Weekly Macro Note: Into the FOMC Circus & Peak Earnings Season for Summer, Consumer Weakness, De-Cyclified SaaS Opportunities, Powell's Future

In this Weekly Macro Note - the team articulates the 'FOMC circus' and why a higher longer-end is problematic for July rate cut dreams... for now, discussed earnings this week, software, and more

Into the FOMC Circus & Peak Earnings Season for Summer (@DonMiami3, MacroEdge Chief Economist)

Good Sunday evening MacroEdge Readers & Community,

We remain in the summer lull period as we’ve defined it and are now just a week out from the FOMC rate decision next week - where the Fed is likely continue holding rates - barring any rapid pivot by Powell to convince FOMC members otherwise. Powell knowing that he’s on his way out has little incentive to do just that and the FOMC is increasingly divided between those that want to cut and are vying for a promotion or continued term on the Board and those that are not keen on rate cuts (like Kashkari, and at least for now - Jerome Powell).

That’s not to say the economy is all roses and unicorns - the ‘bifurcation nation’ continues - with signals like a continued slowdown in luxury fine dining and Hawaii travel falling off a cliff as evidence of weakening at the margins - the asset class continues to thrive with the wage class continues to get clubbed over the head by fiscal & monetary policy. The answer to insanity is not to turn up the insanity levels with rate cuts at this point in time as the solution to bolster affordability and lower the debt burden for the government, especially as M2 begins to pick up speed again.

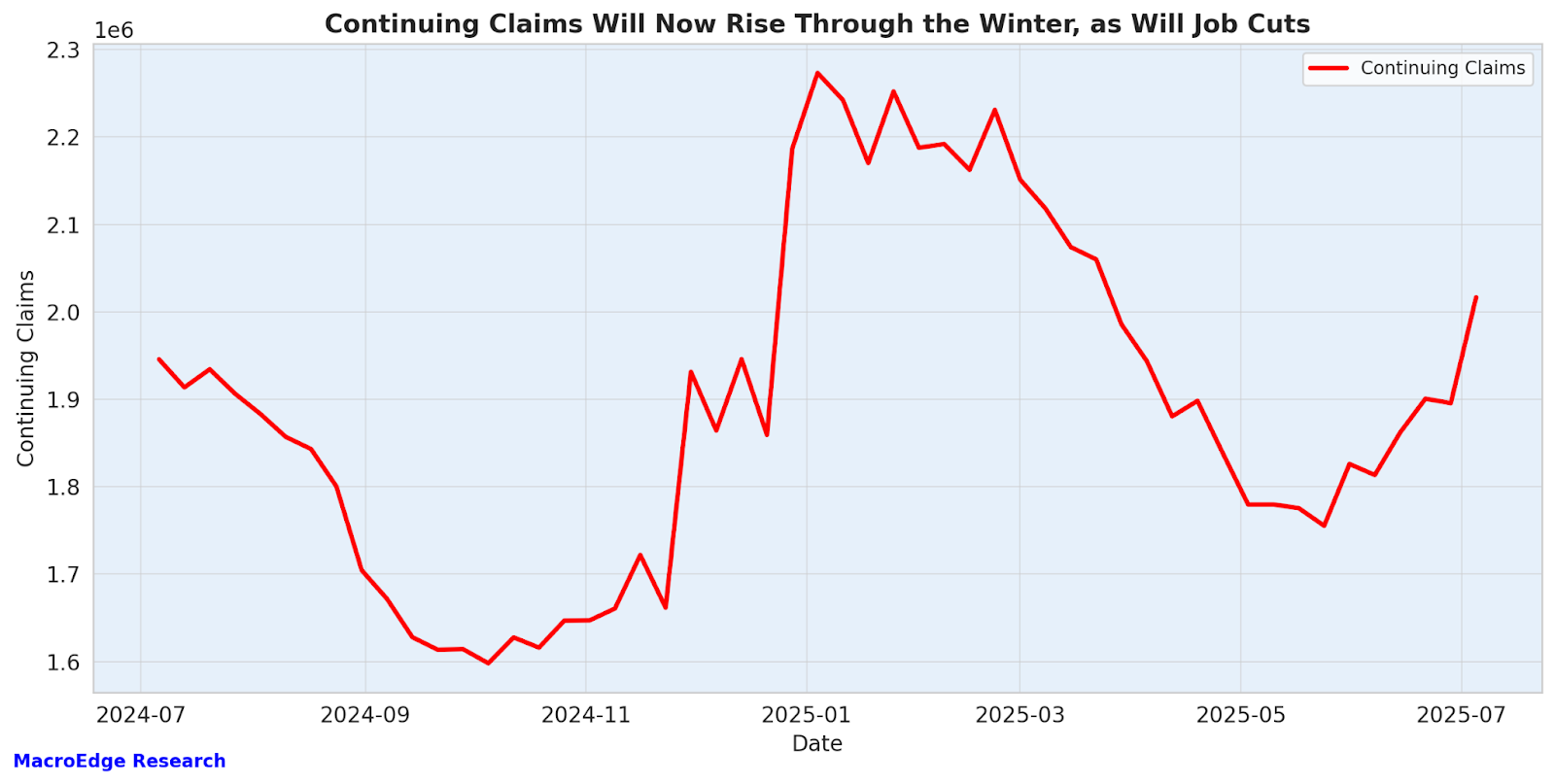

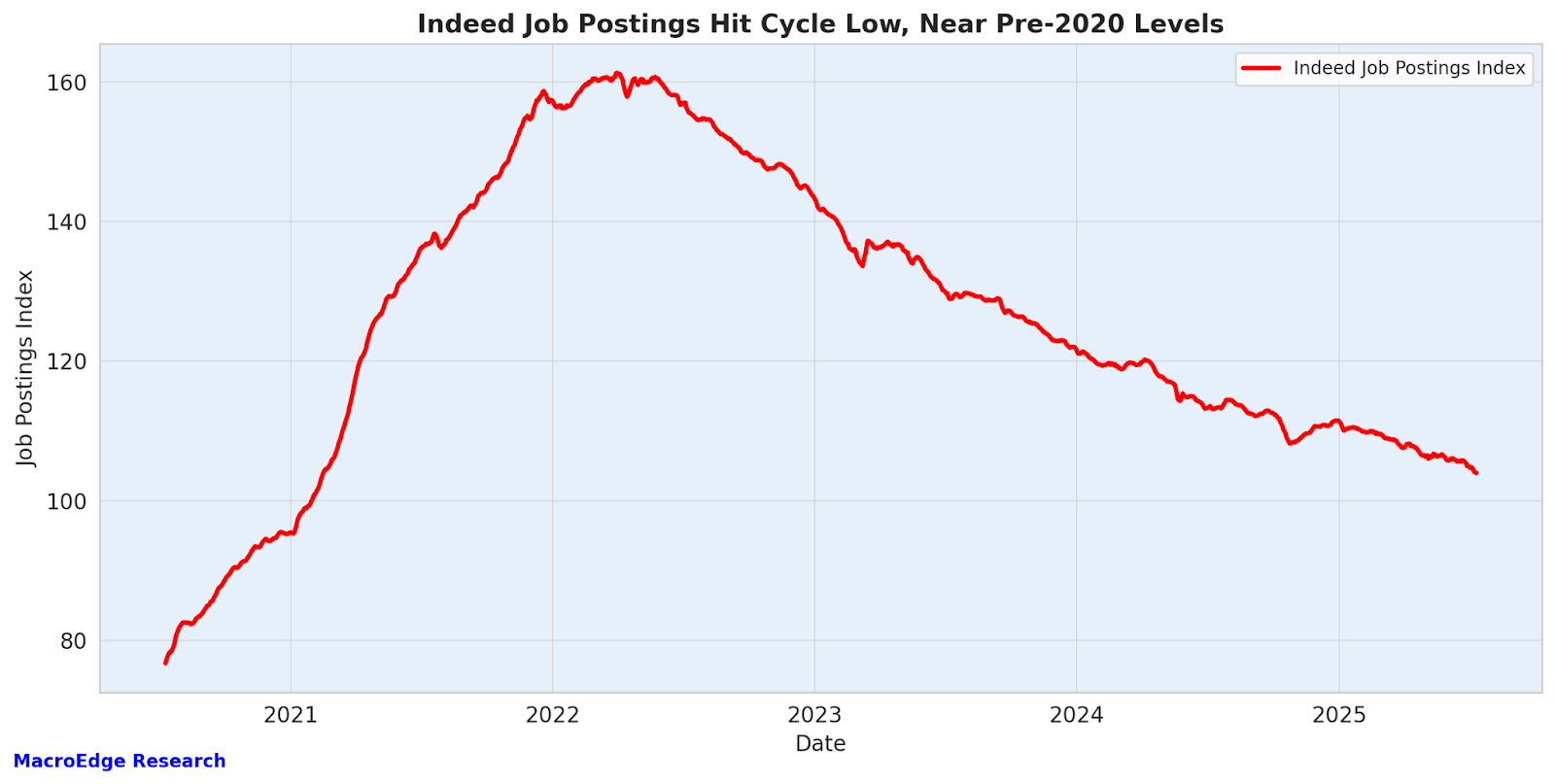

Employment data itself remains soft - but at a 1990 cycle rate and showing no signs of 07-weakening yet - looking at both job postings and claims (CCSNA in millions):

Indeed Job Postings — a new cycle low:

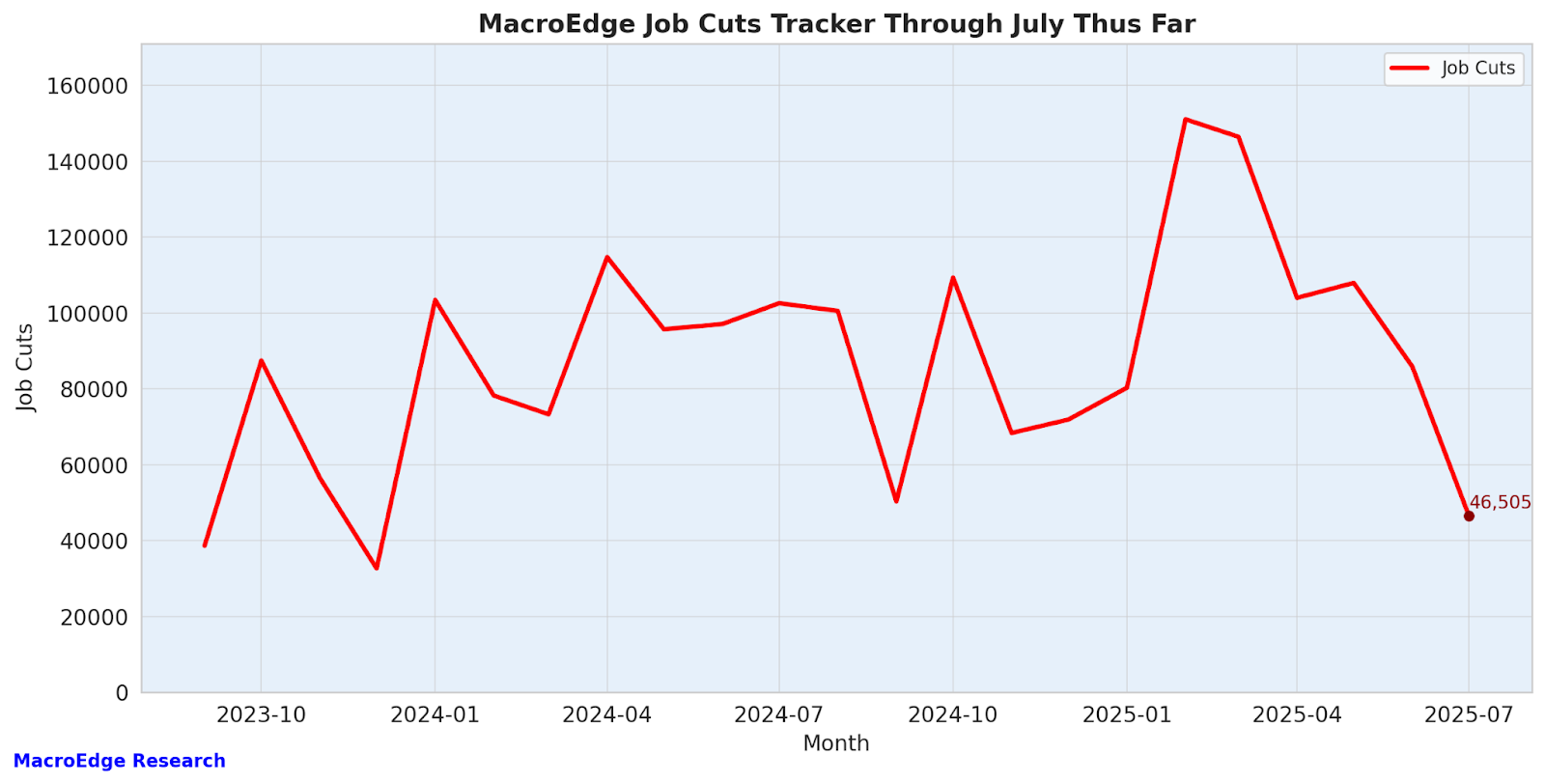

Our own employment data shows a cooling in the number of job cuts for now, after the DOGE spike, and we will likely not see a rise until September, post Labor Day, and correlated to Q3 earnings.

Keep in mind that employment is usually the absolutely final metric to crack…

If you missed our operational update last evening covering all of our new exciting offerings, see the Redeye Macro Note from yesterday evening:

Redeye Macro Note: Accelerating our Enterprise, Into the Stratrosphere, Chart Blast, Videos from the Past

Good Saturday evening MacroEdge Readers & Community,

There may be website disruptions this evening, please pardon them for the time being, and stay tuned for continued updates through the remainder of the week in our reports & through our Social Club on X. We’ve delayed the release of our video series while we prep for the first MacroEdge office location opening, so stay tuned for more across the board with what we’re doing through Research, Transform, and Economic Advisory.

Access MacroEdge Ozone for two weeks at:

Macro Data for the Week

> Continue monitoring the 10Y

> Personal Income and Spending including Core PCE

> CPI and PPI inflation reports for July> Weekly jobless claims and ADP employment change> Flash Manufacturing and Services PMIs

> Earnings season continues

This week’s data will help confirm whether the current softening in certain macro trends is sufficient for a pivot or if the Fed will continue to wait for further disinflation and labor market cooling.

The 10Y Leaves Little Reason to Cut for July

The long end of the Treasury curve remains elevated with the 10-year yield holding near 4.4 percent. This continues to pressure financial conditions upward despite no movement at the short end. The bond market is not pricing in any urgency for rate cuts. Growth expectations remain solid. Inflation is proving sticky. Real yields have stayed firm.

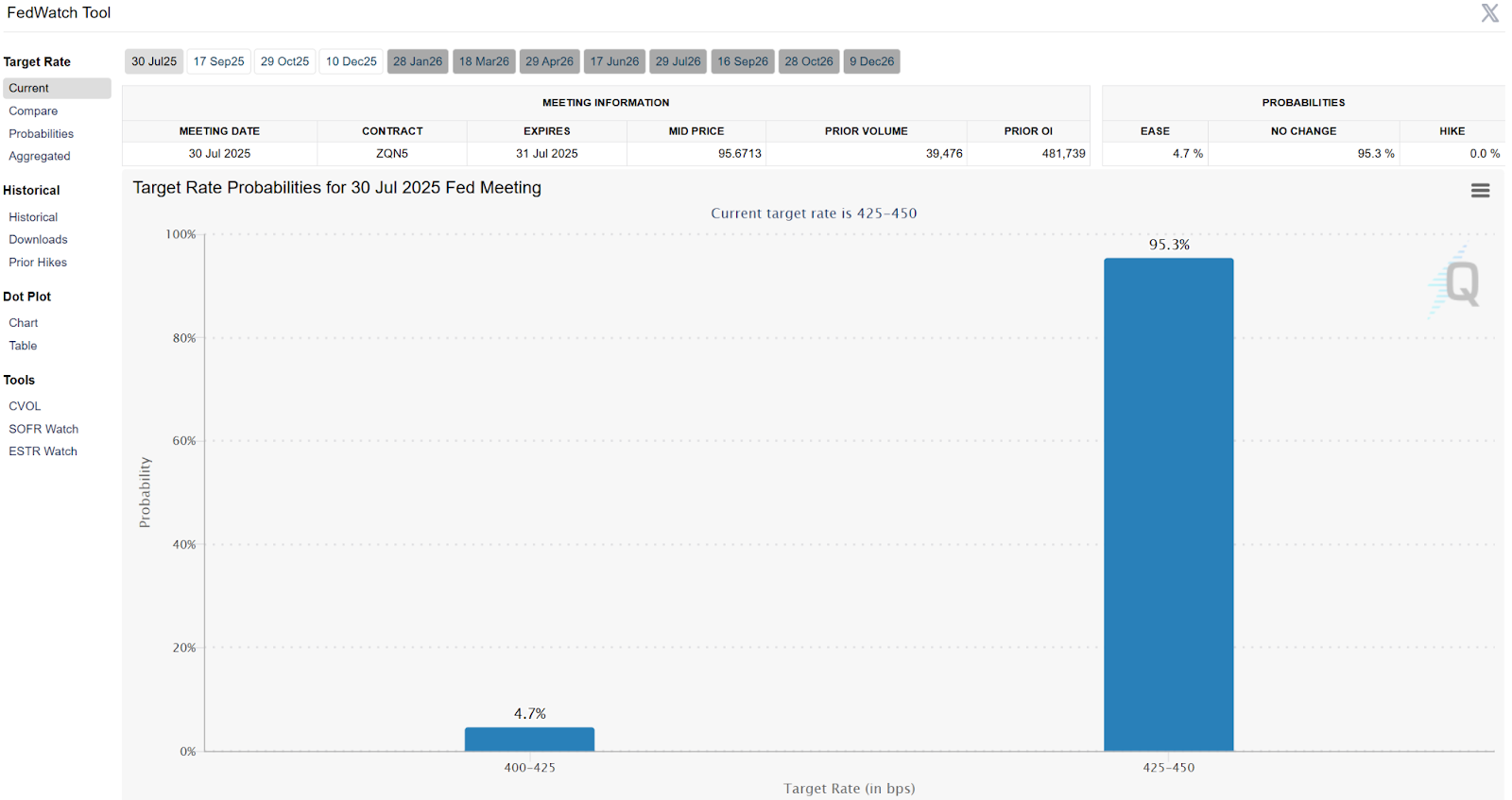

CME Fed Funds futures currently price in less than a five percent probability of a July cut. Fed speakers have shown no interest in moving early. The narrative has shifted to September or beyond. Market participants broadly understand that cutting now would risk undermining the Fed’s credibility given the data trajectory.

There’s no crisis. Financial conditions are still super loose (as our spreads). The Fed is looking for more confirmation that inflation is trending to target before making a move. The economy is not signaling a need for emergency action.

Odds of a July cut are sub 5% now, and with little in the way of macro data until then, no cut through September remains likely:

Rate Cut Odds are Still Pushed Until September, & Moving Towards October

Rate cut odds remain heavily skewed away from July and August, with market pricing and Fed commentary pointing to September as the earliest possible window. Futures have consistently reflected less than a 10 percent probability of a move in July, and even the September meeting has seen sliding confidence in recent weeks as core inflation remains sticky and growth data refuses to materially deteriorate. The Fed has clearly communicated its desire to see sustained progress on disinflation before pulling the trigger, and so far the data hasn’t provided enough assurance to justify an earlier shift. Financial conditions remain very loose (just look at crypto and equity market speculation) further reducing the urgency to act preemptively.

What’s evolving now is the creeping shift of expectations toward October or even December. With each passing data print that shows a confusing picture in labor or inflation metrics, the probability distribution slides further into the back half of the year. This also reflects a deeper truth (now we will have the Big Beautiful Bill to skew growth), there is no pressing need for the Fed to force a move until either markets break or the economy buckles. Unless either of those things happen swiftly, policymakers are increasingly likely to wait for a fuller inflation deceleration trend to emerge before cutting. The tone of rate expectations has certainly changed.

Yield Curve Control…?

If the long end of the curve remains stubbornly elevated despite Federal Reserve rate cuts, a future Trump administration could consider an aggressive and unconventional approach like a form of yield curve control. While historically more associated with Japan, YCC involves targeting longer-term interest rates by committing to purchase Treasury securities in unlimited quantities to cap yields. If inflation subsides but long-term yields remain high due to fiscal concerns or structural imbalances, the political incentive to intervene could rise, especially with a pro-growth agenda reliant on keeping borrowing costs manageable. A Trump-aligned Treasury and Fed could explore some variation of this policy to suppress long rates without further slashing short-term rates, allowing stimulus to flow without reigniting inflationary pressures. I might sound crazy, but don’t rule this out.

Peak Earnings Season

Megacap earnings this week:

Monday: Verizon

Tuesday: Coca-Cola

Wednesday: Alphabet

Thursday: Tesla, ServiceNow

Friday: HCA Healthcare, Phillips 66

As we progress further into earnings - optimism has continued to be underpriced for now after the April tariff scare. Things continue to look okay from an earnings standpoint, and problems in earnings may lag into late Q3/Q4, which by that time will meet Big Beautiful Bill tax boosts and other stimulus forces. It really depends on the company, industry, and identifying where the opportunities lie.

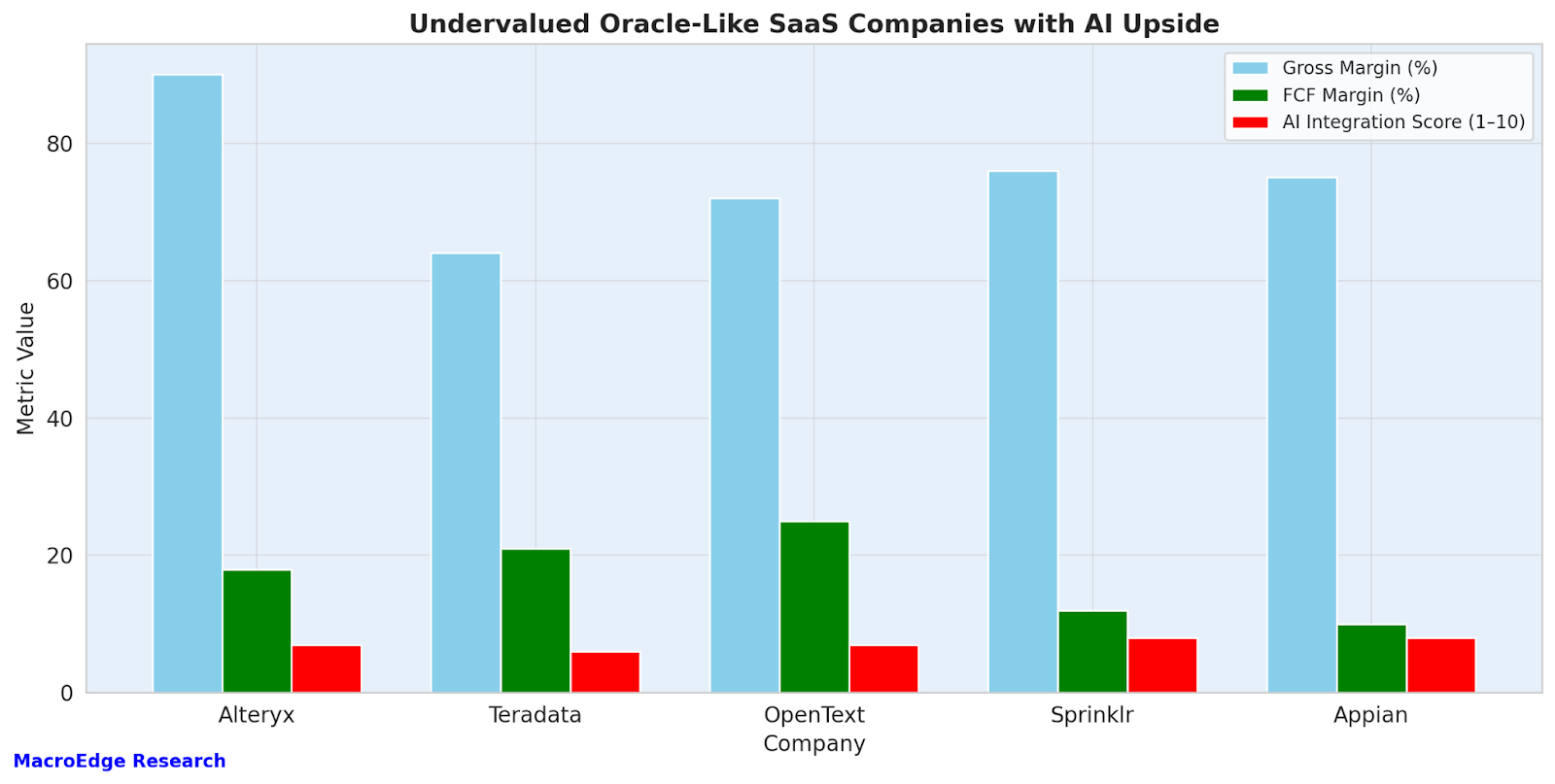

SaaSy Opportunity

… the current wave of excitement around artificial intelligence has caused investors to overlook some of the most fundamentally sound areas of tech. Capital continues to chase semiconductors and bleeding-edge infrastructure while enterprise SaaS companies with high gross margins and strong free cash flow sit largely ignored. These businesses are not broken or at risk of disruption. Instead, they are well-positioned to integrate AI features into their existing platforms in a way that adds value without cannibalizing their core. This creates an asymmetric setup. Investors get exposure to operational leverage, predictable recurring revenue, and the upside from AI enhancements without paying extreme multiples.

Oracle is a prime example. Long seen as legacy tech, it has rebranded itself as a modern infrastructure and AI backbone. The market has finally rewarded that transition. However, there are several smaller companies that mirror Oracle’s structure but haven’t yet received that premium. Firms like Alteryx, Teradata, OpenText, Sprinklr, and Appian (we discussed some of these yesterday evening) operate at the intersection of enterprise data, automation, and analytics. They offer sticky software, real customer reliance, and increasingly layered AI toolkits that make the product better, not riskier. These companies have high free cash flow conversion and strong unit economics. As the market eventually rotates back toward profitability and resilience, these names could re-rate meaningfully.

Many of these names, heavily integrated into enterprise data are also more cyclically-immune, unlike many other names like those in the homebuilding segment, etc.

Have a great start to your week and we’ll talk to you on Wednesday evening.

Don

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.