Weekly 6/1 Macro Note: May Employment Preview, Bottom for Inflation, Summer Vision Welcome, Nikkei, Defense, Robotics, AI, Power to the Trade War

In this 'Welcome to Summer' Weekly Macro Note + Vision Investment Research report - the team dives into numerous sectors, opportunities for the rest of the year, macro data, and much more. #MacroEdge

May Employment Preview (@DonMiami3, MacroEdge Chief Economist)

Good Sunday evening MacroEdge Readers and Community,

This evening we’re tuning up for the first month of summer, which means more macro, more data, and a whole lot of headlines hitting the tape over the next couple of weeks here. This week comes our May employment data release from the BLS, earnings from Broadcom, ISM data, and we look ahead towards the next FOMC meeting -

As we’ve entered June - markets priced out much of the tariff fear from April - first half of May - though gains moderated to end the month of May as tariff talks under ‘TACO’ saw their pivot towards ‘TOFU’ right now. China appears to be balancing on a tightrope - trying to avoid any additional tariffs or sanctions - with its Commerce Minister (daytime China hours) highlighting that it was abiding closely by the agreements reached in Switzerland a few weeks prior. Earnings this season have been fine, as we expected back in our early April outlook. However, the outlook as we progress into the year, with multiples returning to cycle highs, remains a lot more blurred.

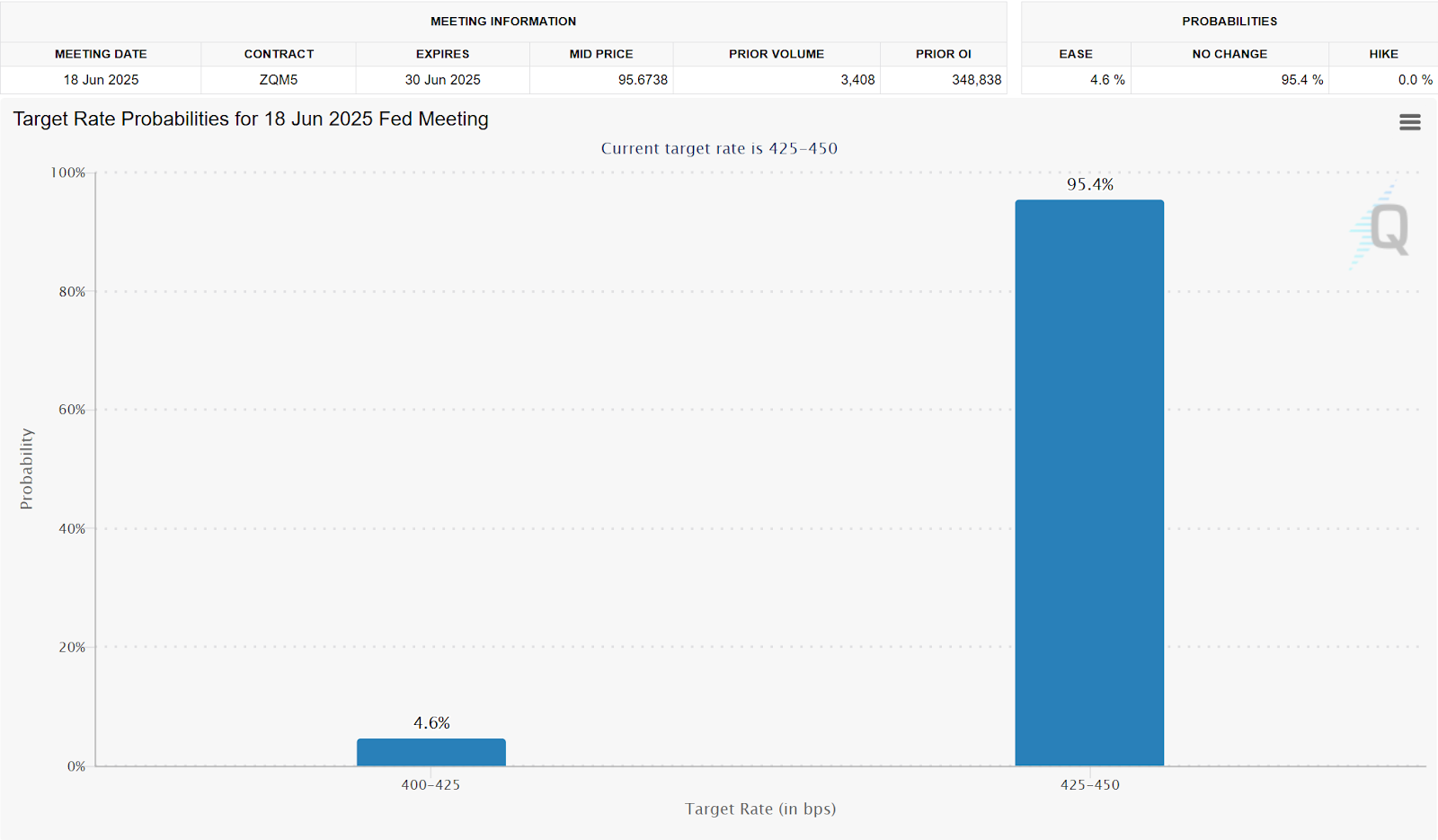

The picture remains quite complex - but we’d need a much more dovish Fed and weaker employment data to see the Fed get more aggressive on their rate cut agenda - with the 10Y largely rangebound as the ‘Big Beautiful’ Omni’bomb’ works its way through Congress getting its latest round of pork fillings for various Congressional Districts. Employment data in May (the leading data) appears again to be quite soft.

Important Macro Data This Week

Monday: ISM Manufacturing PMI, Construction Spending MoM, JGB 10Y Auction

Tuesday: JOLTS Job Openings, Factory Orders,

Wednesday: ISM Services PMI, Bank of Canada Interest Rate Decision, Beige Book

Thursday: AVGO (Broadcom earnings), Imports/Exports, Claims

Friday: Employment Data, Consumer Credit Change

Trident / Ozone

With Trident - we’re turning our leading macro perspectives into action. Learn more about the Trident I Global Macro Fund below:

Access MacroEdge Ozone for two weeks and never miss a beat on our reports, research, data, and more:

Employment Preview (May)

Labor Market Cooling Continued in May - But Don’t Expect Negative Job Growth

May is usually a positive month for employment data - though we will likely register some negative prints in temporary employment, trucking (potentially), and government employment. Broader the picture remains soft - and even moreso when you begin to break things down at the state level (especially Sunbelt + California / Illinois).

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.