Weekly Macro Note: Elon v Bessent, Another Tariff Delay, June Employment Stays Mediocre, Financial Pandemic of 2025

In this Weekly Macro Note the team notes the light weak ahead for macro data & earnings - and encourages readers to focus their attention back on 'tariff letters' and vol inducing headlines...

Elon v Bessent, Another Tariff Pause...?, Quiet Macro Week, June Employment Stays Medicore (@DonMiami3, MacroEdge Chief Economist)

Good Sunday evening, MacroEdge readers and community,

As we wrap up the Fourth of July holiday weekend, I hope you all enjoyed the long break and are ready for the second half of the year. Hard to believe we’re already there, but I read another “fun fact”: we’re now closer to 2050 than we are to 2000.

The “Big Beautiful Bill” was signed last week, carrying major macro implications. Corporate heavyweights like Musk are now taking aim at what they see as continued pandemic-level emergency spending that keeps finding its way into bill after bill. While the prevailing narrative is an “all-clear” following this latest pre-bailout signing, mixed signals remain across the economy on growth, employment, and inflation. We’re likely to see at least a baseline level of tariffs implemented by September, though their revenue impact on the U.S. will be minimal. An announcement on tariff rates could come as soon as tomorrow.

Now that the spending bill and tax-cut extensions have passed, expect the administration to turn more fiscally hawkish if CPI starts ticking back up. They remain laser-focused on equities—and, to a lesser extent, the bond market. It’s a quiet week for data, but with the bill pushed through on party lines, the bond market is sure to be top of mind in Washington. The pro-blowoff regime continues for now - and the next macro shift is yet to drive any disruption there. We’ll have more in a Midweek Macro Note this week.

Things to Watch This Week - Quiet Macro Week

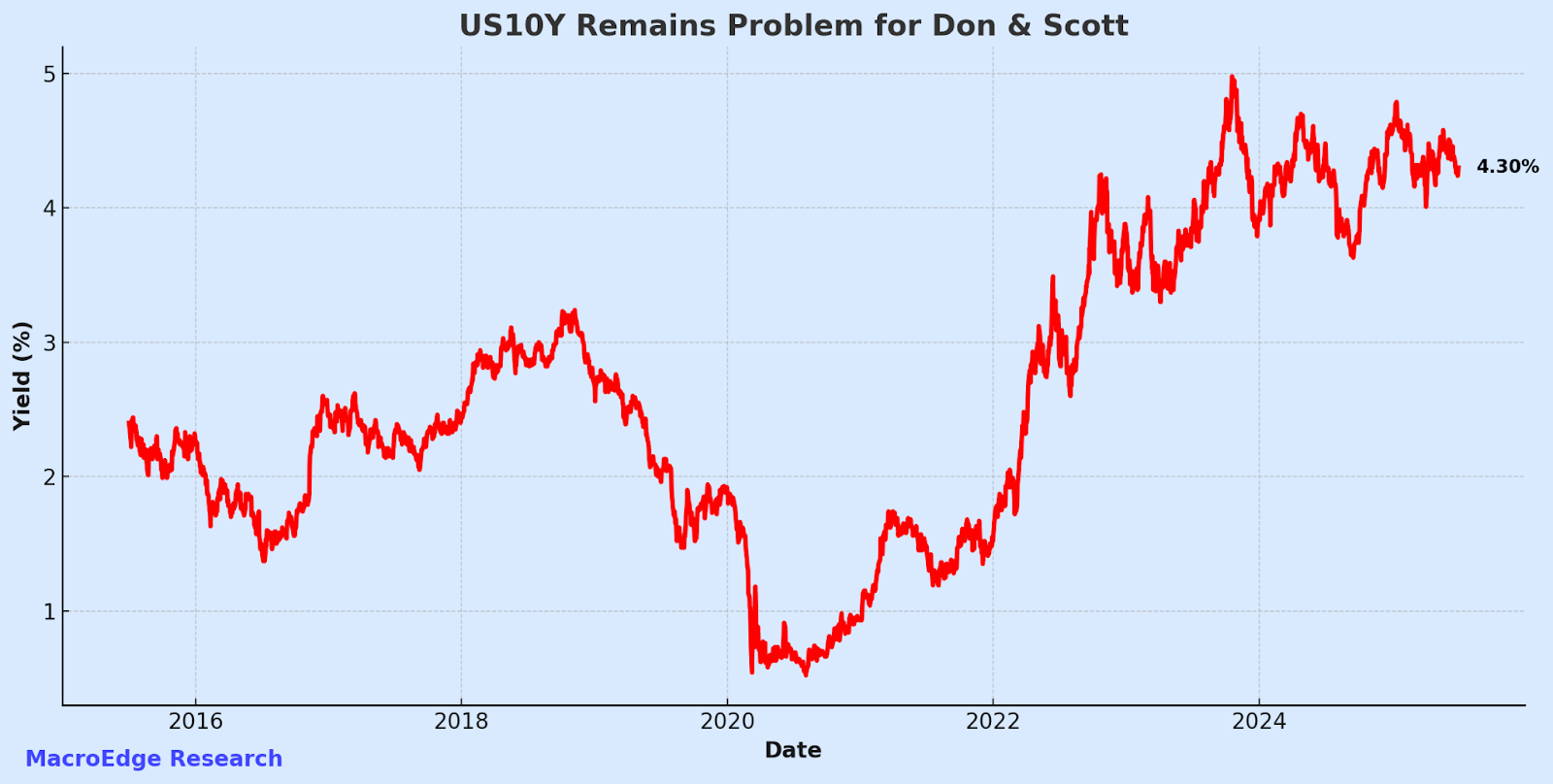

The 10Y yield remains constructive which may cause the Admin some fear… with the lack of critical macro this week – we’re likely to see some lower volume and less attention in markets as we continue a ‘vacation mode’ through mid-July leading up to the FOMC announcement at the end of the month.

This week we also get the FOMC minutes, and what will likely be an additional round of pricing out a July cut if data continues to come in okay.

Week of July 7–11, 2025 | MacroEdge Weekly Outlook

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.