Weekly Macro Note: Knocking on Heaven's Door: A Return to Greenspanomics? ... & An Inflation Report Courtesy of the Federal Reserve and Tariffs

In this Weekly Macro Note, the team explores the Administration's desire to return to the Greenspan-era, the cooling real estate and employment environment, odds of rate cuts, inflation, and more.

Knocking on Heaven’s Door: A Return to Greenspanomics? (@DonMiami3, MacroEdge Chief Economist)

Good Sunday evening MacroEdge Readers and Community,

As we lock-in and return to a more normal cadence after setting up our new operation hubs (still a work in progress… but we’re getting there) we turn the corner into a new month and find ourselves closer to the fall. While we’re not quite there yet, with the latest dose of employment data and the coming shifts at the BLS - we’re quite likely to see employment data get cooler through the remainder of the year. With an Administration hell-bent on lower rates, the updated data overhaul may bring about softer data that gets them to their end results of a lot more than 2 cuts over the next year.

The data on Friday sharply shifted the next cut forward to September, with an additional cut expected after that in October – which takes us nearer to the end of Powell’s tenure. Powell is likely to remain in hawkish mode for the time being given the lagged impact of tariffs on inflation, which is showing up (slower than expected). With all of the data headfakes over the last two years, we shouldn’t take a single datapoint and make broad assumptions from it, but can acknowledge that the continued trend of labor cooling has been very obvious since the Fed began hiking back in early 2022.

From a technical standpoint, we’re in one of the most extreme regimes on record - especially in tech. The run-up since April has truly put us in a historic runup - on par with 1998-99 and larger than the gains experienced after the pandemic - and valuations are at their highest level on record - with market cap concentrations also pushing back into the 99.5% percentile, historically. All that being said - we’re back in the ‘K2’ zone. Still, we have an Administration openly citing Alan Greenspan as their model economy (think bubbles & easy money) and not balanced budget of the 90s… since we are no where close to that, but retail risk on is something that takes a long time to shake. I still think the latest bout is going to take more to break it than just a few 1% drawdown days. From a macro standpoint, the Admin wants those lower rates to bring back life into the housing market - though we’re seeing some early signs of stress and distress now in the construction spending and real estate employment datapoints, which have lagged aggregate construction pretty dramatically. Don’t forget historically that employment lags the most - and real estate employment is no exception to that rule.

On Wednesday we will have the first edition of our MacroEdge AlphaSights Report (#1) out for July-August, covering unique opportunities, value, and more - and this first edition will be accessible for all current MacroEdge Ozone readers. Going forward, you can inquire to access future editions of AlphaSights - which are focused on delivering alpha that you can profit from, direct to your inbox once a month, right from our team.

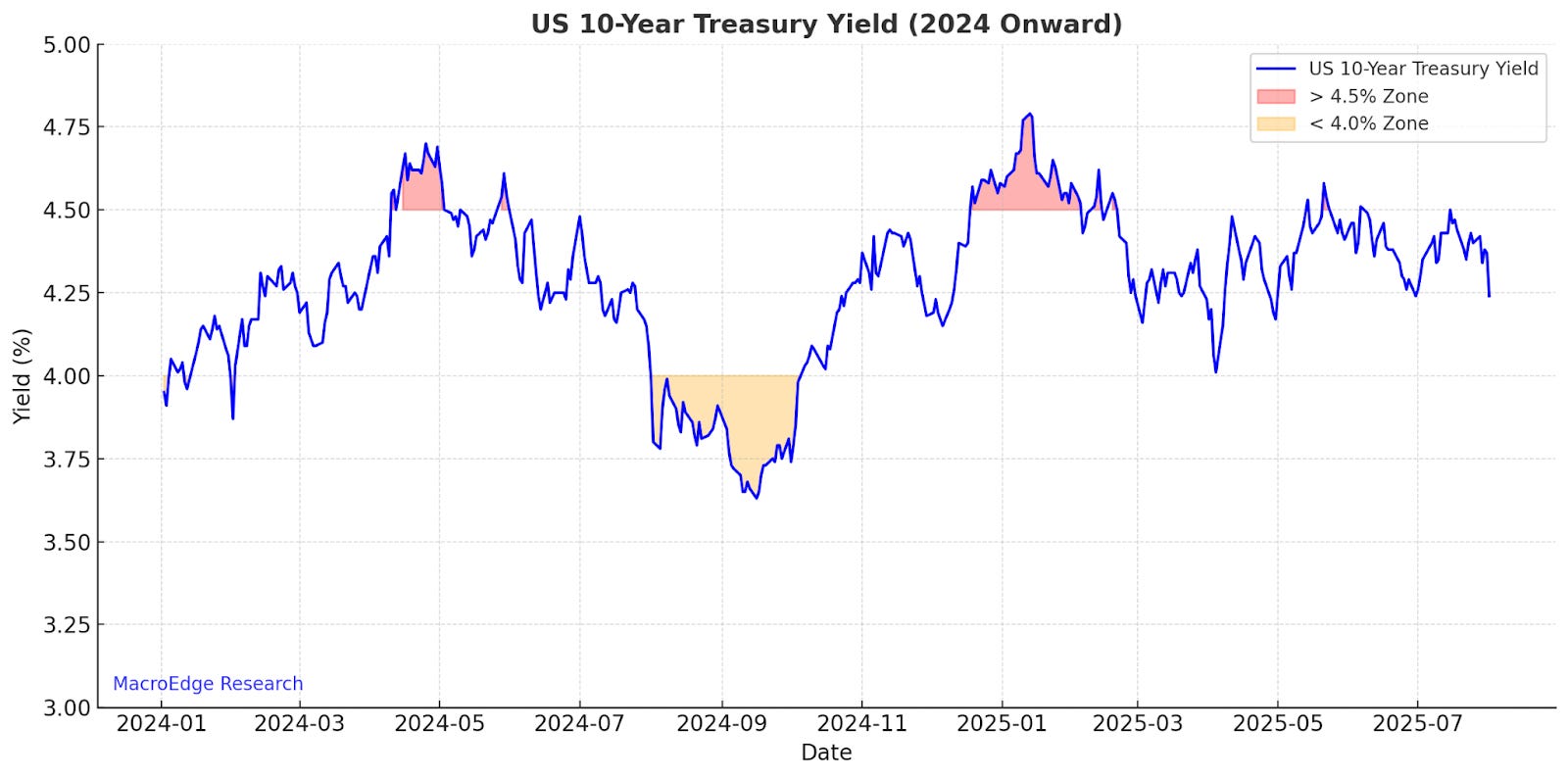

For the 10Y… let’s see how the remainder of the year plays out:

The zone above 4.5% or close to it has been the ‘red zone’ for policymakers, while we saw last summer a dip into the ‘recession zone’. For now, the range remains very defined and watchable going into the last 5 months of the year. There’s a lot of competing forces - from tariffs to softening employment - that will continue to play a role in the direction of the 10Y.

Access MacroEdge Ozone for two weeks and get access to all of our insights and data, below:

The Macro Ahead: What to Watch This Week

For earnings - it’s likely that Q4 is the story of slowing again, as Q2 numbers are holding up quiet well for a lot of companies. The reaction for Apple and Amazon was interesting, and we have plenty of earnings coming up this week (most importantly being the AI names, Berkshire, and consumer barometers like McDonald’s):

From a data and macro standpoint - continue to watch for signs of Fed direction as we head towards September, with a sharper divide in the ‘camps’ of Fed voting members as we continue to see more macro data. While things are soft - especially in the middle and lower classes - there’s still little reason for a ‘total panic’ - ie: inter-meeting cut before the September FOMC. It now looks likely that this is when the next cut is going to occur, and if housing and its employment cool further then we’ll have a lock sooner rather than later. Freight is another barometer that has cooled sharply again, and capacity rising there continues to put stress on operators - as evidenced by surging bankruptcies (somewhat of a similar story for restaurants too…) unable to manage their costs, with surging competition.

Monday: Factory orders, vehicle sales

Tuesday: ISM Services, Total Household Debt

Wednesday: Fed Cook Speech

Thursday Claims, Fed speakers, Consumer Credit

Friday: n/a

From a pure macro data standpoint - this week is not that impactful, which may drive positive equity action early in the week if earnings continue to hold up fine - and things may slow again later into the week. If we see softness in names like AMD, that may provide a warning sign for things like construction spend in the data center space, and more, which should be watched and noted for opportunity. The bigger the blowoff becomes, the harder it’ll be for policymakers to intervene once things spiral the other way, as they inevitably do.

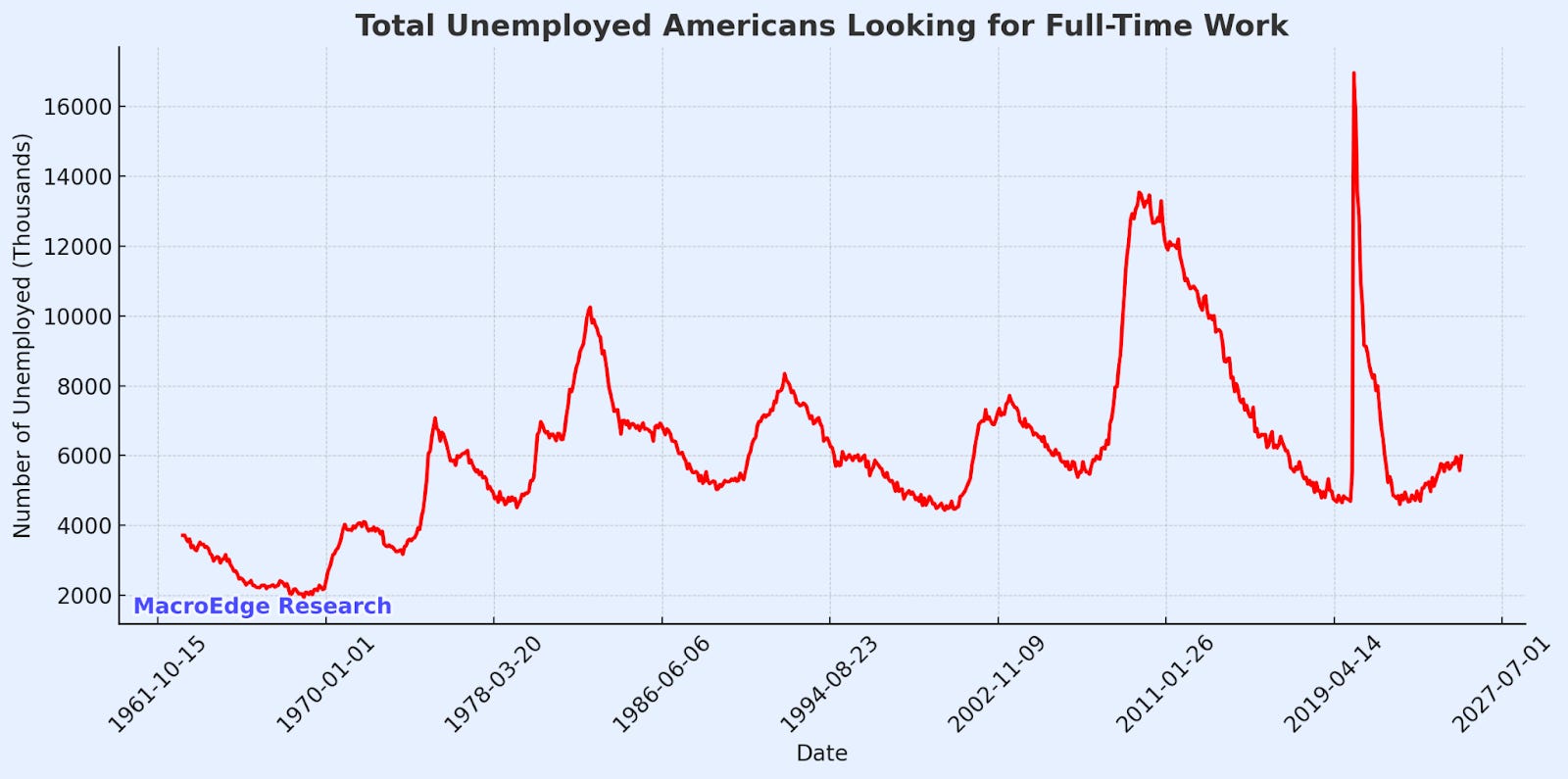

Employment Overview - Cooling, Especially in Real Estate

The most obvious barometer of employment health going forward will be our large cyclical sectors - namely real estate. That being said, we’re seeing some continued new highs of soft employment (aggregate) datapoints, like the below:

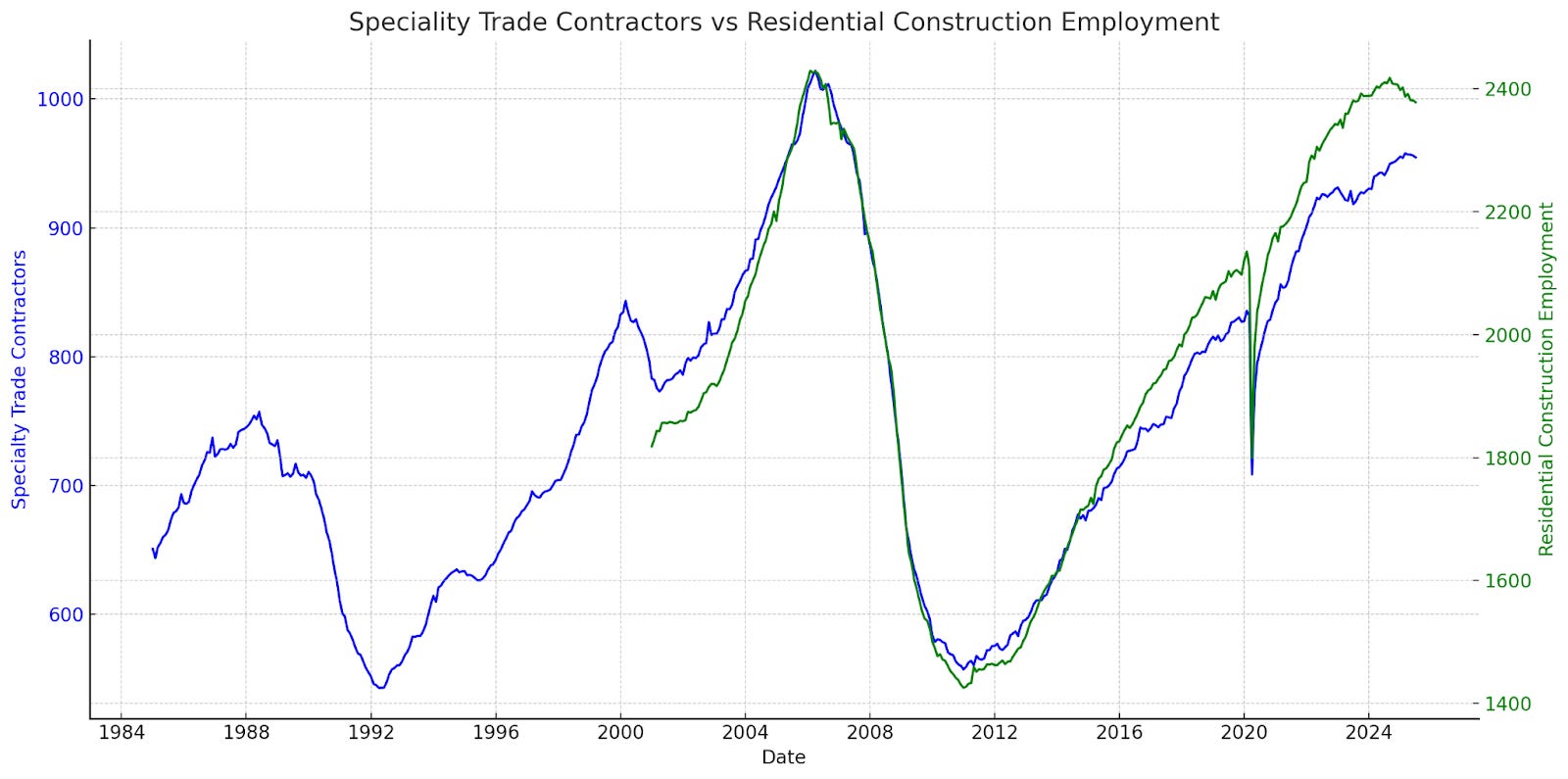

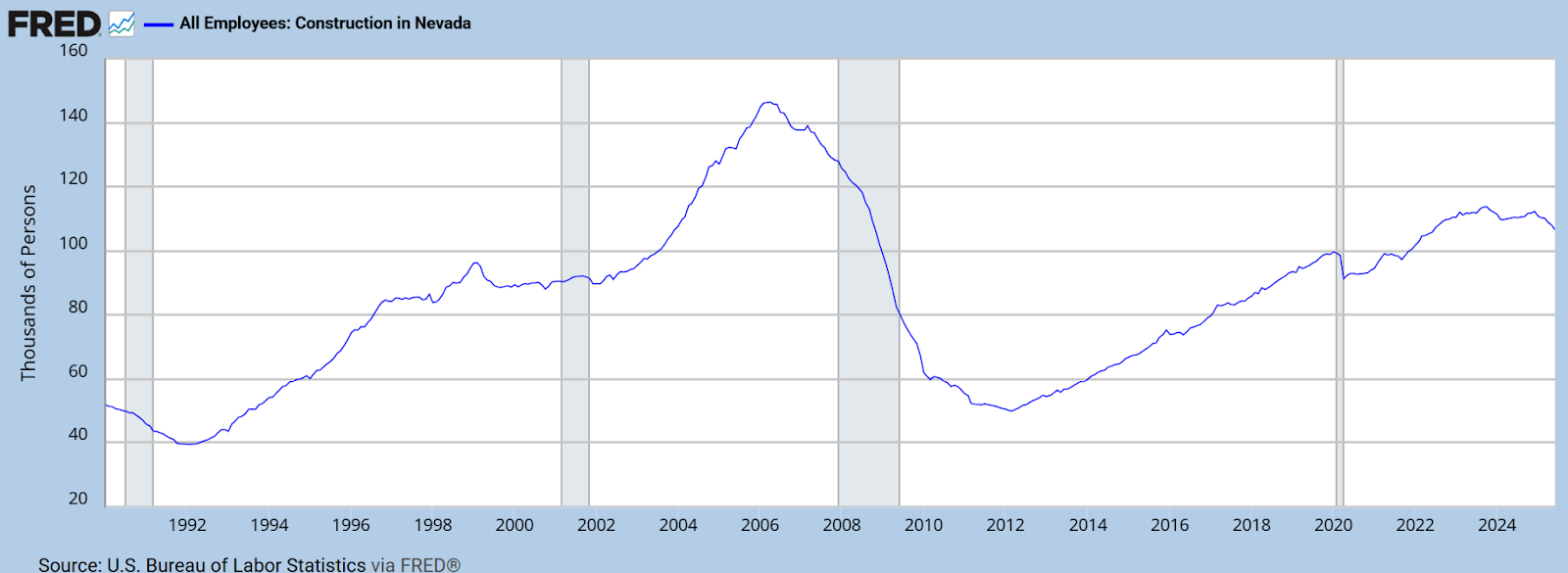

& in real estate, things are cooling, too:

Both specialty contractors and residential builder employees have been falling now for the last several months. Both ironically, or un, their previous cycle peak. With an Admin hellbent on goosing this sector, however, it’s likely we see interventions, bailouts, YCC/rate cuts or other measures before we see them let this sector fall too far, at the current time. That’s not to say we can’t respect the lag, which finally seems to be biting, and rate cuts take a long time to impact employment (they do), there’s just a lot of support for endless bailouts in the RE world… even if you cannot print buyers, or can you?

There’s always the opportunity to look under the hood…

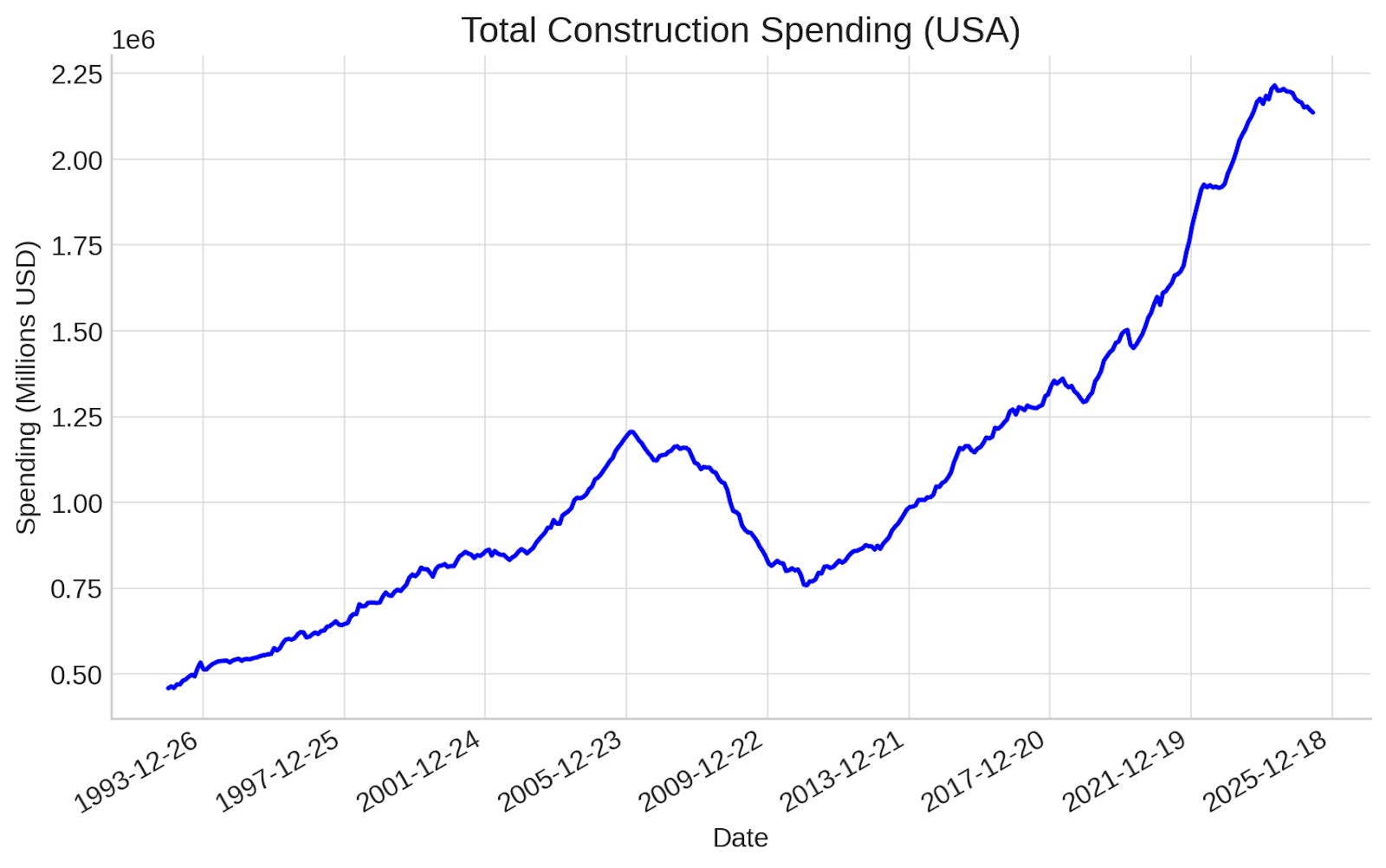

Construction Spend is Getting Problematic - Cyclical Slowgrind to a Halt

Construction spend has enjoyed a boon - especially due to data centers and growth in manufacturing - but we’re seeing those trends rollover:

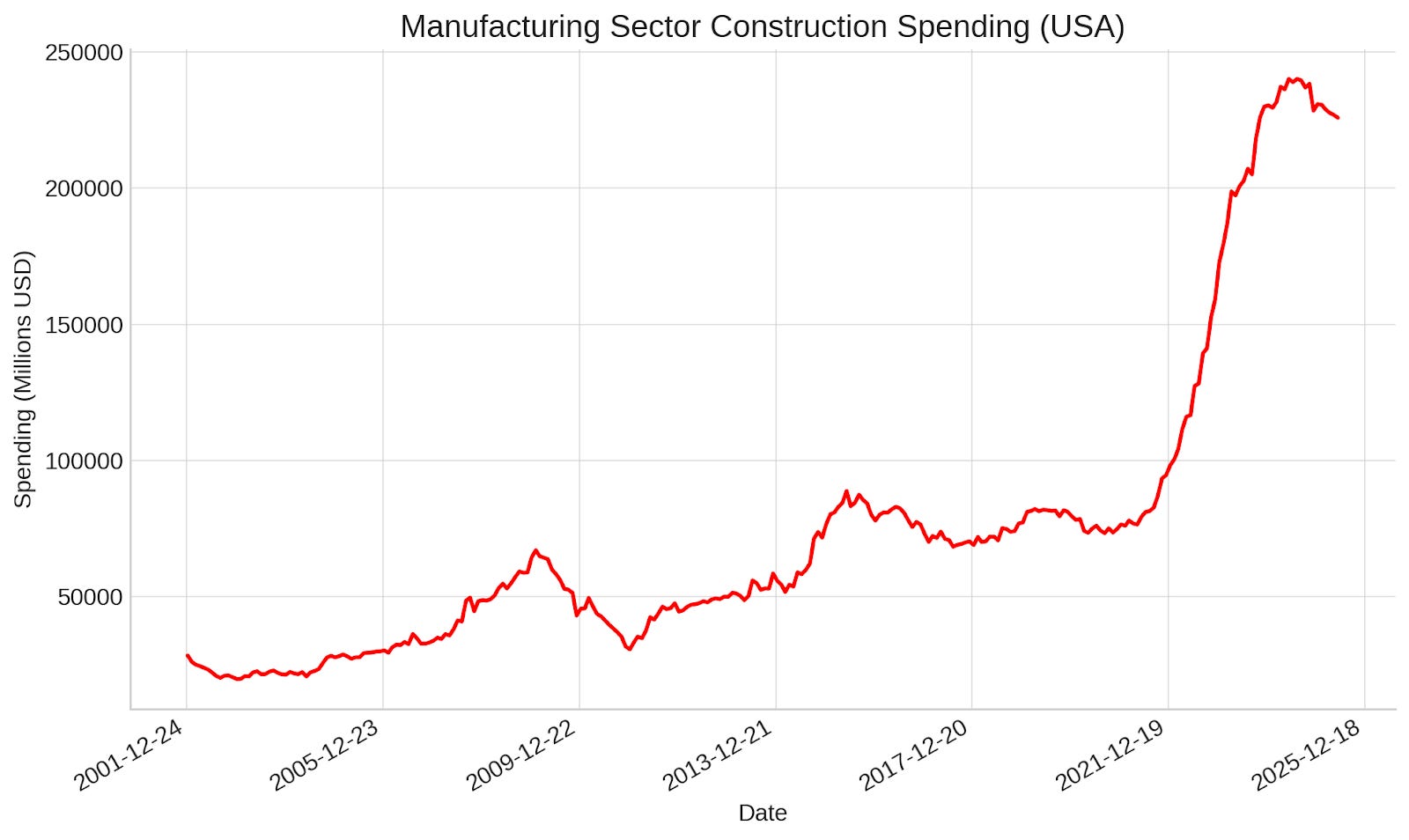

And in manufacturing…

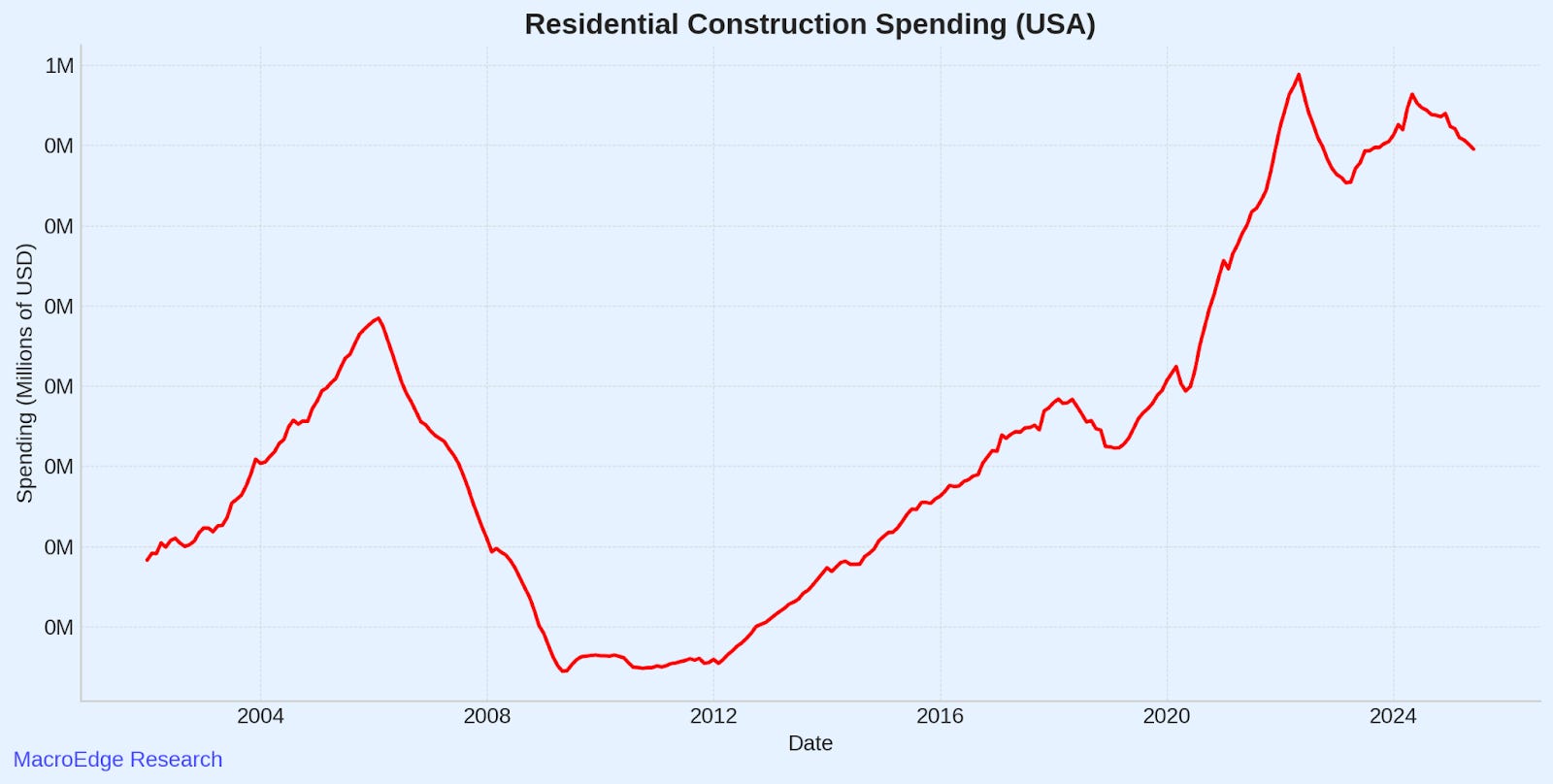

And in residential construction (again) - the most important for employment, too:

Builders continue to be way out over the skis for the time being - especially eating it in the Sunbelt - though we’ll see how the Admin’s support for them shifts over the next few months.

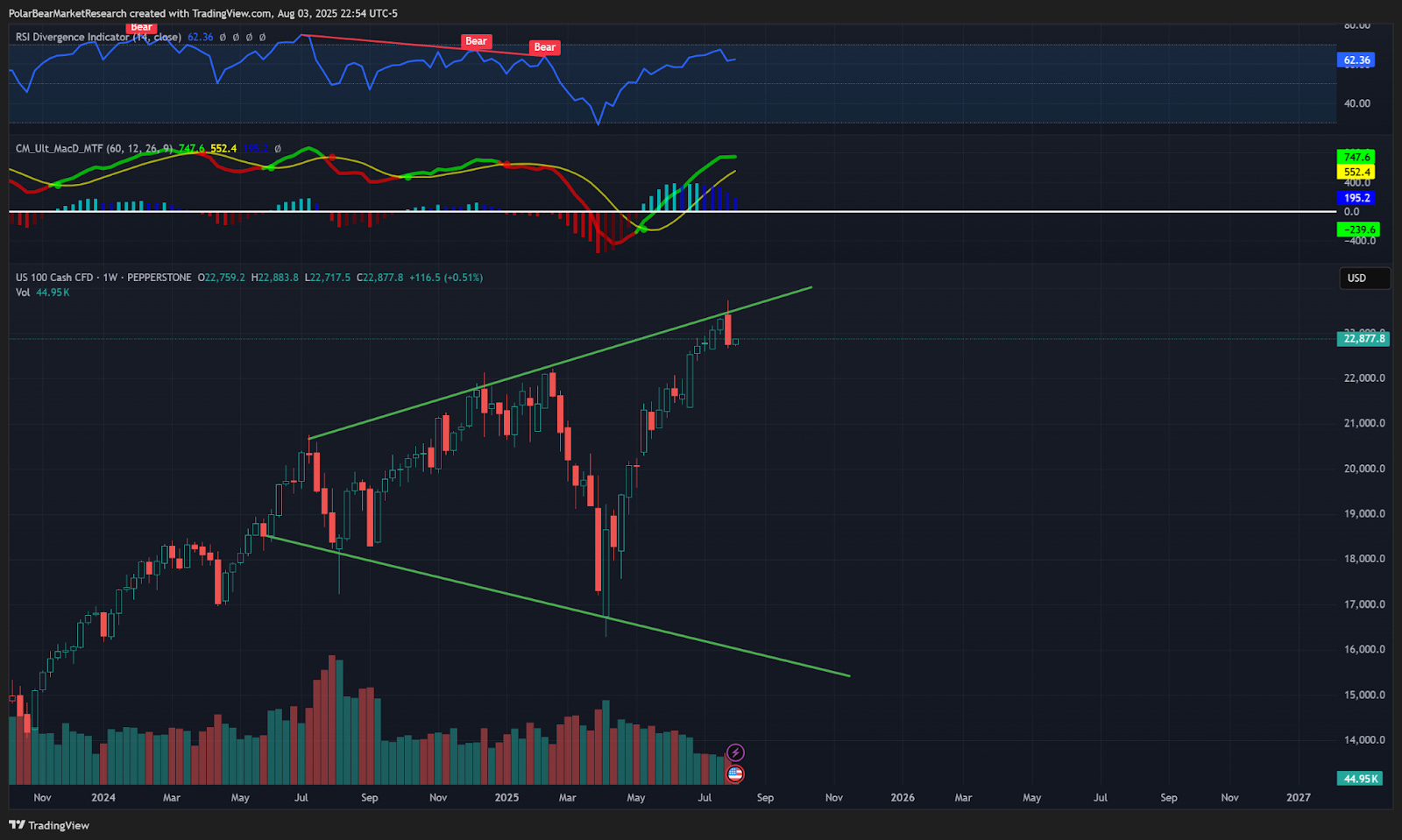

Technicals: Finally Showing Some Distributive Signals, but No Triggers Yet

On the technical front, we don’t have enough to hit the alarm for a similar move that we saw in March and April, of a nearly 30% drawdown on the Nasdaq – but there’s obvious reason to start paying attention again for a move the the other way… against the trend, that is:

There better be a full and complete move towards currency debasement and pro-inflationary policy, coupled with lower rates to keep seeing things move astronomically higher, and other factors need to participate alongside of that as well to make it a reality.

We continue to see a lot of pre-recessionary data - with the employment market and real estate continuing to cool.

The Bitcoin barometer (of risk…)

Bitcoin is slowly but surely showing bearish divergences on about every possible timeframe (from the 1D on) and those will have to validate or invalidate themselves:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.