Weekly Macro Note 8/24: Digesting Jackson Hole, Jaws of Kyoto, Technicals, Macro Week Ahead

In this Weekly Macro Note - the team dives into the sentiment around Jackson Hole, classifying it as slightly hawkish, talks about the 'Jaws of Kyoto' for those that follow... technicals, & more.

(@DonMiami3, MacroEdge Chief Economist)

Good Sunday evening MacroEdge Readers and Community,

As we move past Jackson Hole and Powell’s short comments (it seems like it was just 2024’s speech yesterday) - we continue to head towards fall at an ever-increasing pace. While the overall equity market picture has been one of tremendous rally since the April intervention lows, it’s been largely narrow in scope, and we’ve seen market cap concentration hit record levels in particular indices.

Times are certainly different from a fiscal & monetary intervention system, though history gives us no period to pull from where these combinations enable insanity to continue indefinitely… now that may be different from an inflation standpoint, with a September rate cut on near-lock, though there is still data that needs to be digested before I’m certain on it. There’s also a significant employment data revision arriving in early September, that we’ll talk more about in the coming weeks.

While it’s easy to say there will be continued TACOs, bailouts, multiple expansion, and intervention - the fake financial reality that we’ve created in America, coupled with dramatic data issues in how we understand what’s really going on in the economy, create rare periods to capture volatility and policy error from a body of people that are way out over their skis, yet again. We’re sitting with GFC-level delinquencies in everything but the mortgage market now, and there will likely be both CPI and broad macro implications from such data, which has been masked by a pump all assets regime from April.

On Wednesday we’ll have much more in our Midweek Macro Note, including timing on the next AlphaOne Report, so don’t miss another Midweek Macro Note with two week access to MacroEdge Ozone below:

First AlphaOne Report remains available below:

More is coming to AlphaOne, that we’ll discuss on Wednesday, including the institutional EdgeDashboard - and more, for all AlphaOne clients.

Macro Week Ahead

USA - United States of America

Monday: New Home Sales

Tuesday: Durable Goods, Consumer Confidence

Thursday: GDP (Q2, 2nd estimate)

Friday: PCE inflation (July) plus Personal Income/Spending, U. Michigan sentiment

Japan -

Thursday night/Friday

Tokyo CPI (August)

Industrial Production, Retail Sales, UL/J2A Ratio, and Consumer Confidence

Next BoJ meeting is September 17-18

Earnings this week:

With Nvidia this week, we’re likely to see some activity in volatility towards the latter half of the week, though optimism is high enough that we may remain in a distributive pattern for the time being, if earnings does surprise to the upside, and guidance into the fall/winter stays strong.

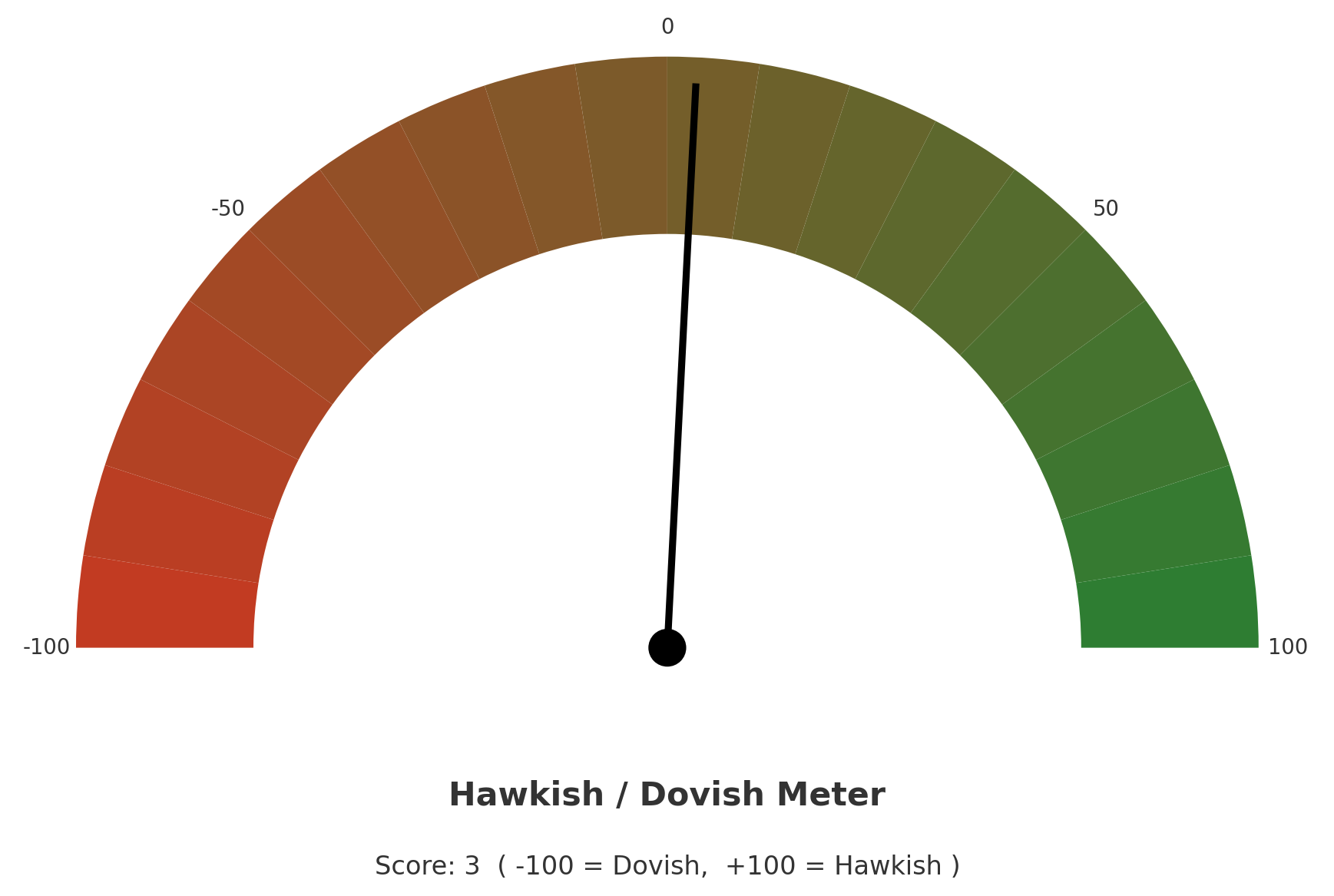

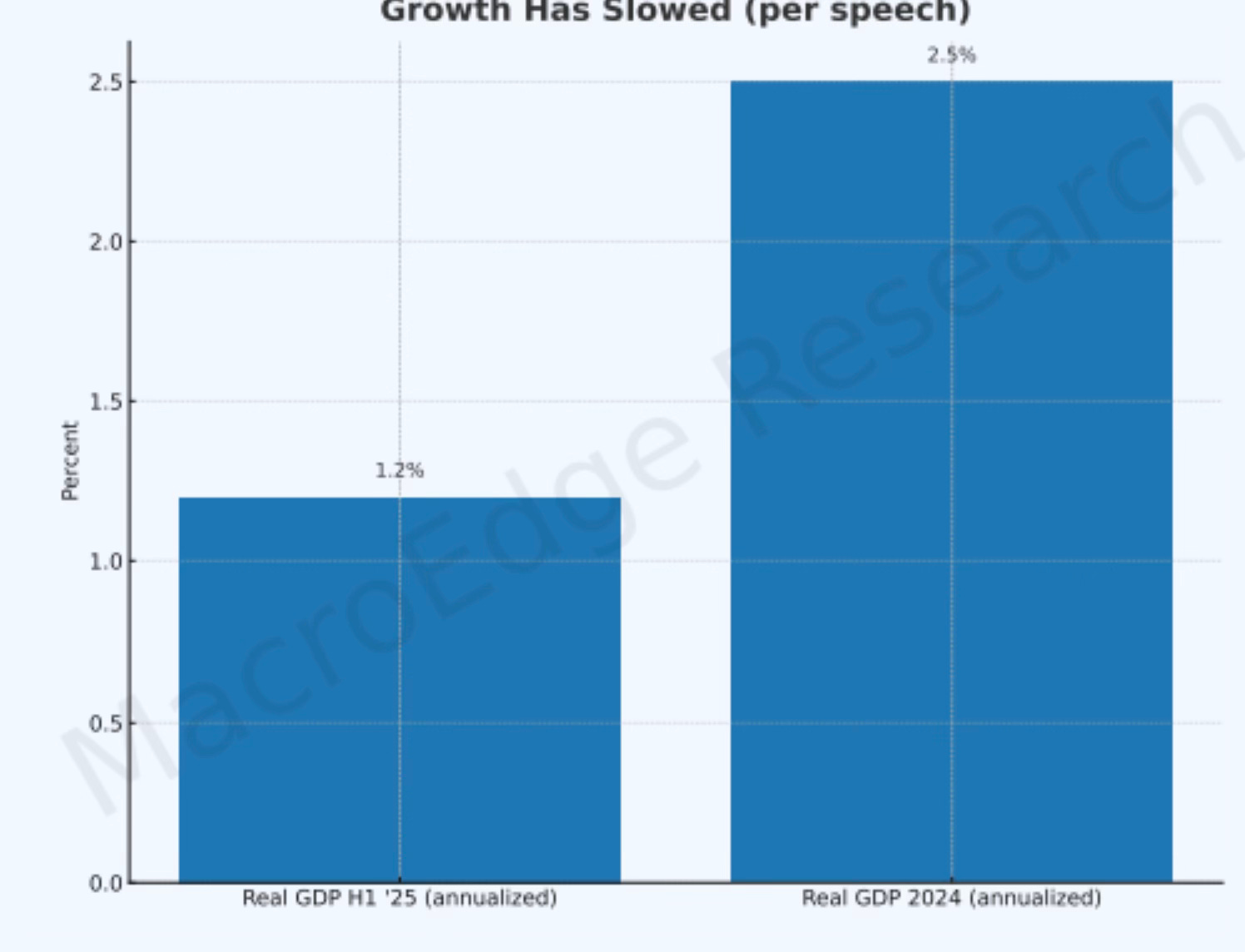

Digesting Jackson Hole - Really that Dovish?

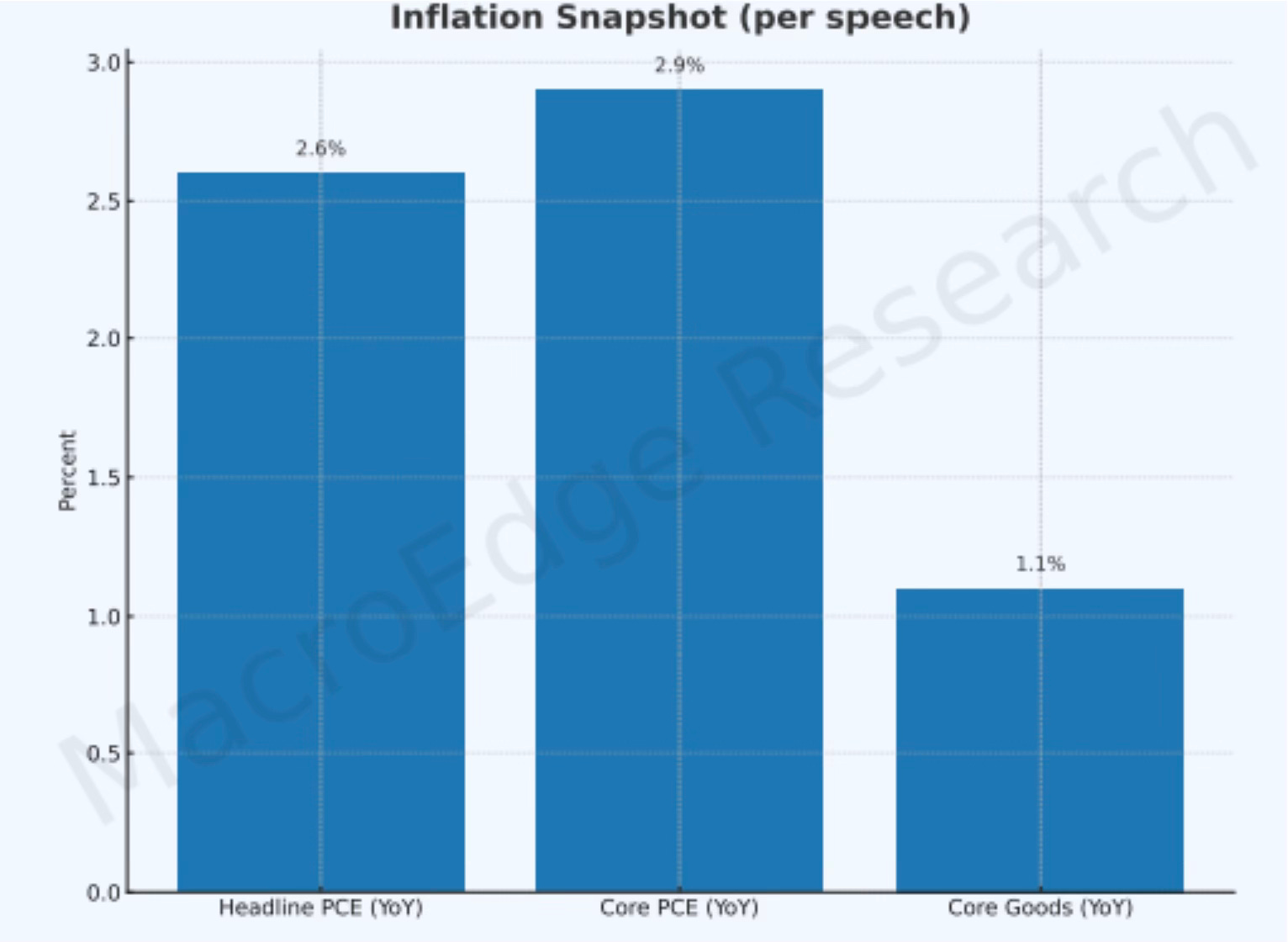

In digesting in the Jackson Hole, it really wasn’t that dovish. While it moved the needle on a September cut, that’s not necessarily a bullish development if it enables a higher-CPI regime going forward. CPI is resulting in ‘shrinkflation’, eats into margins as it accelerates, and causes great pain in the lower 50% of the K-shaped economy, something our policymakers seem to have forgotten about.

Retail and the CNBC institutional crowd alike got jazzed up by a September 25bp cut, which really doesn’t do anything at all for the economy, debt load, or real estate, if the 10Y stays anchored.

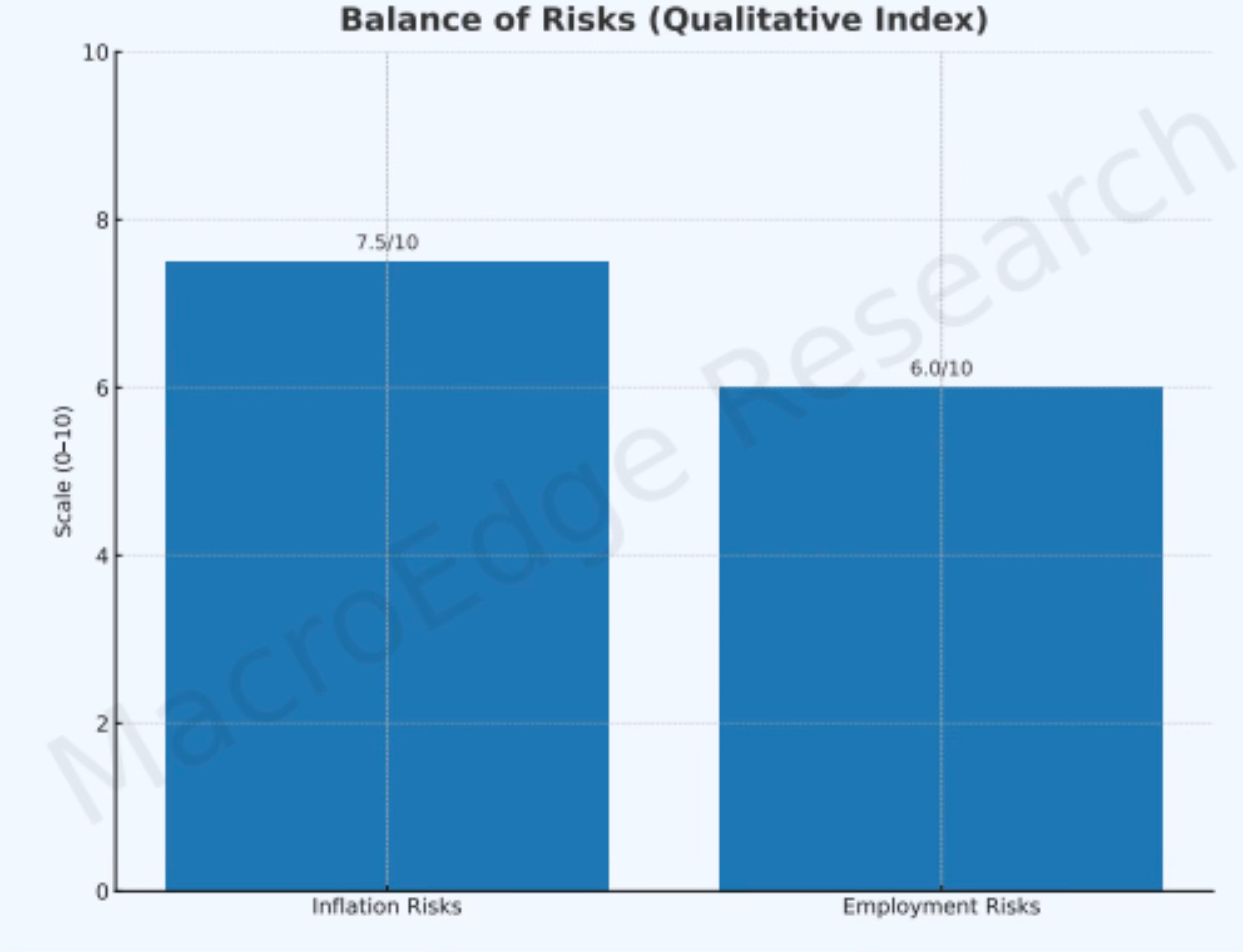

Our hawkish/dovish meter - looking at 9 factors, came out as moderately hawkish not dovish.

Technicals

As noted over the last few weeks, Bitcoin continues to be our overall risk gauge - with potential leading components to the broader high-beta environment…

Bitcoin

A large single-sell order triggered some minor liquidations in Bitcoin earlier this afternoon, with a single seller unloading about $3bn worth of coins in one block order, this particular individual or entity has around $17bn remaining in their wallet.

This negative divergence on the weekly, monthly, and three-month time frame is not a positive development for the crypto crowd - and could be signalling significant financial conditions tightening in the months to come. Rate cut fantasies about unicorns and multiple expansions, with valuations completely detached from any reality known to man & everyone from barbers to airport bartenders switching career paths to daytrading, provide signal for caution for some time in the risk markets.

Nasdaq

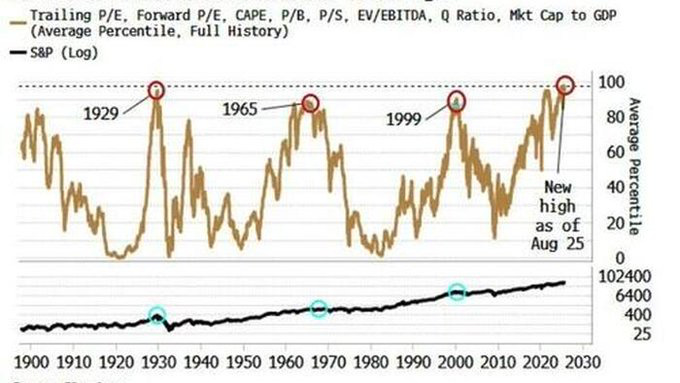

The ‘Jaws of Kyoto still stand here…

The structure of this broadening formation will take some time to resolve, though at third, and fourth glance - does not appear to be an overwhelmingly bullish development, with the VIX and credit spreads buried below the surface of reality. Without a doubt, the most important chart for the remainder of the year.

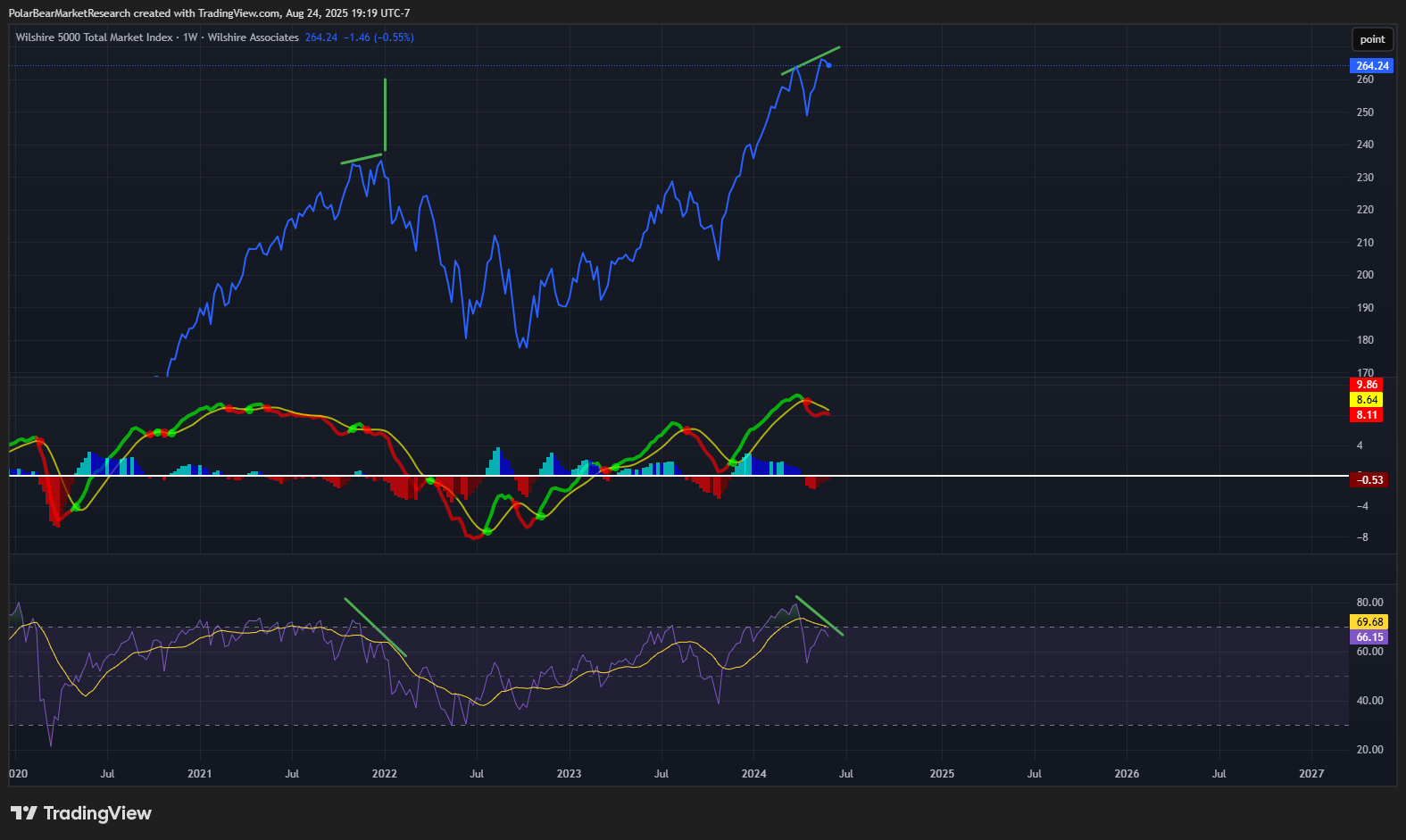

Wilshire 5000

Interesting signals developing for the Total Market Index… similar to some of those seen in late 2021.

A top/distributive pattern is something that takes time, and we’ll keep a close eye on it.

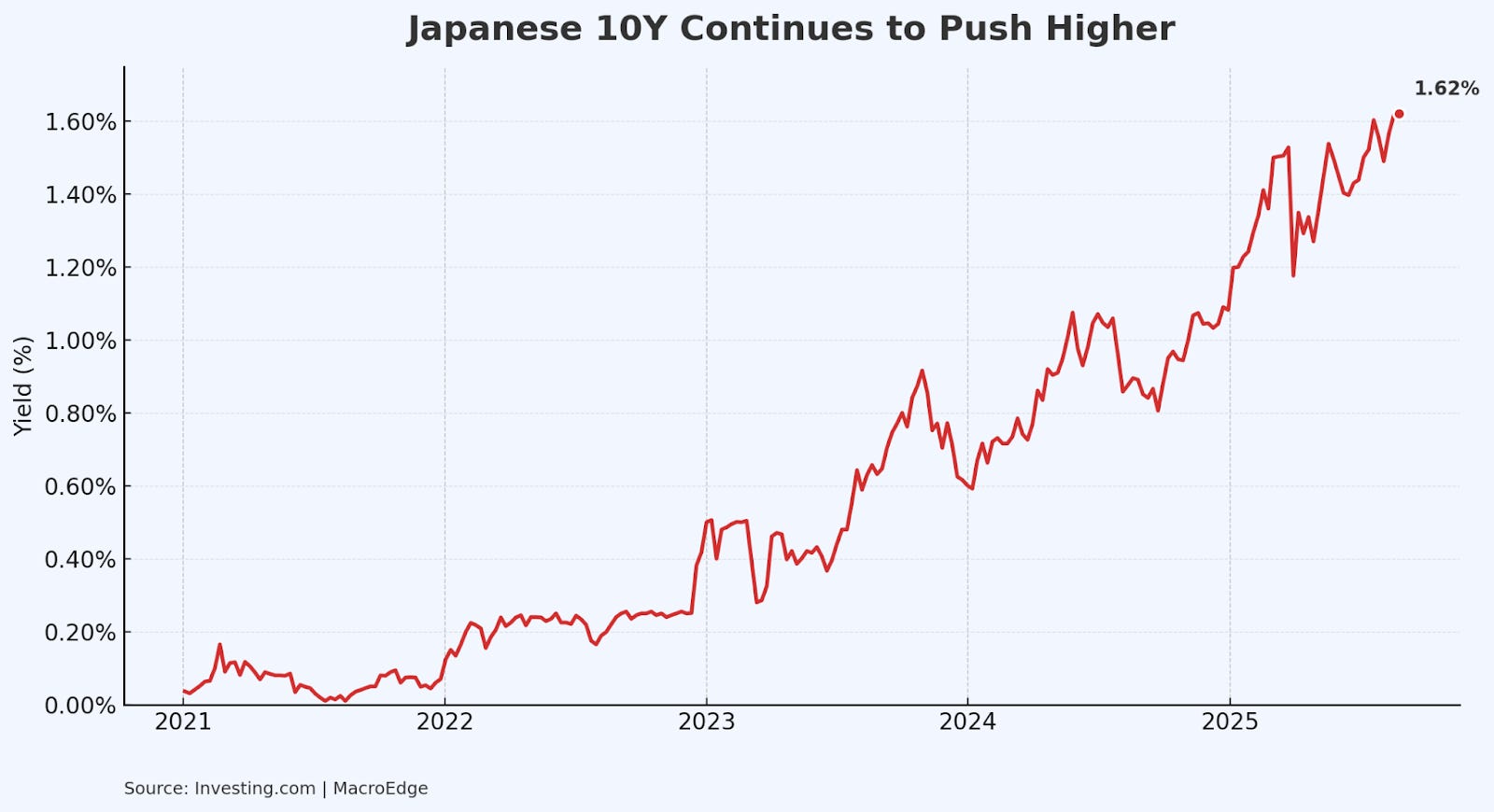

Keep an Eye on Japan

While we’ve lessened our focus and emphasis on Japan over the summer - after the BoJ intervened heavily to save markets temporarily - those efforts are again providing futile in the Japanese bond market. Keep in mind, this is a nation with a 250% debt/GDP ratio…

A more hawkish BoJ in September is an interesting left-tail event to watch:

Trump’s Stagflation Nightmare Accelerates with Powell’s Folly (@RealJohnGaltFla, MacroEdge Contributor)

As someone who studied history and lived through the late 1970s in high school then into college, it might seem like I am now once again sound like the old man screaming at clouds type of warning. This is only because every type of monetary and economic theoretical mistake of that decade seems to be the path that both the President of the United States and the Federal Reserve seem damned to repeat.

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.