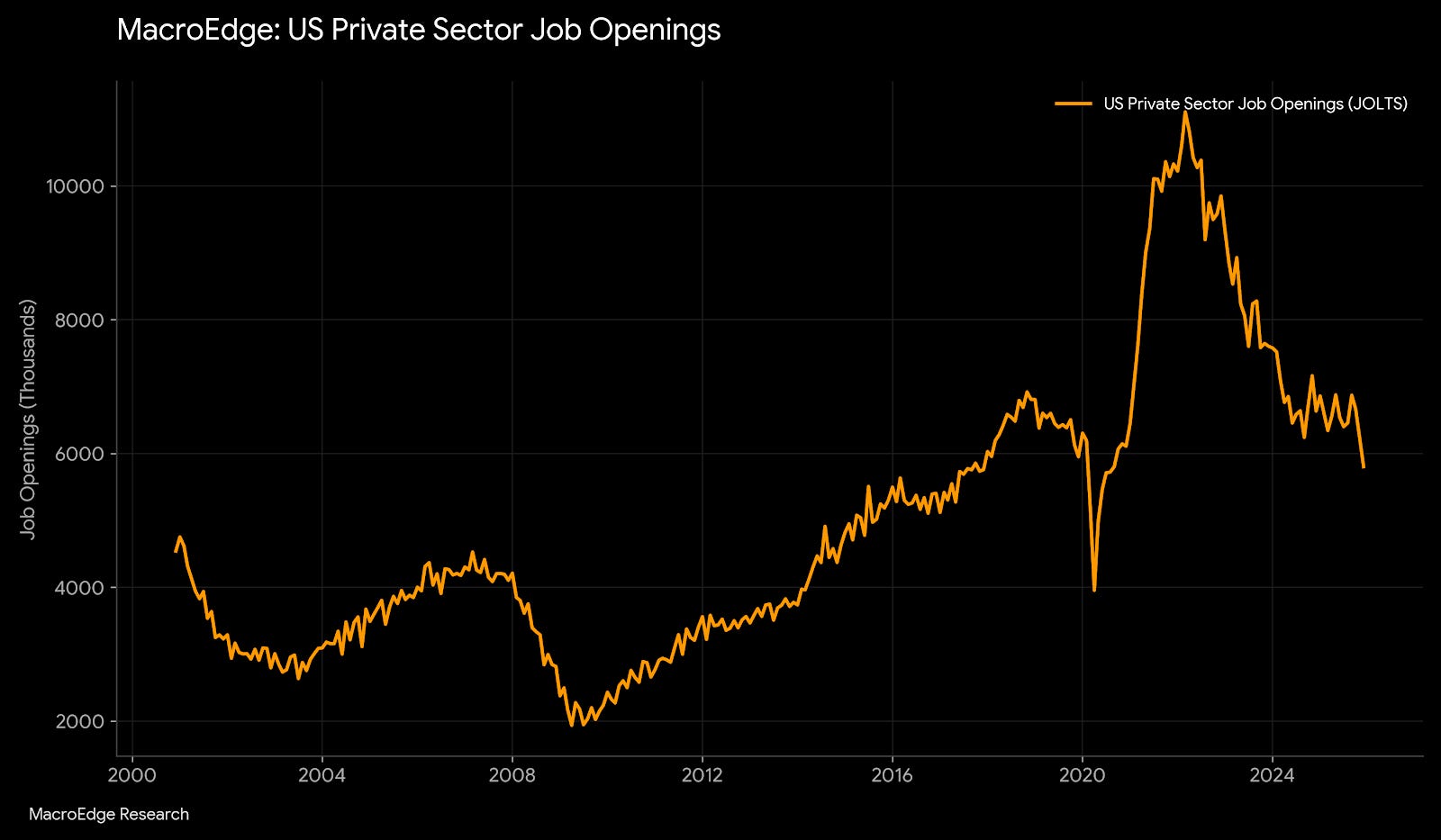

Job openings highlight a labor market that is in trouble, with private sector job openings continuing to plummet:

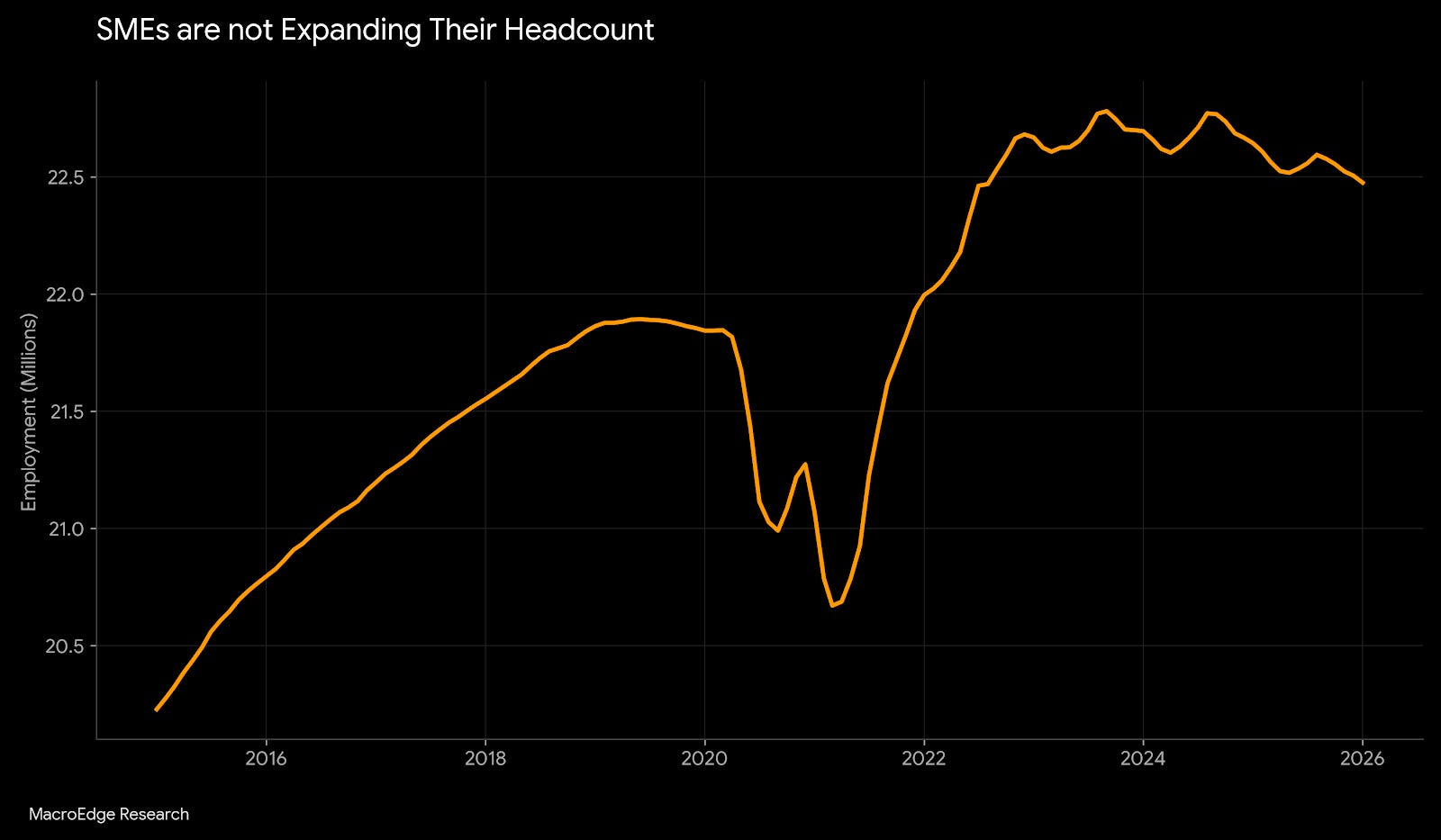

Government job openings are also bleeding lower. This labor market is still softening, and new grads/younger employers are coming into a very difficult labor market environment. On top of that, they’ll be competing with older, more qualified workers for entry-level positions as the white-collar side of things continues to soften. While there’s not a direct 1:1 correlation between JOLTs and U3, we should continue to note softening employment conditions. The hiring rate also remains near historic lows - and low hiring and low firing is a toxic combination for real labor market growth… some of this might be due to the broader hollowing out trend of our labor force that’s underway, but if companies are not hiring - saturation is going to continue to grow on the labor supply side, which will bleed into things like lower wages (Nebraska introducing a lower minimum wage, lower salary caps being permitted at certain roles at the state level, and much more).

Indeed Job Postings (live) have resumed their downward trajectory after a brief seasonal bounce:

ADP private payrolls continue to point to a very weak hiring environment:

With the government reopen now, it’s going to take a week or two for them to cycle through what data is actually available for the January print, make adjustments, and get it published. I continue to believe there is little efficacy in any initial print, though it really depends on the month and what’s being put out by the BLS.

In the ISM data, we saw a bright spot in the manufacturing data, though some of that may have been a 2026 pull-forward. This is the first positive print here in over a year.

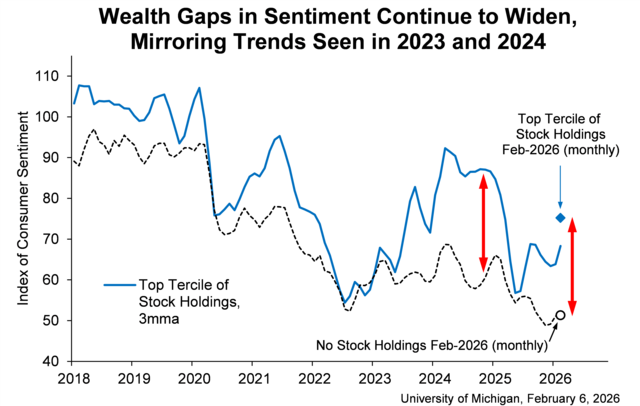

Consumer sentiment data from the UMichigan survey series also moved higher:

February Data Center Update Pt. 1

For Part 1 of our February Data Center Update, we’re going to briefly discuss trends so far this month. We now have six states with active *potential* legislation against data centers - and concerns from water, to utility cost, and more are mounting against the data centers. While movements continue to largely be local and grassroots, we’re starting to see state-level and a select few national-level politicians and leaders take positions on the matter.

(Continued below: February Data Center Update Pt. 1, A Fresh Look at the Hotel Sector, and More). Subscribe to MacroEdge Ozone to get all of the latest from our

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.